Below are Hedgeye analysts’ latest updates on our twelve current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each.

Please note we added UUP (U.S. Dollar), ZOES (Zoe's Kitchen) and FNGN (Financial Engines) this past week.

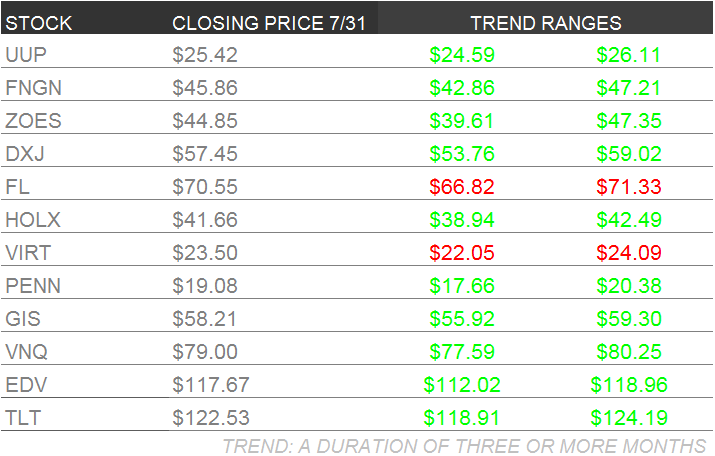

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

ZOES

ZOES stock sky rocketed in June, and although the valuation is high, we don’t view it as overvalued. This is a differentiated concept with little competition in its way. ZOES’ operational and profitability metrics are ahead that of Chipotle’s in their early days, giving us even greater conviction in this LONG idea.

About a month ago their CFO resigned and although he was a leader within the company, we are confident they have the talent in house to carry the company forward.

We view ZOES as one of the best small cap growth names. The company is set-up for long-term success for the following reasons:

- Superior brand positioning

- Management philosophy and execution

- Unit opening geographic profile

- Early-stage average unit volumes and returns

FNGN

FNGN is a battleground small cap name that we think is misunderstood and undervalued. FNGN will report 2Q15 earnings on Wednesday, August 5th, after which we will provide our fundamental update.

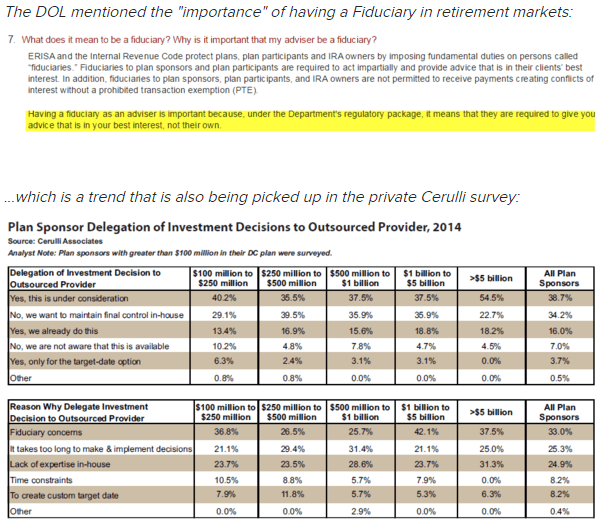

The Department of Labor (DOL) is in the midst of a 75 day comment period for pending adjustments to the handling of retirement accounts and client assets. Currently, the language and verbiage points to broad sweeping principles to ensure low fees, avoiding conflicts of interest/steering, with sweeping adjustments within the IRA markets. Buried within the literature is mention of continued support for independent advice within both the IRA and DC/401K market, which in final form would continue to make the case for independent advisory firms including Financial Engines (FNGN).

While the finalized proposals won't likely take shape until the end of the year, the rule set in current form looks to extend the regulatory tailwind from the 2006 Pension Protection Act, which suggests a default investment alternative to allow for improved investment results (otherwise potentially assigning liability to plan sponsors). We note that the most recent annual Cerulli survey of the retirement market continues to point to "Fiduciary Concerns" as driving delegation of investment decisions to independent 401K advisors in concert with this ongoing regulatory push.

HOLX

HOLX’s earnings release were as good as we expected, and in some spots, much better than our optimistic view.

We’ll have the monthly update for July by Monday morning for our 3D Tomo Tracker. Strength in the Hologic’s Breast Health segment caught analysts off guard, and the questions from the sellside seemed to be searching for a handle on the upside. For their part, management responded by eliminating any disclosure about unit placements or market conversion! Maybe that was a reaction to recent downgrades into their earnings. Given our tracking tools, we don’t really mind less disclosure, but it will be interesting to see how consensus numbers change over the coming days.

Given the move in the price, we did begin to do some work on Hologic’s Diagnostic segment. We touched base with a lab Director who currently does his testing on Hologic/Gen-Probe’s Panther system. During the call management made some positive comments about uptake of the systems and rising utilization per box. Our contact suggested the benefit from the Affordable Care Act was substantial over the last 12 months, pushing volume up to a mid-teens growth rate, but that trends were flattening. But on the positive side Qiagen continues to cede share with an out of date test and the alternatives are primarily Roche and Hologic, but not Cepheid’s system.

The bottom line is that we may be too conservative with our estimates for Diagnostics, which we’ve been assuming treads water from here. However, we’re starting to think there is some incremental acceleration that’s possible, which would be welcome news indeed.

FL

Coming off a period of growth, Foot Locker boosted returns by 2,000 basis points without spending. That productivity improvement was driven by a rationalization of the store base as FL removed duplicate and underperforming stores throughout the U.S. The slide below shows an example where 3 FL store concepts are in the same mall location (North Riverside Park). Over the past 5 years FL has removed these redundancies. Now there are few opportunities left to close or 'rebanner' stores, and no more capital to pull away from this model.

The change was led by Ken Hicks, CEO from 2009 to 2015, who is now gone (retired). His team is still there, but the new plan involves spending to grow, which we see driving down asset returns. That's never a positive for a company's multiple especially when you consider that FL is trading at a peak 16.5x earnings multiple.

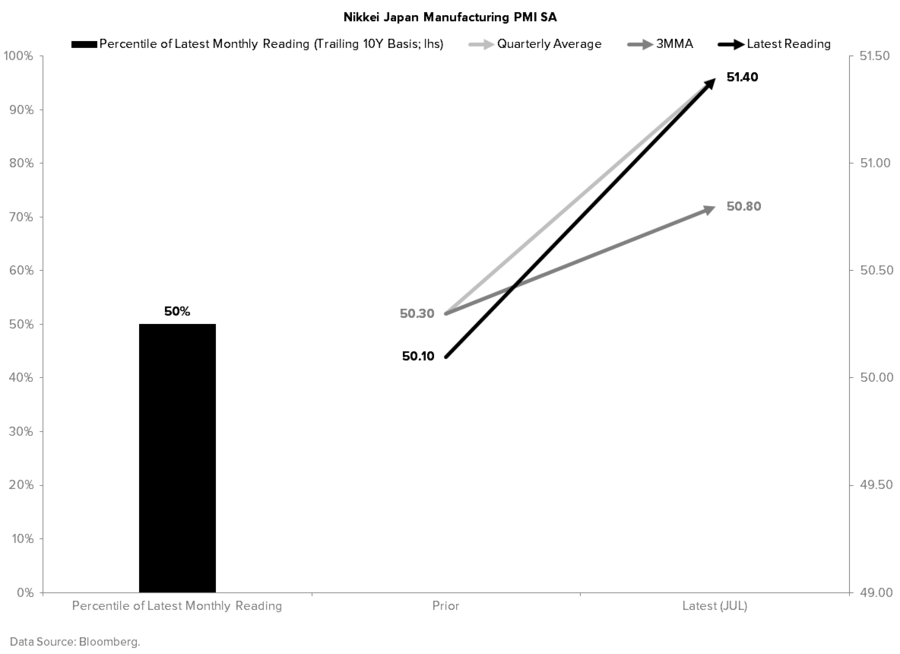

DXJ

Still Working: DXJ Update

Japan – our favorite country exposure on the long side of equities – continues to deliver positive absolute and relative returns and we continue to prefer the hedged exposure offered by the DXJ, given the currency’s inverse correlation to the QQE fueled equity market. Specifically, the DXJ finished up +0.7% on Friday to cap a +1.4% gain for the week. That compares to 1-day and weekly returns of -0.2% and +1.2%, respectively, for the SPY.

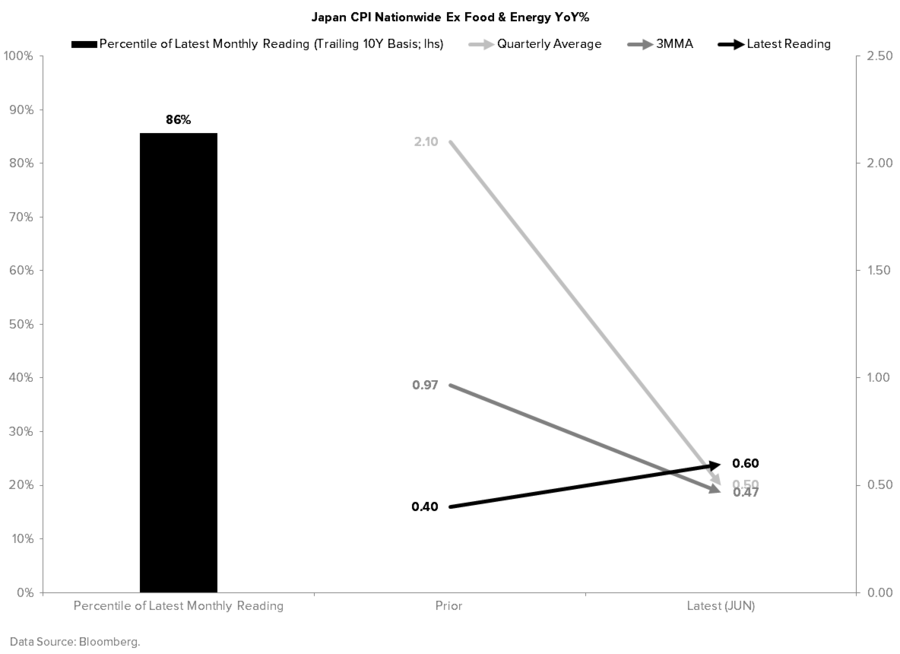

With respect to the key economic data released this week, household spending slowed sharply again in June as core CPI ticked commensurably.

One might think this should lend pause to the BoJ’s drive to perpetuate a sustainable and structural increase in inflation, but the trend in real incomes remains extremely positive, having rebounded in a more-or-less strength line to +2.8% YoY in June from a bottom of -7.1% YoY in April 2014. Rising real incomes is positive on the margin for Japanese equities as it gives the BoJ additional scope to combat the trending deceleration in both reported inflation and inflation expectations. Regarding the latter, Japan’s 10Y breakeven rate is down from its YTD high of 1.12% to 0.96% latest; recall that it has been making a series of lower-highs since peaking at 1.39% in June of last year.

With monetary policy remaining accommodative and set to become incrementally supportive of the Japanese equity market (we anticipate QQE expansion within the next 4-6 months), the positive trend in Japanese manufacturing and trade data is an additional tailwind to the extent such trends are reflected in improving corporate operating metrics. Recall that a structural improvement in the ROEs of Japanese corporations and increased financial engineering are as key to our bullish bias on Japanese stocks as the country’s debt and demographically challenged inability to meet its growth and inflation targets (i.e. perpetual QQE) is.

All told, we reiterate our bullish bias on Japanese equities and continue to see substantial upside over the intermediate-to-long term.

VIRT

VIRT will report 2Q15 earnings on Wednesday, August 5th, after which we will provide our fundamental update.

Our Financials team believes that VIRT is being valued incorrectly by the market. Our main qualm is that the company takes intraday prop risk, but has no tangible equity capital to cover any potential trading losses. We see fair value in the mid-teens (30-40% downside).

PENN

After attending PENN’s analyst day at the Plainridge Casino in Massachusetts our Gaming, Lodging & Leisure Team struggled to find any negative takeaways. The property opened very strong in late June, and the strength continued in July.

We are now raising our win per day per slot assumption to $500 from $400. Terrific highway access, a lower gaming tax rate and garage parking provide a competitive advantage in what seems to be a deeper market than the consensus view. Our 2015 and 2016 estimates are materially above the Street for EBITDA and EPS. Most importantly, we think PENN should generate an ROI of 28% on Plainridge, much higher than the Street anticipates.

PENN has a done a nice job with the new casino (clean bathrooms and ample parking) and it’s showing in the early results. We believe Street estimates for PENN will need to move higher as early as Q3 and certainly for 2016, due in part to the strength of Plainridge. We’re now projecting $340 and $383 million in company EBITDA for 2015 and 2016. Our EPS estimates are $0.66 and $1.10 for 2015 and 2016, respectively - 12% and 16% above the Street, respectively.

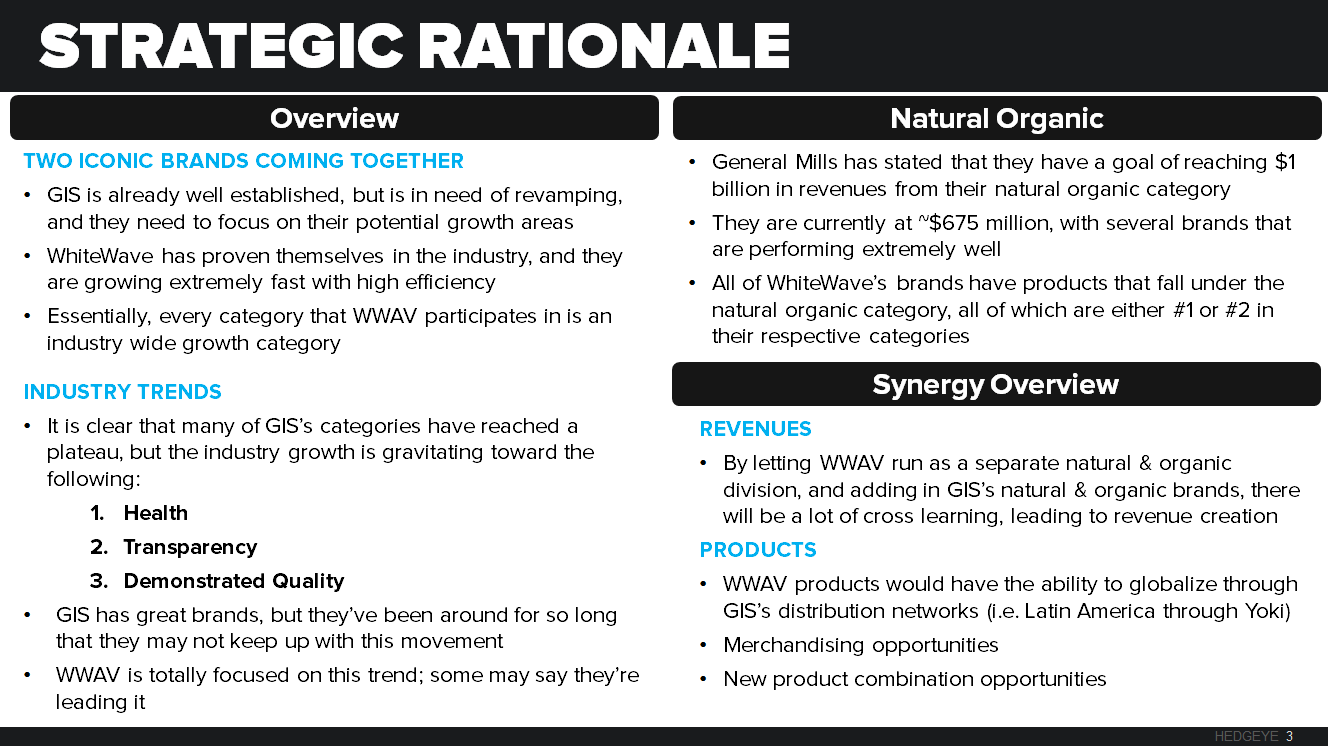

GIS

This Thursday we posted a full note on why GIS should buy WhiteWave Foods (WWAV). This transformational transaction although dilutive would reinvent the way GIS operates forever. We are confident investors will look past the dilution and to the immense amount of growth WWAV would provide.

FY16 Hedgeye Guidance ―

Looking into FY16 we are excited about the possibilities. Management is working hard on their “Consumer First” initiative and making great changes to current product while also introducing new products. Below is not a comprehensive list but some of the biggest things that we are looking forward to this year:

- Yoplait in China

- Gluten-Free Cheerios

- No artificial colors or flavors in the cereal

- Granola innovation / Muesli

- Greek Plenti / Whips

- Original yogurt sugar reduction

- Renovation on Grain Snacks

- Strong push on Natural & Organic products

- Delivering Value to consumer on brands like Totino’s and Hamburger Helper

- Bringing U.S. innovation International

Bottom line is they are still struggling; we don’t want to shy away from that. But the core of the portfolio is growing and management seems to be working tirelessly on implementing changes to grow the rest of the portfolio, especially cereal. We also still believe that to have continued growth into the future a sizeable acquisition or divestiture would be beneficial to the business.

TLT | VNQ | EDV | UUP

We added UUP to investing ideas this week as a largely expected sequential acceleration in GDP from Q1 to Q2 on a seasonally adjusted annual basis pulled forward the market’s expectation for a rate hike which = USD strength. The USD finished positive on the week (+0.50% on Thursday’s print alone)

- U.S. GDP reported Thursday for Q2 came in at +2.3% on a Q/Q seasonally-adjusted annual rate and the market took it as a positive print à rate hike expectations pulled forward.

- Remember that 1) Consensus focuses on this SAAR number and 2) The GDP acceleration came off of an awful Q1 print (Q1 revised to a measly +0.60% for Q1 vs. initially reported -0.20%)

- On a Y/Y basis (crazy Hedgeye speak) GDP for Q2 actually decelerated to +2.3% YY vs. 2.9% prior

- With very difficult base effects in our model for 2H 2015 GDP we expect Q2 data (especially the GDP print) to provide support for the USD

- Our expectation for Y/Y GDP in Q3/Q4 are +1.6% Y/Y (+1.4% Q/Q SAAR) and +1.5% Y/Y (+1.7% Q/Q SAAR) respectively; These prints (Q3 will come in October) will stoke a relatively more dovish FED for a short time (USD headwind) but until then we’ll ride the Q2 data train.