With all of the geopolitical hurdles that must be jumped, we expect a significant increase in crude exports to be delayed until early to mid-2016 at the earliest.

Below we outline the key catalysts to watch in the Iranian Nuclear Deal which was endorsed by the U.N. on Monday. Today Iran’s Minister of Industry, Mohammad Reza Nematzadeh, trumpeted a $185Bn investment target in oil and gas by 2020. While Iran’s energy resources are immense, the timetable and feasibility is uncertain at this point. With a myriad of undecipherable noise around the nuclear deal currently we hope to provide a more straightforward overview of the most important developments to watch:

- Can Congress pass enough votes in the next ~50days to avoid a presidential veto (2/3rds majority)? Likely not.

Congress provides the statutory basis for most U.S. sanctions. However, the executive branch is the party responsible for interpretation and implementation. Most importantly, POTUS has the authority to waive all or some of any repealed measures from Congress.

In May, President Obama signed into law provisions for congressional review that place restrictions on his prerogative to waive sanctions. Under this law, the House and Senate foreign relations committees have 60 days to review the agreement. During this 60 day period, Obama cannot loosen sanctions. However, for Congress to derail an agreement, it would not only have to vote it down but muster a two-thirds majority to override a presidential veto.

- If all goes smoothly, what will it take for Iran to prove to the IEAE (International Atomic Energy Association) that it has taken steps to reduce its stockpiles of fissile materials and centrifuges?

In 1974, Iran signed the IAEA Safeguards Agreement. Under the agreement, it promised to never become a nuclear-armed state. In the early 2000s, indications of work on Uranium enrichment renewed international concerns which started several rounds of initial sanctions from the U.N., EU, and U.S. attempting to block Iran’s access to the necessary materials needed to develop nuclear capabilities. The root of current Iranian Sanctions dates back to 2005 when the IAEA (International Atomic Energy Association), part of the U.N., found that Tehran was not compliant with its international obligations. The U.S., U.N., and EU have since hit Iran with a multitude of sanctions which have had crippling effects on Iran’s access to international capital.

Some sanctions will be lifted if Iran can prove to the IAEA that it has taken steps to reduce its stockpiles of fissile materials and centrifuges. The beginning of this proving period won’t commence for at least several months.

- When will Iranian crude potentially be released onto global markets?

In November of 2013, Iran and the P5+1 signed the JPA Agreement (joint plan of action) that provided some sanctions relief and access to $4.2Bn in previously frozen assets. Tehran agreed to limit uranium enrichment while permitting international inspectors to access geographical sites of interest.

This joint plan of action capped Iran’s crude exports at 1.1MM B/D (they are right at 1.1MM B/D in exports currently, down from 2.4MM B/D as recently as 2007).

Washington and Brussels will keep the terms of the JPA in effect until the IAEA has verified that Iran has followed through on an agreed-upon set of steps to limit its nuclear program, which, as mentioned, will likely come several months after the July 14 agreement.

Richard Nephew is the Program Director for Economic Statecraft, Sanctions and Energy Markets at the Center on Global Energy Policy at Columbia. He outlined the lengthy steps needed just for Iran to prove its compliance with the IAEA before most IOCs can even begin their capital plans in a REPORT last week.

“First, the agreement involves an extensive procedure for ascertaining the support of home legislative and other legal bodies for it. In the US system, this will take at least 30-60 days as Congress will need to receive the text of the deal, hold hearings on it, and decide what to do.

Second, the implementation will itself take months. Iran’s list of nuclear steps is long, as is appropriate considering they are the party in need of building the most confidence. I’ve noted for a long time that removal and storage of centrifuges will be the long-pole in the timing tent, and nothing in the text contradicts this. Based on the schedule in the document, all of this work will not even start until after 90 days from today (the end of October) and it will take months from that point to fully execute the remaining changes to Iran’s nuclear program.

Third, sanctions relief itself will not flow until these nuclear steps are completed.”

- Will Iran Change the incentive structure for IOCs to make the riskiness of fixed investment worthwhile? Even if IOCs take the plunge

The National Iranian Oil Company (NOIC) is responsible for all upstream oil and nat. gas projects. The Iranian constitution prohibits foreign or private ownership of natural resources. However, international oil companies can participate in the exploration and development phases through buyback contracts:

Here’s how it works currently…

An IOC puts up its own capital through an Iranian subsidiary (service-type contract). After the project is developed and the field is producing, the projects operatorship refers back to NIOC or relevant subsidiary. IOC gets no equity rights and NIOC uses oil and gas revs to pay back IOC for capital cost. The annual repayment rates are set at a pre-determined percentage of the field’s production at a rate of return usually in the 12-17% range.

------

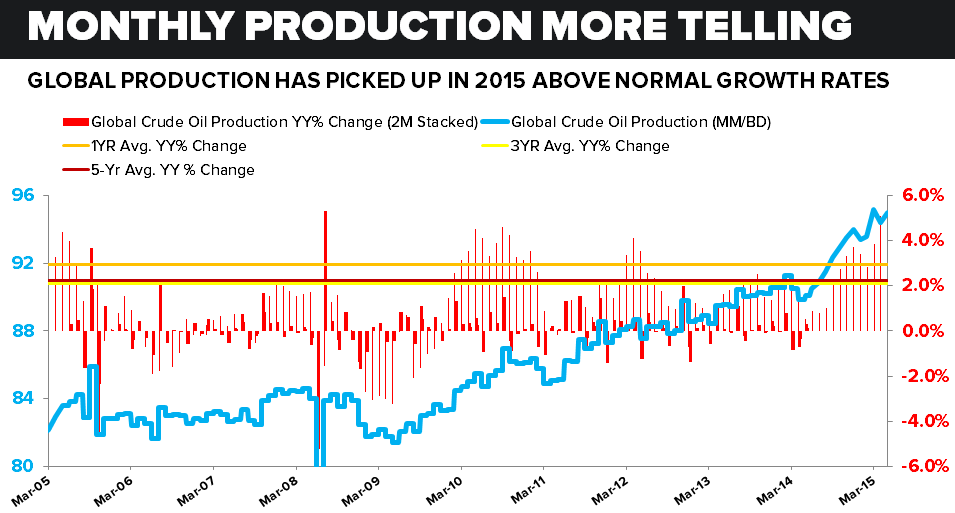

A quick look at global production will tell you that a surplus of crude oil is still coming out of the ground at an increasing rate globally. While a reversal in the USD from March to June and signs of declining U.S. production gave the market a psychological boost, much of the production increase has come from OPEC members, Iran included.

Although Iranian exports are capped at 1.1MM B/D under current sanctions, Iranian crude production has increased by double digits YY and they have an estimated 20MM barrels in storage, ready to release onto the global market when sanctions are lifted. Iran has used its domestically produced crude by satisfying a much higher percentage of its growing energy needs internally. With that being said, we believe it will take an extended period of time before exports pick-up. The Iranian catalyst adding to the global supply picture is more noise than anything for now.

Global Production Picture: Crude Everywhere

Sanctions Effect on the Iranian Economy:

- Iran has not had a new oil field enter production since 2007

- Nearly all western companies have pulled investment

- Few Chinese and Russian Companies are still participating (CNPC, Sinopec, PEDCO)

Trade Impact:

- Iranian crude oil and condensate exports have dropped from 2.5MM B/D in 2011 to 1.1 MM B/D in 2013 due to tighter U.S. and European sanctions

- In 2012 came the insurance and re-insurance bans from the E.U. (European insurers underwrite the majority of insurance policies for the global tanker fleet).

Iranian crude sales, even in Asia, were impeded by the insurance ban. Iranian exports dropped to less than 1MM B/D in July 2012 as Japanese, Chinese, Korean, and Indian buyers scrambled to find insurance alternatives.

Fiscal and Currency Impacts:

- Value of the Rial declined by 56% between January 2012 and January 2014, a time in which inflation reached 40%

- The IMF estimates that Iran's break-even point, the price per barrel at which the country can balance its budget, is $92.50.

- Iran’s energy prices are heavily subsidized (particularly gasoline). At the end of 2010 the government initiated the first phase of subsidy reform, decreasing the subsidies on energy prices to discourage waste. Subsidies have been a huge fiscal drag.

- Oil production, given the lack of capital investment, has also declined significantly

Reworking the Addressable Market:

- Iran has now become somewhat of a closed energy economy for the time being. Growing domestic demand needs have been met internally. The country has continued to increase its refining capacity

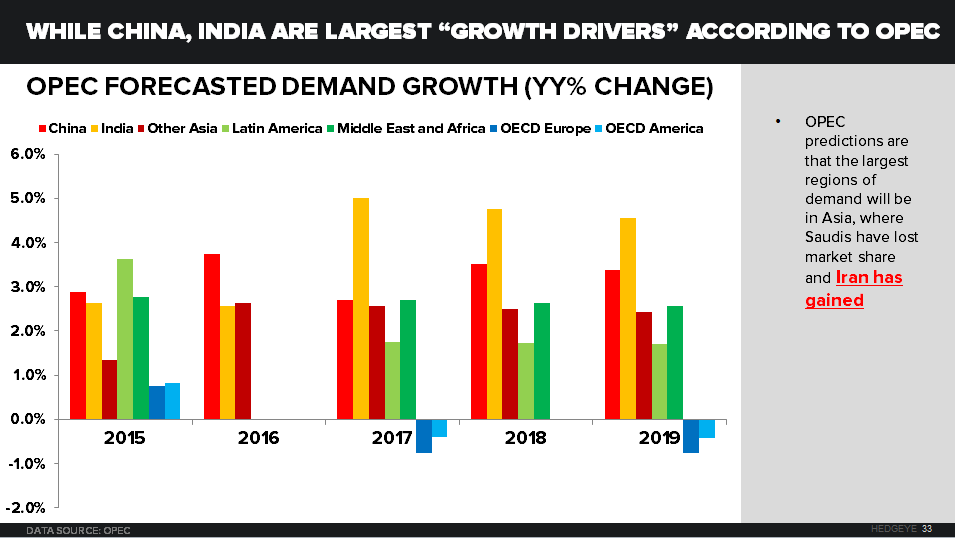

- Meanwhile, Iran has found opportunity in the highest growing regions; Iran has refocused its key customers to Asia and India where the highest global demand rates are forecasted

Energy Potential

The potential in the energy space in Iran is immense, and Iran’s potential trading partners are not limited to high growth, eastern countries. A year before the 2012 sanctions, the EU was the largest importer of Iranian oil, averaging 600,000 barrels per day, according to the Congressional Research Service) :

- 4th largest proved crude oil reserves (10% of global crude reserves)

- 2nd-largest natural gas reserves (17% of world’s proved natural gas reserves (2nd only to Russia)

- Despite the fixed investment crippling sanctions, Iran still ranks among the top 10 oil producers and top 5 natural gas producers. Crude oil production is up double digits Y/Y (+370K B/D)

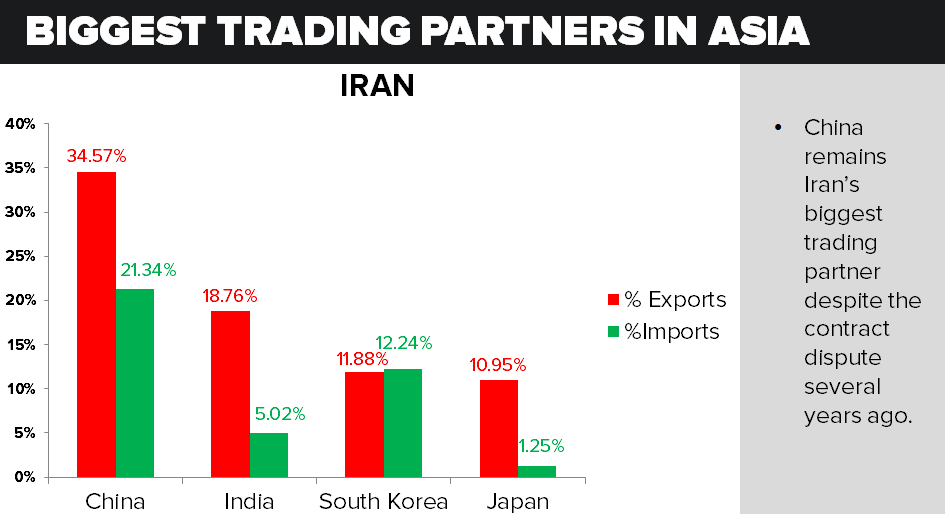

- Almost all of Iran’s export increases have been to China and India, and other Asian countries

As mentioned previously, with all of the geopolitical hurdles that must be jumped, we expect a major increase in exports to be delayed until mid-2016 at the earliest. Even then, the risk for IOCs is immense should Iran fail to comply with strict requirements from the IAEA. Sanctions relief will permit new business with Iran, but uncertainty over Iranian compliance and US politics will deter long-term deals for the next 18 months. But, if these steps cross the sanctions line, the Obama Administration has made clear that it will be forced to act which could provide a huge risk for capital that is tied-up.

Ben Ryan

Analyst