overview

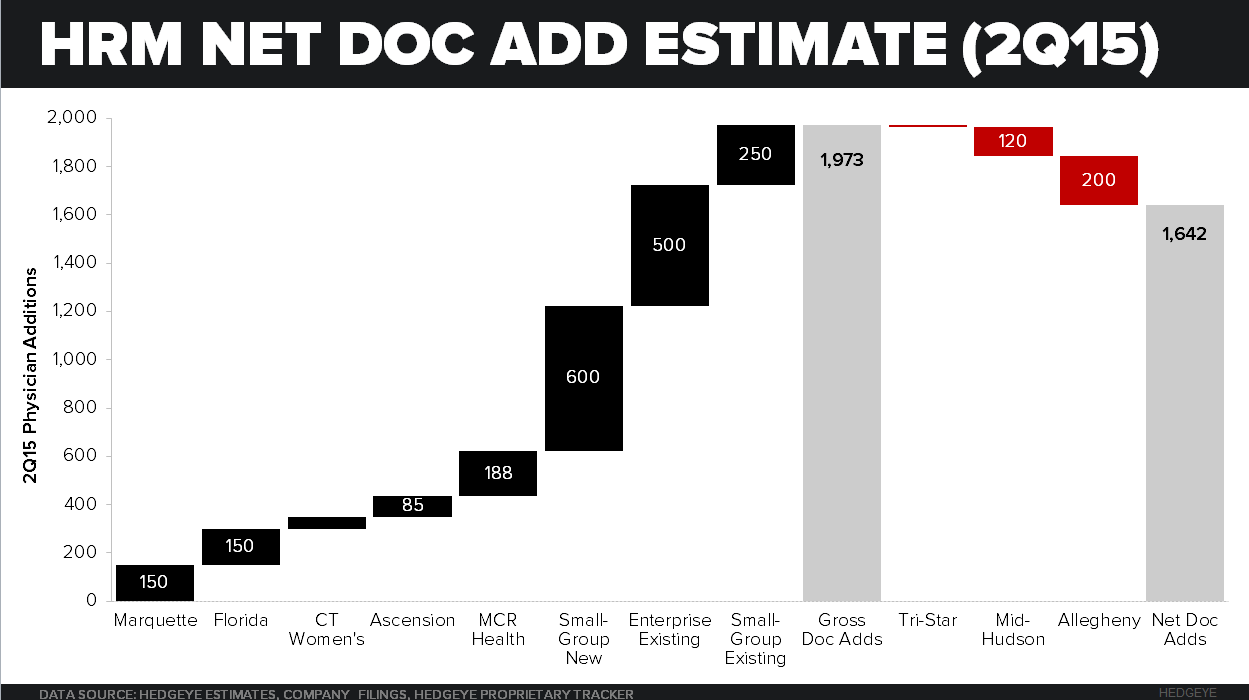

StreetAccount consensus estimates for Q2 net physician adds were just released and they look reasonable. Relative to consensus, our estimate comes within a margin of error for athenaCollector and athenaClinicals, which are the most important products when gauging the health of the business. We are ~500 lower for athenaCommunicator after adjusting our mix assumptions due to several quarters of coming in higher than actual results. However, we don't think it will make a difference as our model is forecasting above consensus Sales and Non-GAAP EPS of $229.3 mill ($227.0 mill Consensus) and $0.30 ($0.25 Consensus), respectively. Chart above above shows the build up and break down of how we arrived at the net physician count for the quarter.

We will get into the details of our process and provide a comprehensive review of our long thesis in a Best Idea Update Call tomorrow at 11:00 am ET. As a reminder, the company will be reporting earnings after the close that day.

key metrics

- athenaCollector

- Consensus 1,697 vs HRM 1,642

- athenaClinicals

- Consensus 1,077 vs HRM 1,154

- athenaCommunicator

- Consensus 1,907 vs HRM 1,415

Please call or email with questions.

Thomas Tobin

Managing Director

@HedgeyeHC

Andrew Freedman

Analyst

@HedgeyeHIT