We want to be clear about where we stand on the whole Macy’s REIT issue.

Up front let’s just say — it makes sense. When this became a potential issue six months ago, we removed the name from our active short list. Note that as it relates to this week, the concept of a REIT is not new. The only new component is Starboard going activist on making it happen two days after Macy’s sold off a store in Pittsburgh.

We want to be crystal clear that the way to be positioned in this space into our #growthslowing Macro call is to be short KSS. There is ZERO potential for Kohl’s to be monetized as a REIT.

There Is Zero Real Estate Play At KSS. The same strategy that gave KSS the upper hand in a pre-Internet era is the same one that takes away any optionality on a take out. It’s real estate is worth very little. The company owns 413 out of its 1164 stores. But they are almost entirely located in strip centers. JCP, for example, has 140 stores in ‘A’ malls (the top 300 malls in the country). KSS has less than 10. When you look at the economics, there are 1100 regional malls, and there have been maybe 5 built over the last decade. If you are a retailer who owns a piece of that real estate (the equivalent of beachfront property – there’s simply no more being made) then you’re in luck. But there are 7,000 strip centers. They’re literally a dime a dozen. Using the same metaphor, it’s like having a beach home, but being a half-mile walk to the ocean.

As it relates to Macy’s there are a few considerations.

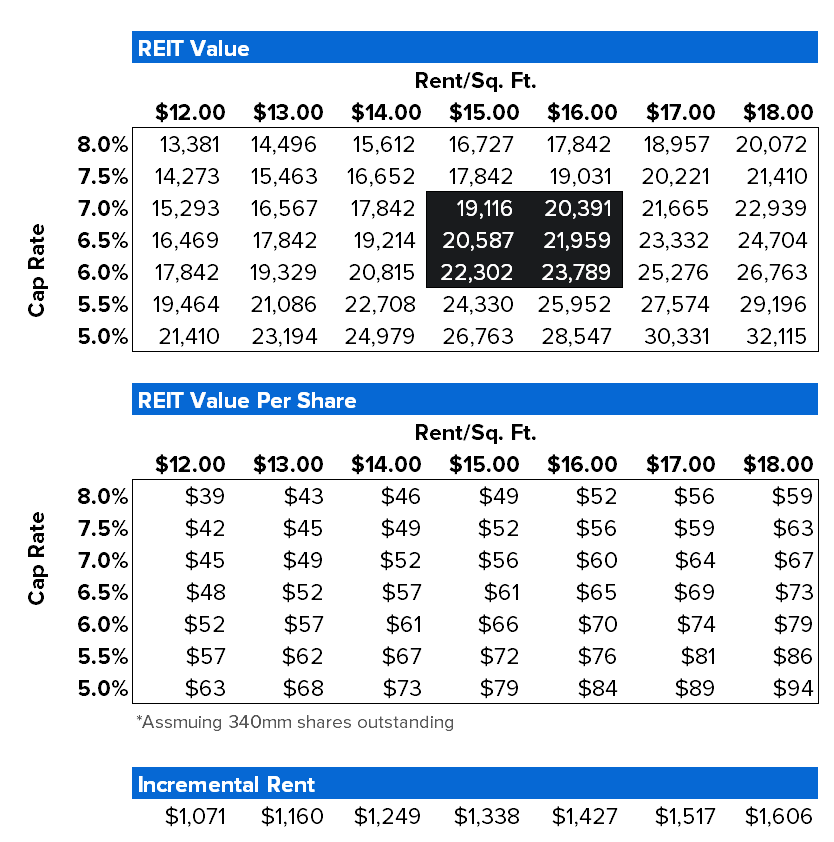

1) First is that we don’t think that the property values argued by Starboard are egregious. Keep in mind that Saks recently monetized its 5th Ave store for $3.7bn. When we look at Macy’s Herald Square, Chicago, and San Francisco properties, we don’t dispute that we could be looking at $6bn+ in value right there.

2) But, and this is a HUGE but…These exceedingly valuable properties are currently a massive freebie. Macy’s pays zero rent on them. Unless you want to assume that the operating company goes away — i.e. is worth zero — then Macy’s has to pay rent back to the future landlord. The more valueable the property is, the higher the rent, and the lower the margins. A $24bn value in the analysis below suggests that Macy’s would have to pay about $1.5bn in extra rent. Do you really want to cash in the crown jewel assets of an uber-cyclical and levered business, weigh it down with rent occupancy payments, potentially buy back stock (as some are arguing to us) at the top of a growth and margin cycle — only to leave Macy’s with no levers left to pull when the environment inevitably goes the other way? Yes, you’ll have sold assets at the top, but will have locked in rent at the top too.

3) The CEO and CFO at M are easily the most financial savvy executives in all of retail. If doing this kind of deal made sense, we think they’d probably have done it already. That said, CEO Lundgren has maybe a year or two before retirement, and Hoguet (CFO) has maybe a couple years more. This could potentially alter their appetite for a deal as it relates to creating a legacy. We’re just not so sure that’s the legacy they want to create.

4) If a deal comes to fruition, we wonder who will be on the other end? We know for a fact that there’s a market for one-off properties — like Macy’s Pittsburgh property that it monetized earlier this week. In that instance, Macy’s sold it and exited the market. It didn’t belong there. We’ve also seen instances where several stores were sold at a time. But 446 stores worth 89mm square feet and 5% of total apparel and accessory retail space in the US? We be really interested to see how liquid the market is for that kind of space.