A look at good, neutral, or bad numbers…

MCD is scheduled to report October same-store sales numbers before the market opens on Monday. Management provided the following outlook for October sales trends on its 3Q09 earnings call:

“As we move through October, consolidated comparable sales remain positive with Europe and APMEA contributing strong results. In the U.S., despite continued gains in market share and advancement in our industry-leading position, we're expecting flat to slightly negative October comps. This is due in part to the current economic environment and strong results a year ago. We do not believe, however, that this is a change in the overall trend in performance in the U.S.”

Taking those comments into consideration, I wanted to provide comparable sales ranges for each geographic segment as a benchmark of what I think would be GOOD, NEUTRAL, or BAD results based largely on 2-year average trends.

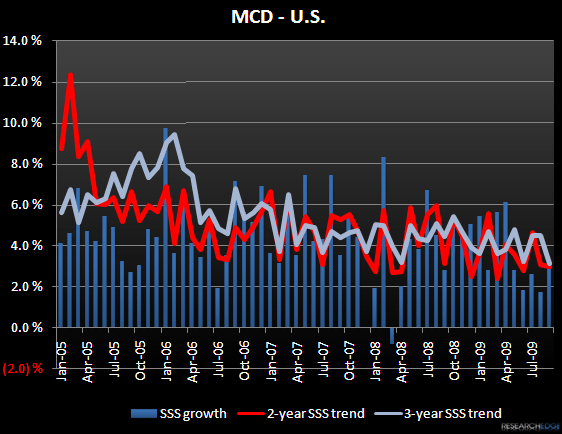

U.S. (facing a relatively difficult +5.3% comparison from last year):

GOOD: Any number better than flat would signal that the company’s trends came in better than management’s guidance. The company needs to report at least +0.6% to just maintain its 2-year average trends from August and September. So this month, even a GOOD result will most likely point to a continued deceleration in 2-year average trends.

NEUTRAL: -1% to flat would signal that full month trends were in line with management’s guidance. So this range of results, though neutral from an investor sentiment perspective as it relates to expectations, is not a favorable sign for current trends. MCD has not reported a decline in U.S. same-store sales growth since March 2008. This neutral range also implies a continued deceleration in 2-year average trends.

BAD: below -1% would be worse than expectations as set by management. A -1% number points to an 85 bp sequential decline in 2-year average trends. A -1.5% or below would be very BAD as it implies a 2-year average trend of less than 2%. MCD has not posted 2-year average trends below that level since early 2003.

Europe (facing a relatively tough +9.8% comparison from last year):

GOOD: +4.5% or better would signal an acceleration in 2-year average trends from September levels and a return to the 7%-plus levels MCD has experienced for the greater part of the year.

NEUTRAL: +2% to +4.5% would point to 2-year average trends that are about even with to slightly better than what we saw in September. Investors are most likely expecting some sequential improvement as management said Europe and APMEA are “contributing strong results” in October.

BAD: below +2% would imply a slight slowdown in 2-year average trends and anything below 1% would be viewed as really BAD as it would signal a return in 2-year average trends to the low reported June levels.

APMEA (facing a relatively difficult +11.5% comparison from last year):

GOOD: +2.0% or better would signal an acceleration in 2-year average trends. A +2.5% or better would be really GOOD as it would imply a return to the 7%-plus 2-year average trend we saw earlier in the year.

NEUTRAL: flat to +2% would point to 2-year average trends that are consistent with to slightly better than what we saw in September. Like Europe, based on management comments, investors are most likely expecting some sequential improvement in APMEA.

BAD: any number below a flat result would imply that 2-year average trends have slowed somewhat. Although MCD reported a negative comp in August, I think the sticker shock associated with seeing this segment go negative again would be bad. Any number below -2% would be really BAD as it would imply a return to the softened 2-year average levels we saw in June, July and August.