Below are Hedgeye analysts’ latest updates on our EIGHT current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each.

Please note we added Hologic and removed Kate Spade this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

holx

Hedgeye Healthcare Sector Head Tom Tobin is hosting a call with our institutional subscribers this coming Wednesday to discuss Hologic’s path to $50... and higher.

Tobin first added HOLX to the Hedgeye Best Idea List as a long in April 2014 when the stock was in the low $20s. Since then, our original thesis has played out, with the stock doubling as we predicted, and many of the fundamental and sentiment drivers maturing on schedule. We will review the path into the $50s ahead of HOLX earnings report July 29.

ROOM TO RUN, EVEN FROM HERE

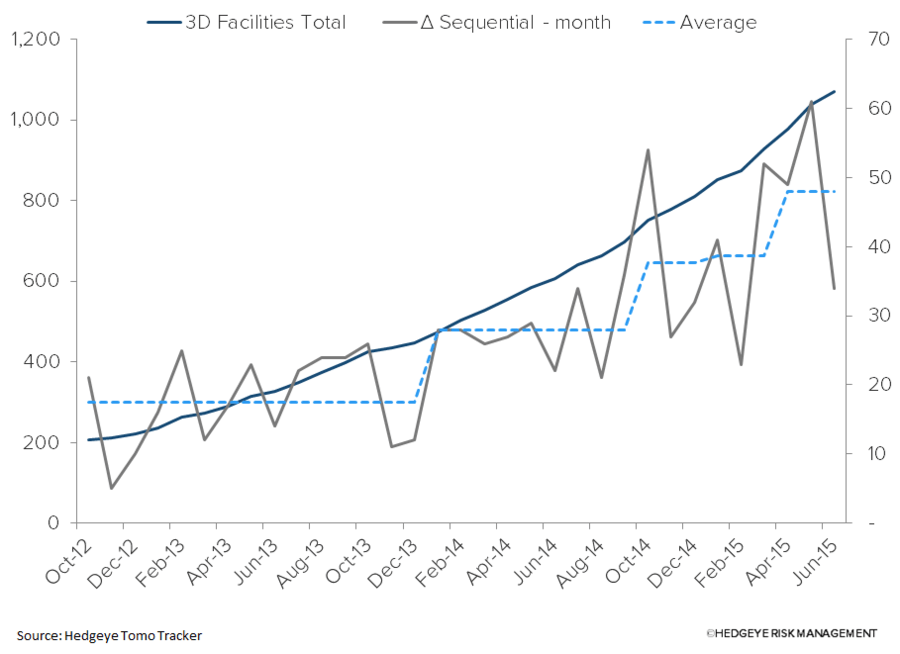

The sensitivity table below makes use of our s-curve forecast model that is based on MQSA and our monthly count of 3D facilities published in the Tomo Tracker. As we've published recently, consensus Breast Health revenue numbers are low compared to our model. However, despite the large gap between our estimate and consensus, we view our estimates as conservative.

As the table shows, if we accelerate the pace of adoption by even very small increments, the impact to revenue, EPS and valuation is substantial.

3D TOMO TRACKER

Below are the monthly 3D Tomo Tracker update charts through June. Our data on the facility counts with a 3D Tomo system allow us to update and forecast 3D adoption. Our s-curve model currently has a variance of 0.13% between predicted penetration and actual facility adoption between September 2012 and June 2015. As seen in the revenue build table below, we believe Breast Health will drive substantial upside in the coming quarters beginning F3Q15 (Jun).

virt

Shares of newly public proprietary trader Virtu continue to broadly drift higher as the drama in the European Union pushes up volatility measures spurring trading volume. That being said the market has awarded VIRT stock a valuation that ignores the fact that while more volume does beget more opportunities for the firm’s algo book, that volume is simply not riskless and that eventually VIRT will have more trading losses in its operations.

This will not be comforting for investors as the company has no tangible equity capital as of last quarter and thus any trading deficit will have to be financed with overnight credit lines (of which the firm only has $70 million committed currently). We think the stock is trading solely on its historical track record of only 1 day of trading losses in the four year period from 2009 to 2012 disclosed in its recent S-1 IPO filing.

While an undoubtedly venerable statistic, we think the firm benefited from a very low volatility environment during that time and that increased vol in the current period will create a choppier revenue distribution for VIRT. We see fair value in the mid teens or 30-40% downside, as the current exchange type valuation (which are companies with riskless trading operations) normalizes lower.

VIRT is currently trading in line with exchange sector because of its recently disclosed historical daily trading track record. We think this track record benefited from abnormally low volatility and as vol normalizes higher, that the firm will experience more losing trading days which will compress the firm’s current excessive valuation.

PENN

According to Gaming, Lodging and Leisure Sector Head Todd Jordan, additional state gaming agencies have reported revenues for the month of June. The good news here is that Penn National Gaming remains on track to beat second quarter estimates this Tuesday July 23rd.

In addition, PENN will be hosting an investor day on July 24th. We will be there and communicate any noteworthy color and developments.

Bottom line? The company remains one of our favorite names on the long side and boasts the best new unit growth story in domestic gaming.

GIS

The General continues to make tough calls as they work to further streamline their manufacturing footprint as part of Project Century. This week, announcing the closure of two plants, one in West Chicago, IL and the other in Joplin, MO, eliminating approximately 620 positions in the process. West Chicago produced cereal and dry dinner products for the U.S. Retail organization, while the Joplin facility was acquired as part of the Annie’s acquisition and produced snacks. Because of union negotiations management is expecting these actions to be fully executed by fiscal 2019.

We view this as a big positive for the company as they go to a more nimble asset light model, which will save on capex and allow it to be allocated to higher growth product platforms.

FY16 Hedgeye Guidance ―

Looking into FY16 we are excited about the possibilities. Management is working hard on their “Consumer First” initiative and making great changes to current product while also introducing new products. Below is not a comprehensive list but some of the biggest things that we are looking forward to this year:

- Yoplait in China

- Gluten-Free Cheerios

- No artificial colors or flavors in the cereal

- Granola innovation / Muesli

- Greek Plenti / Whips

- Original yogurt sugar reduction

- Renovation on Grain Snacks

- Strong push on Natural & Organic products

- Delivering Value to consumer on brands like Totino’s and Hamburger Helper

- Bringing U.S. innovation International

Bottom line is they are still struggling; we don’t want to shy away from that. But the core of the portfolio is growing and management seems to be working tirelessly on implementing changes to grow the rest of the portfolio, especially cereal. We also still believe that to have continued growth into the future a sizeable acquisition or divestiture would be beneficial to the business.

de

The only thing worse than forecasting a stock is forecasting a stock based on a commodity that is dependent on the weather. Flooding and drought conditions in key farming areas has helped to reduce expected crop yields, pushing grain prices higher in recent weeks.

More importantly, the Association of Equipment Manufacturers’ monthly retail tractor sales showed continuing deterioration for the month of June as seen in the chart below.

While higher crop prices is the key short-term risk to our bearish DE view, US growing conditions are likely still pretty favorable. The next USDA crop progress report is due out on Monday, July 20th.

TLT | VNQ | EDV

After an awful retail sales print on Tuesday, the confluence of growth slowing data reared its ugly head Friday with a +0.1% year-over-year headline CPI print for June and a UofMich consumer sentiment reading that declined to 93.3 from 96.1 in May.

Note that a +0.1% inflation rate is a heck of a long way from the Fed’s 2% target.

These two prints were successful in taking the 10-Year Treasury yield down 10 basis points from Monday’s highs to finish the week at 2.35%.

We remain one of the lonely bulls on Treasury bonds (bearish on yields) via TLT, EDV, VNQ.

Weakness in retail sales, small business confidence, and UofM confidence is significant because household spending (consumer-led GDP contributor) had been a positive surprise for May. Gains in personal income and spending growth helped combat what has (and continues to be) an awful looking investment and manufacturing picture in the U.S. (early cycle): Industrial Production, factory orders, durable goods, Manufacturing PMI.

We are now learning that the positive, consumer-driven data for May will not turn into a new trend. If anything, it’s the opposite despite (late-cycle strength is normal):

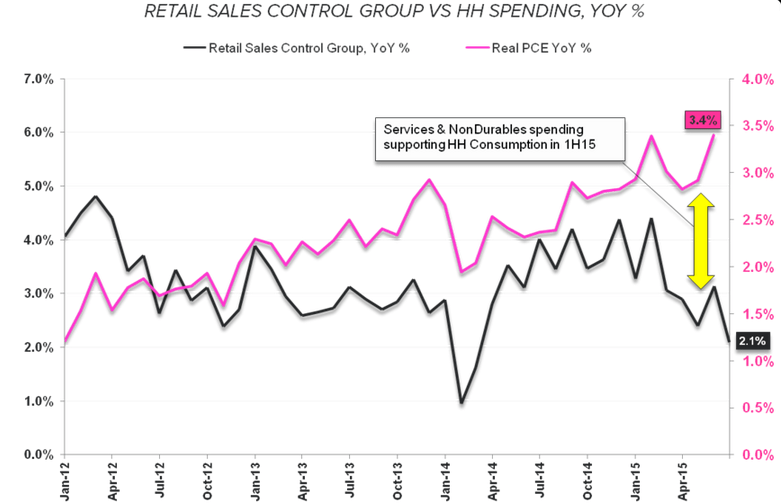

- Headline Retail Sales declined -0.3% sequentially from May to June

- On a longer-term duration which is more telling, headline retail sales decelerated on both a 1Y and 2Y basis in June (See chart below for the deteriorating trend)

- Small Business Confidence, meanwhile, declined -4.2 pts in June with the Expectations and Job Openings readings leading the decline

- NFIB optimism sits at its lowest levels since March of Last year

- UofM Consumer Confidence declined to 93.3 in a preliminary July estimate; this was down from 96.1 in June (nearly 3%)

As for rate hike expectations, Hedgeye Macro analyst, Christian Drake, said it best in a research note to institutional clients this week:

“In short, middling-to-down is not what Team Janet wants to see - particularly with sirenic hopes of a September lift-off still lingering and a sustained attempt at policy normalization stirring restlessly in the queue.”