Chipotle is on the Hedgeye Restaurants Best Ideas list as a LONG.

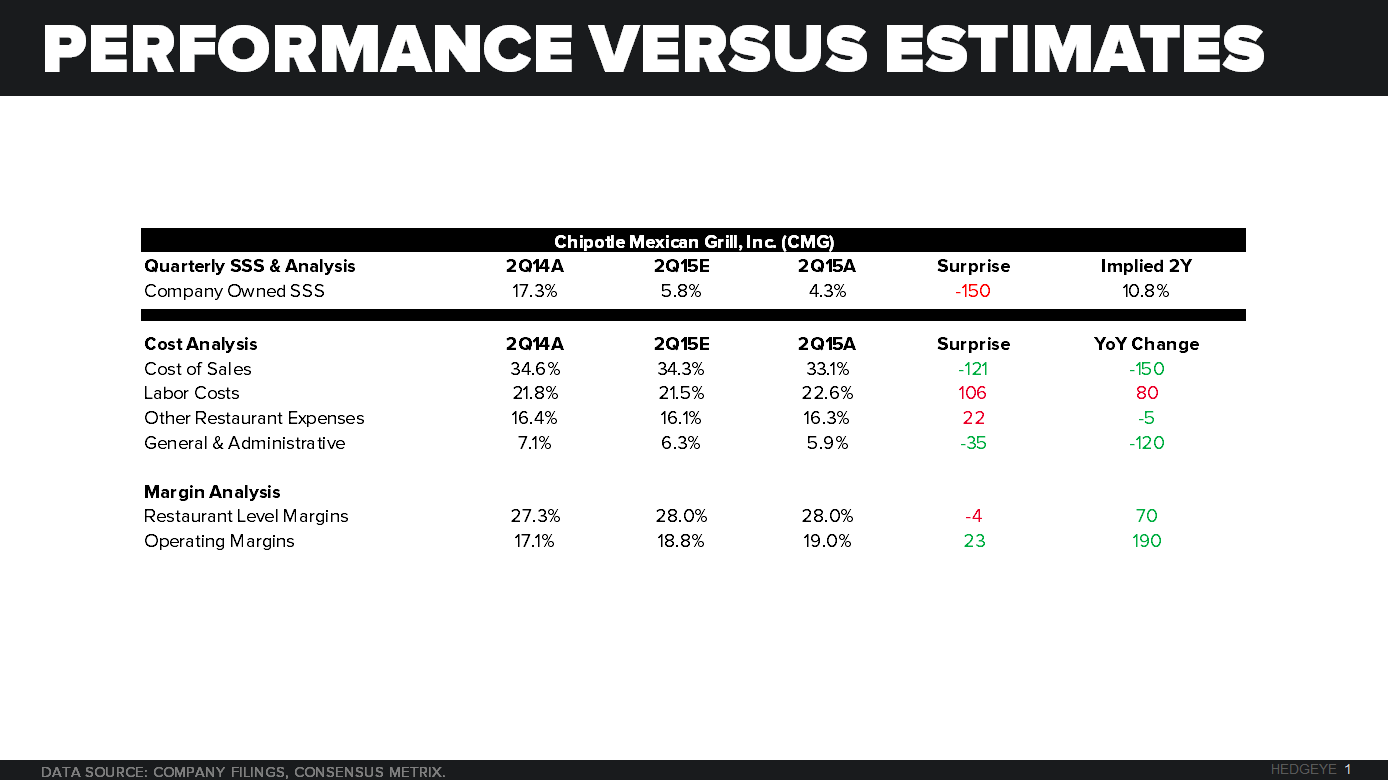

Chipotle (CMG) delivered an impressive 2Q15 when you digest the numbers and get past the same-store sales comp miss. Reported revenue was $1.20B missing slightly versus consensus estimates of $1.22B. Same-store sales (SSS) were +4.3% missing consensus estimates of +5.8% by 150 basis points. The build-up of the comp consisted of +4% price, traffic was slightly negative at -0.3% but offset by +0.6% mix driven by catering and kids meals. Diligent management of cost of sales enabled management to deliver a bottom line beat with reported EPS of $4.45 versus consensus estimates of $4.43.

CMG maintained its full-year 2015 guidance for:

- Comps of low-to-mid-single digits

- Unit development of 190 to 205

Given current trends and the outlook for the balance of 2015 the current consensus estimate for EPS of $17.34 appears to be conservative.

A few things that impacted the quarter:

- Poor management of the labor schedule as teams work to integrate the new software caused a $0.16 impact to EPS in Q2. This is expected to be resolved through Q3 and by Q4 management expects to make up some of this headwind.

- Regulatory calls for higher wages, CMG already pays above minimum wage, but to continue to maintain the high quality workforce, they need to stay above it.

- Absence of carnitas is obviously still an issue but with a new supplier online CMG expects to have all restaurants loaded with pork by early Q4. No bounce back from carnitas has been included in company guidance, providing possibility of further upside.

- Commodity inflation, Avocados sourced from California and Beef system-wide will add pressure to the cost of sales line item, but management is adamant to try to pass some of the cost onto the customers.

Although traffic was negative for the quarter management stated that it has turned positive in the low-single digit range in July. We continue to be encouraged by Chipotle’s continued robust growth driven by strong employees and one of the most loyal fan bases. The opportunistic share buyback program will continue to support this stock, as management steers it towards growth for many years to come.

Below is a look at CMG’s performance versus a year ago and consensus estimates for this quarter. Please note that green is positive performance, while red is negative performance.