Both General Mills (GIS) and WhiteWave Foods (WWAV) are on the Hedgeye Consumer Staples Best Ideas list as LONGS.

We know what the obvious reaction is going to be to this deal. GIS’s management would never do a deal like this and there is a significant amount of dilution. It’s just not a realistic possibility, or is it? It’s true that this deal would be dilutive, but this is a unique opportunity for a transformational transaction that would overshadow the dilution. Given the strategic rationale for bringing together two high quality companies in the food space, we are confident the street will look past the 10-20% dilution in year one and two, and focus on the long-term potential it would provide GIS.

This is a transformational, portfolio shaping transaction that will change the way GIS operates forever. Acquiring $3.5bn in rapidly growing sales is exactly what we called out GIS needs to do in our GIS Black Book. If GIS were to take on WWAV it would be the beginning of other substantial changes at the company. Management still needs to divest the anchor brands attached to the portfolio, the self-identified 28% of non-priority brands representing $5.4bn in sales.

On a pro-forma basis GIS would overnight become the largest global natural and organic company with $4.2bn in natural & organic revenue. Once the transformation is complete the pro-forma total company would be generating mid-single digit organic volume growth, rather than the low-single digit growth GIS produces on its own.

Naturally, there is also going to be a significant amount of skepticism around the possibility of this deal coming to bear given, GIS’s perceived sleepy corporate culture. At age 61, GIS Chairman and CEO Ken Powell, has a significant opportunity to cement his legacy in the food industry as one of the most dynamic CEO’s.

The following is an overview of how the GIS/WWAV deal would unfold.

COMPANY OVERVIEWS

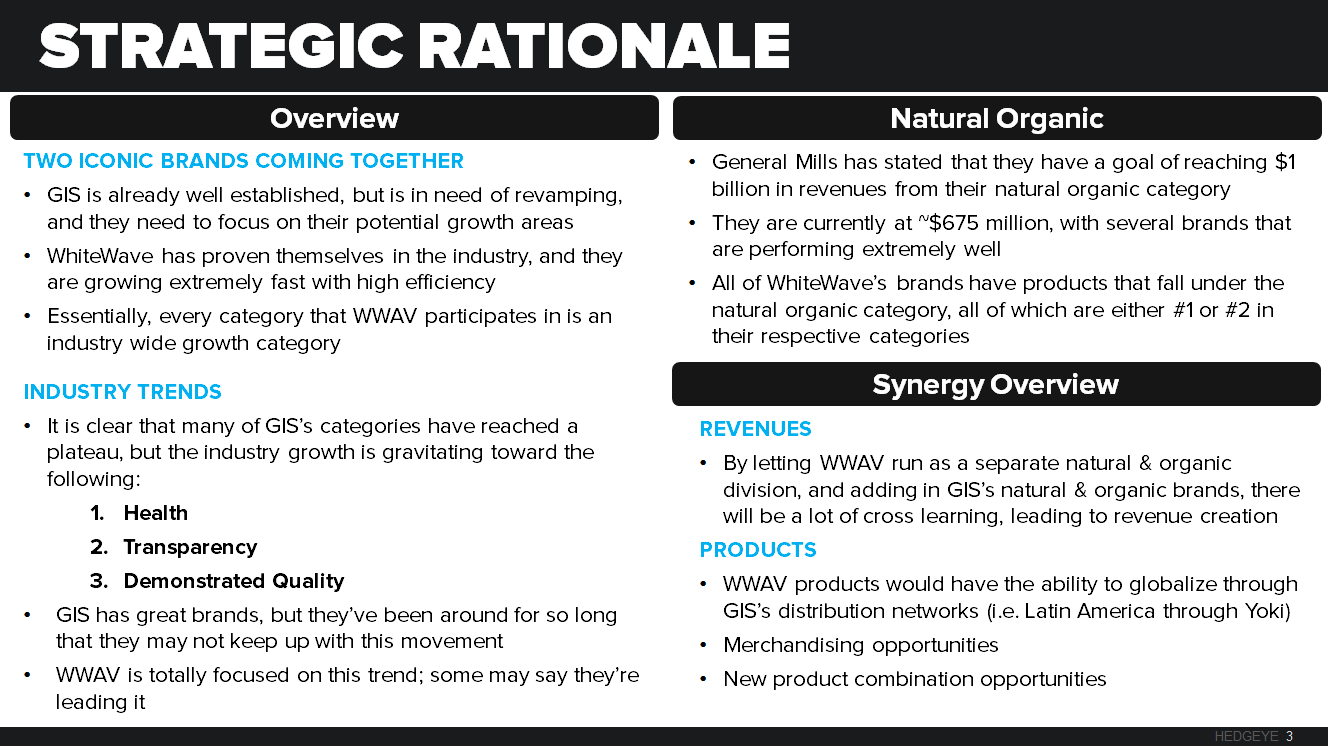

These companies are more similar than people think, just at different stages of maturity. Both operate multinational corporations focused on growth globally. GIS is building out a yogurt business in China, while WWAV recently launched a joint venture in dairy-free drinks under the Silk brand. Although GIS has strong growth brands, the company in total has hit a growth plateau recently and is currently working on growing its portfolio. This is where WWAV comes in, providing immediate growth, and an abundant amount of international expansion possibilities.

STRATEGIC RATIONALE

GIS already plans to get their natural & organic portfolio to $1bn by 2020 organically, this transaction will allow for greater learnings to help GIS’s core portfolio to grow even faster. The perception of GIS will begin to change as they acquire WWAV and divest less desirable brands. Imagine GIS actually being perceived as a health company, the company will gain a lot of appeal from both consumers and Wall Street.

GIS NATURAL & ORGANIC

GIS is going to be a healthier company with or without WWAV. The company has been adamant about changing the consumers perception of their brands by taking out artificial colors and flavors, going gluten free, and innovation towards cleaner ingredient decks.

SYNERGIES

Revenue synergies are going to be a big aspect of this deal. The strong equity that WWAV’s brands have will help to support growth among GIS brands. Cost synergies will be big as well; we imagine some cuts coming from the GIS side, in order to retain the strong talent at WWAV. WWAV knows how to run a natural & organic company and we would hope that instead of absorbing the brands, GIS would create a new division for only natural & organic products and have WWAV personnel run it. We believe this would maximize the benefit.

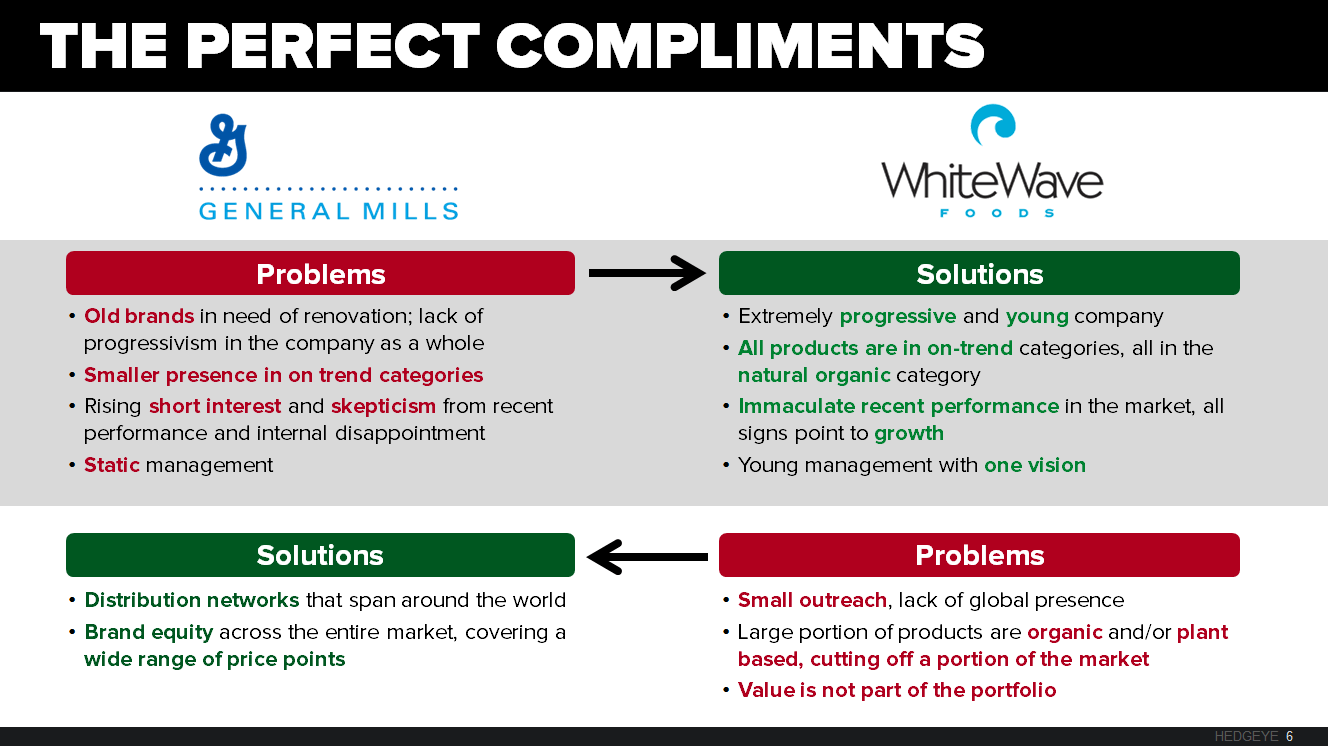

PERFECT COMPLIMENTS

These two companies solve each other’s issues.

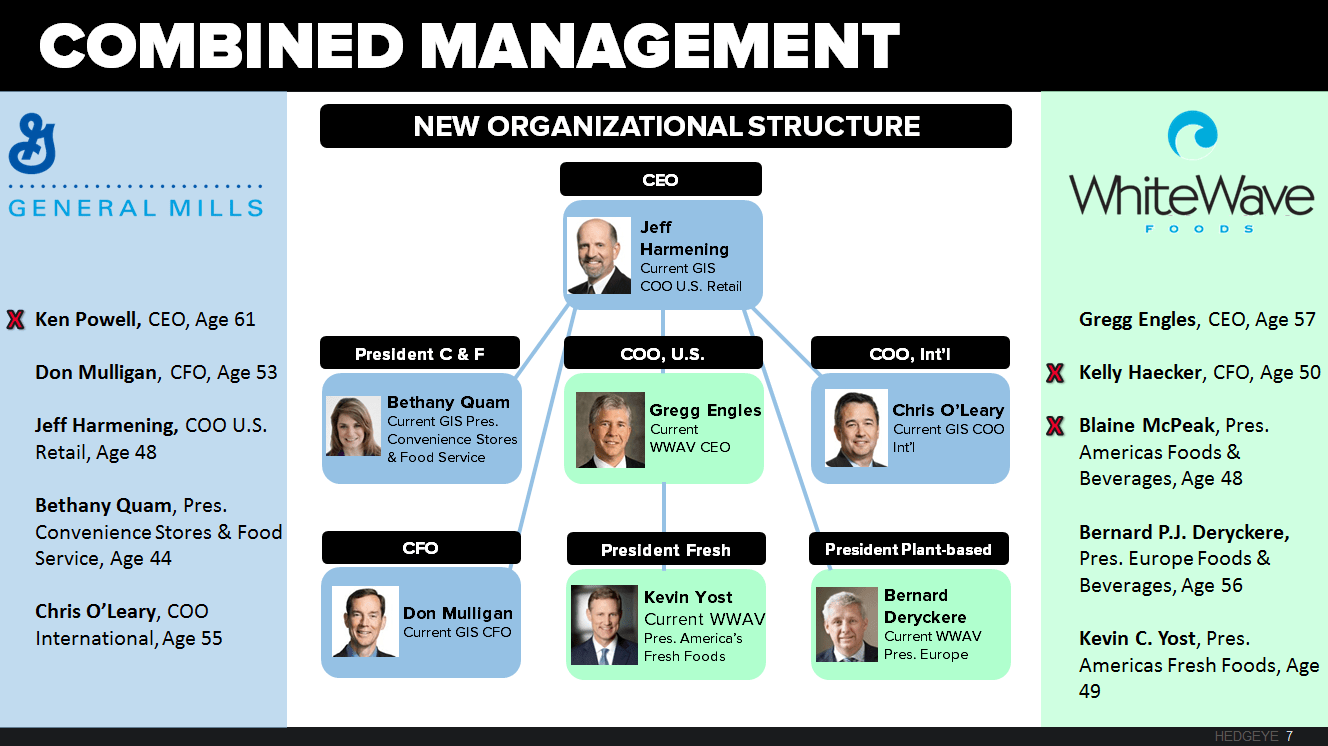

MANAGEMENT TEAM REDESIGN

GIS shouldn’t just want the brands, WWAV has an enormous amount of talent that needs to be retained. Gregg Engles is a phenomenal CEO at WWAV, although he wouldn’t be promoted to CEO at GIS (we think he should some time down the road) he would be a perfect fit as COO of U.S. Retail. A noticeable switch on this chart is the resignation of Ken Powell, current CEO of Chairmen, coupled with a splitting of the CEO and Chairman positions. Jeff Harmening the current COO of U.S. Retail, would work well as the CEO of this improved GIS, he has strong experience across the organization.

This is one of those transactions we get very excited thinking about. The new General Mills would be a powerhouse in the industry with some of the best brands and people the industry has to offer.

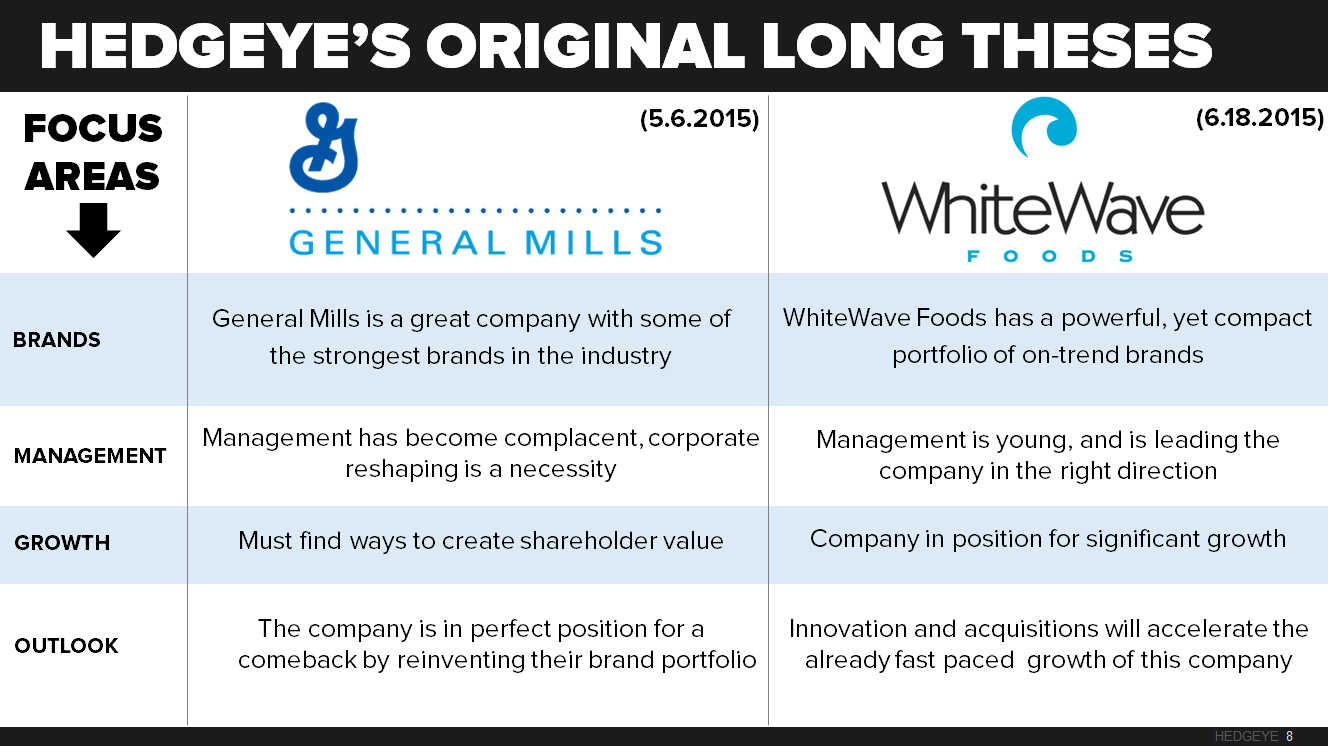

HEDGEYE’S ORIGINAL LONG THESIS

LINKS TO BLACK BOOKS: