General Mills is on the Hedgeye Consumer Staples Best Ideas list as a LONG.

The rumors keep rolling in on the expected divestiture of their Green Giant assets. With the latest rumors that Bonduelle is in discussions with Centerview to team up on a bid for Green Giant, reported by Reuters. Bonduelle is a France based company, but owns manufacturing facilities in Canada that co-pack for the Green Giant business.

This is further confirmation that GIS is still active in the deal process. After just closing out their fiscal year 2015 at the end of May, teams around the company are freed up to conduct a divestiture. Year-end tends to be a strenuous time at manufacturing companies as its all hand on deck from supply chain and sourcing planning volumes for next year, and finance preparing the numbers. It’s no surprise that the sale process probably got pushed till after the year closed.

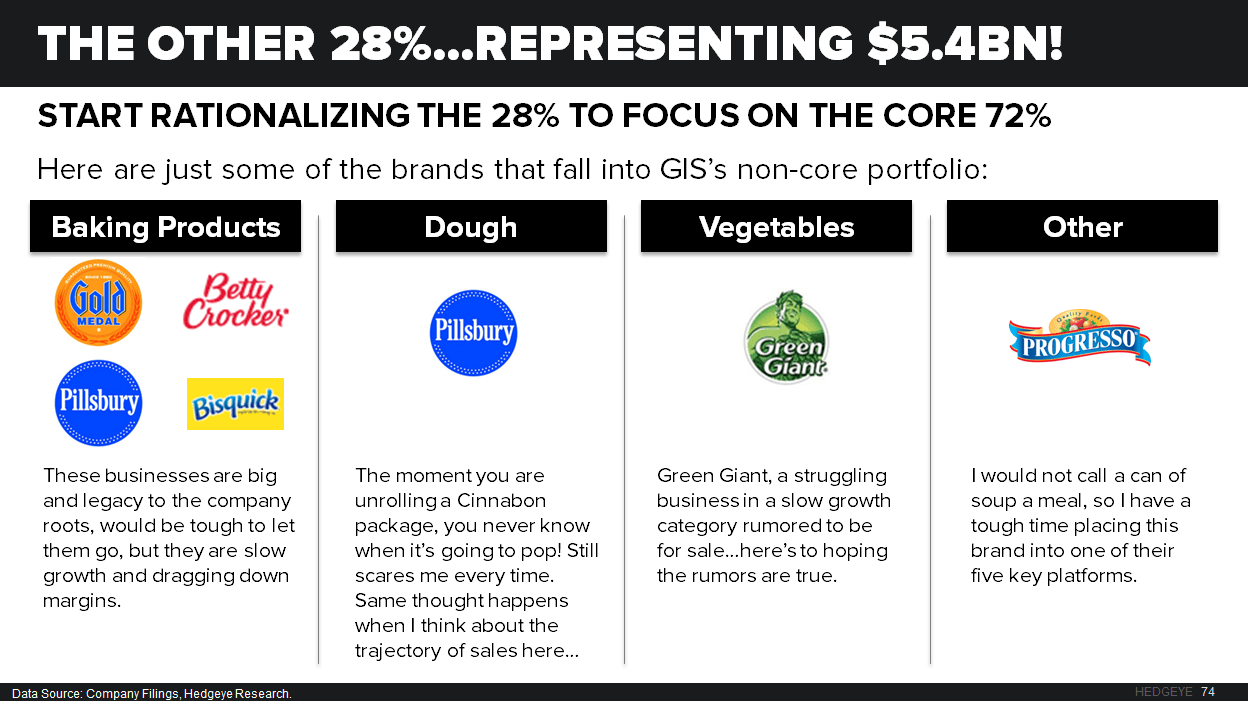

General Mills needs to divest tired assets, and Green Giant is one of the worst performers in the portfolio and we at Hedgeye will be glad to see it go to someone else. Below is a chart from our GIS Black Book that outlines “the other 28%” of assets that management has labeled as non-core.

We hope to see more divestitures come down the pipe, and an acquisition or two to tack some growth onto the portfolio. We predict FY2016 will be a busy portfolio shaping year.