Below are Hedgeye analysts’ latest updates on our nine current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each.

Please note we added DXJ (Japanese Stocks) this past week. We also added Foot Locker and removed Deere (both bear side).

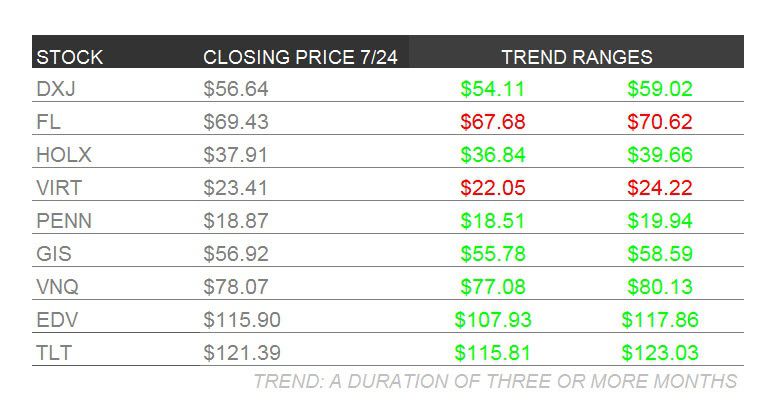

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

HOLX

We shared the following slide during our presentation in our call for institutional clients earlier this week.

Based on our data driven model, and the simple arithmetic of s-curve growth, it looks like the consensus outlook is calling for a steady increase in 3D mammography penetration.

If the market behaves like it did when HOLX helped transition facilities from film mammography to digital, the adoption curve will look exactly as we have it modeled.

If the market adopts 3D even just a little faster (which is likely in our view) the impact to HOLX revenue, EPS, and the share price will be dramatic, as you can see in the table above.

We currently expect the fast part of the adoption curve will take 6.4 years based on our data through June 2015. If the next few months come in better, the pace will begin to fall to 6.25 years (3rd rowin the table) and below. Shortening the adoption time by 3 months at each line in the table drive more revenue, at a high incremental gross profit, and high incremental EPS.

Hologic reports July 29th and we’ll update our positive outlook after the call.

FL

Foot Locker’s RNOA (return on net operating assets) went from 5% to 28% over six years as it pulled capital out of the model (closing stores/re-positioning banners) while boosting productivity and margins to all-time highs. At the same time, its percent of sales from Nike (traffic driver) went up by 2,500 basis points to 72% of COGS (cost of goods sold) – and near 80% of sales.

That’s not going any higher.

Foot Locker’s answer is to become a unit growth story once again and sustain a mid-single digit comp while maintaining the leanest cost structure out of any retailer around. And for all that, the stock is trading at 16.5x forward earnings – an all-time high. The ‘going private’ angle here is moot given its high Nike exposure.

Lastly, the stock is having increasingly muted reactions to good news.

dxj

CEO Keith McCullough added Japanese Stocks to Investing Ideas on Friday afternoon. Click here to read the note. Our senior macro analyst Darius Dale will provide a detailed update next week.

VIRT

A major broker/dealer firm broke ranks this week and initiated research coverage of Virtu Financial with a Sell recommendation. While the rationale for the new rating didn’t highlight our main hangup with the company’s financials, it is a fairly telling sign that a major dealer that interacts with VIRT on a daily basis is also bearish on the fundamental prospects for the company.

Again, our core contention with the firm’s positioning is that with no tangible equity capital that VIRT will have to cover any trading losses in its operations with overnight credit lines which don’t leave an appropriate margin of safety for investors. The company runs its trading book with $245 million of overnight capital and $499 million in equity. However with $715 million in Goodwill, this leaves no liquidity for any mishaps.

VIRT doesn’t report 2Q earnings until August 5th however we will get the latest trading record during the past quarter then which will give investors an indication if the firm’s near flawless daily trading track record is continuing.

PENN

Penn National Gaming reported Q2 profit of $16.9 million on Thursday. The company's profit of 19 cents per share beat analysts' expectations. PENN posted revenue of $701 million in the period, which also beat forecasts.

Shares have climbed 40% since the beginning of the year and 58% over the last 12 months, obviously much higher than the S&P 500.

Gaming, Lodging and Leisure Sector Head Todd Jordan was at Penn National Gaming's investor day yesterday. He will provide a detailed update next week.

GIS

General Mills (GIS) remains on the Hedgeye Consumer Staples Best Ideas list as a LONG.

Key segments across the company are turning the corner and improving performance. Specifically GIS has figured out the yogurt category, after 3 years of struggling with Greek and losing on the core business, management has turned the Yogurt division into a growth segment.

Cereal has obviously been a struggle for all companies participating. Although still down, the trend is looking better, in FY16 we hope to see the switch to Gluten Free Cheerios and other improvement, turn performance around.

FY16 Hedgeye Guidance ―

Looking into FY16 we are excited about the possibilities. Management is working hard on their “Consumer First” initiative and making great changes to current product while also introducing new products. Below is a list of some of the biggest things that we are looking forward to this year:

- Yoplait in China

- Gluten-Free Cheerios

- No artificial colors or flavors in the cereal

- Granola innovation / Muesli

- Greek Plenti / Whips

- Original yogurt sugar reduction

- Renovation on Grain Snacks

- Strong push on Natural & Organic products

- Delivering Value to consumer on brands like Totino’s and Hamburger Helper

- Bringing U.S. innovation International

Bottom line is they are still struggling; we don’t want to shy away from that. But the core of the portfolio is growing and management seems to be working tirelessly on implementing changes to grow the rest of the portfolio, especially cereal. We also still believe that to have continued growth into the future a sizeable acquisition or divestiture would be beneficial to the business.

TLT | VNQ | EDV

Those long of #LowerforLonger enjoyed another solid week of 2%+ gains for TLT and EDV. VNQ followed up last week’s gains with a pullback of equal size, but we received a positive sloth of data this week that confirms our long housing theme, which we’ll focus on below. A positive housing outlook within a bearish rate environment should be positive for VNQ.

With the exception of another positive jobless claims report (lowest level since 1973!) which is empirically late cycle in nature, housing dominated an otherwise light week of economic data in the U.S.

Existing home sales for June reached a new post-housing crisis high:

- Existing home sales totaled 5.49MM units in June (seasonally adjusted annual rate)

- The print marked a 9.6% Y/Y increase (+3.2% sequentially from May)

- As an indicator to what demographic is driving the strength, existing home sales to 1st time buyers rose +17.4% Y/Y

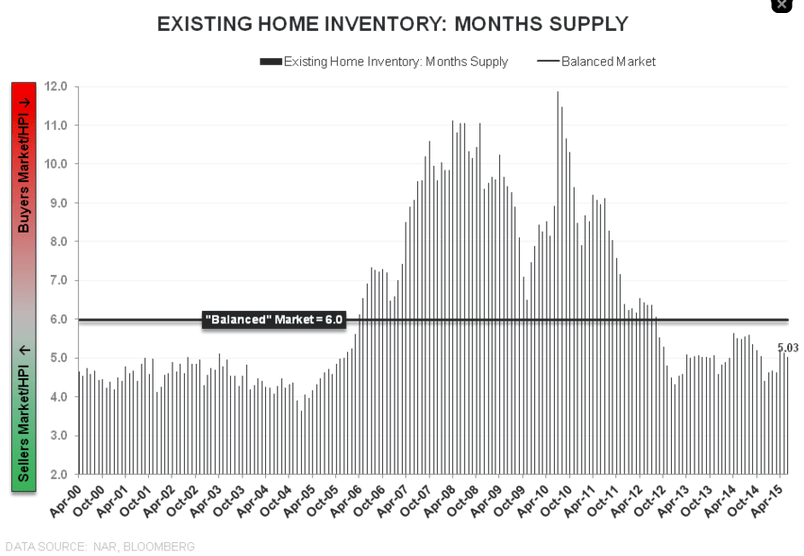

- An excess of housing sales over available inventory fell -2.2% -2.2% in June. A tighter supply should continue to drive the increase in housing price trends

New Home Sales for June came in weaker than expected, but the intermediate to longer term picture has been one of immense improvement:

- New home sales came in at 482K vs. expectations of 548K (546K prior)

- New Home Sales declined -6.8% for June but the intermediate to long term trend remains intact which is why we evaluate marginal changes on a YY comp basis. New Home Sales numbers are still trending up double digits from 2014