“That’s right, Mr. Garrison. Christopher Columbus discovered America and was the Indians’ best friend. He helped the Indians win their war against Frederick Douglass and freed the Hebrews from Napoleon and discovered France.”

— Mr. Garrison’s hand puppet "Mr. Hat" from South Park

It seems like there's always a country to blame for their world’s economic or geopolitical woes. On the economic front, the current mantra is to Blame Greece. On some level, there is justification for this as Greece is rightfully causing investors to question the future of the economic union in Europe. The Euro has been mercy crushed as a result.

More so than the economic questions on the future of Europe are the emerging regional tensions that the current negotiation with Greece are bringing to the forefront. Clearly, the economic supremacy of Germany is taking the pole position in the negotiations with Greece. While every nation and finance minister had a vote, the recent decision imposed on Greece was ultimately negotiated unilaterally by Germany. In other words, the will of Germany is the will of the Eurozone.

The Greeks realize this and will Blame Germany. As our good friend George Friedman at Stratfor (a veritable private CIA) wrote this week:

“In World War II, the Germans occupied Greece. As in much of the rest of Europe, the memory of that occupation is now in the country's DNA. This will be seen as the return of German occupation, and opponents of the deal will certainly use that argument. The manner in which the deal was made and extended by the Germans to provide outside control will resurrect historical memories of German occupation. It has already started. The aggressive inflexibility of the Germans can be understood as an attitude motivated by German fears, but then Germany has always been a frightened country responding with bravado and self-confidence.”

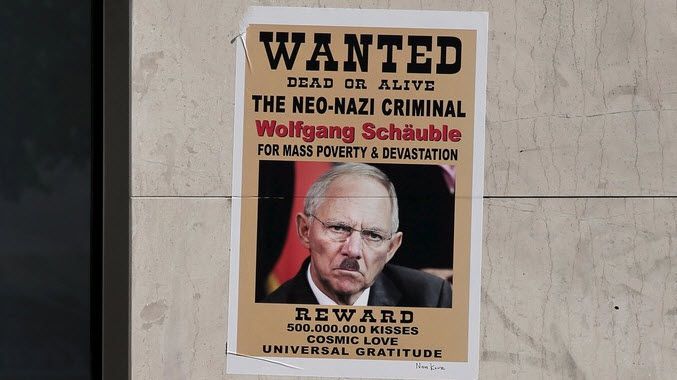

The larger reality then is that the centuries old conflict between nations and regions in Europe is re-emerging. Greek newspapers have been replete with references to World War II and the explicit accusation that Germany is trying to humiliate Greece. As highlighted in the picture below, some accusations have been even stronger. Case in point: a poster recently placed on the Eurobank branch in Athens accusing Germany's finance minister of being a neo-Nazi war criminal.

For their part, the Greeks are probably not doing much to ease the increased flaming of regional and national tensions with their “increased” flirting with the Russians. As an example, in June, Moscow announced a preliminary deal to build a pipeline through Greece. Over the past few days, there has also been speculation that Greece and Russia are close to an accord in which Russia supplies some of Greece’s energy needs (Greece currently imports 99% of its energy).

Is Russia the ultimate lifeline for Greece? Her trump card in negotiating with Europe? Probably not. But, frankly, even if none of this comes to fruition, it’s always easy for Europe to Blame Russia!

Back to the Global Macro Grind...

The Blame <insert country> reference ultimately comes from the TV show South Park, the (adult) cartoon that has been running for some 17 seasons. In a movie version of the weekly show, parents in South Park blame their kids' misbehavior on watching a Canadian made movie, hence Blame Canada.

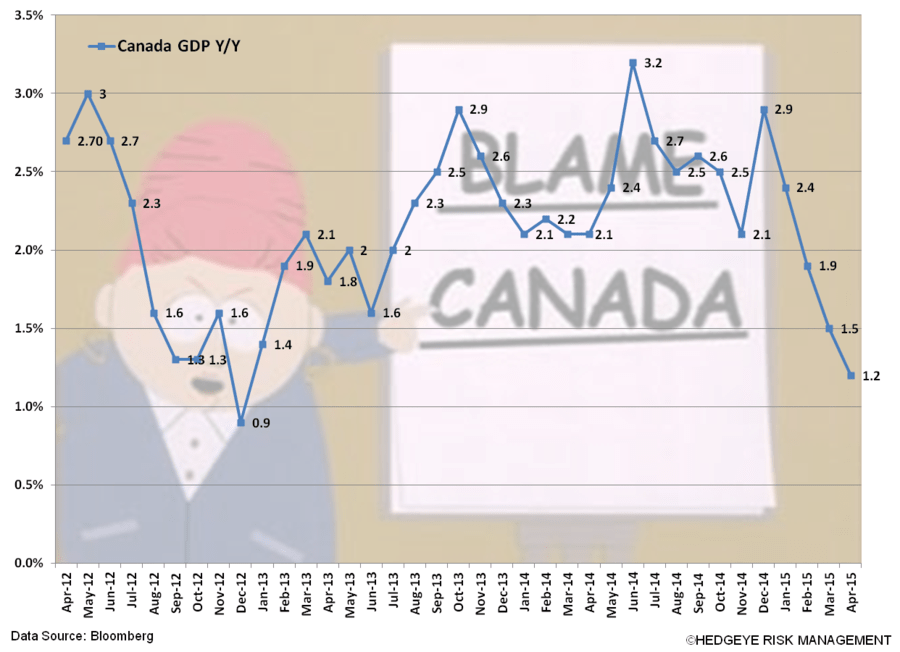

As we’ve been writing about recently, the next major global economic concern may well be Canada. As the Chart of the Day shows, Canada has been undergoing, at best, anemic growth this year. The Bank of Canada yesterday cut interest rates to 0.5%, its second rate cut of the year. In the accompanying statement, the Bank said:

“Canada’s economy is undergoing a significant and complex adjustment.”

We agree with that assessment in spades.

A few weeks ago, our Financials team presented more than 100+ pages on why they believe Canadian banks and banking system are great short ideas. Aside from the obvious exposure to energy, the other major economic risk in Canada is an overheating real estate market. The rate cuts by the Bank of Canada are only likely to continue to propel the home price gains, but the Canadian housing market will not be impervious to economic gravity in perpetuity.

One of the companies that we discussed in our report was Home Capital Group (ticker is HCG on the Toronto Stock Exchange). Fortuitously for our call, the company actually pre-announced negatively earlier this week and traded off some 14% as a result. Not a bad trade if you were short!

Conversely, there was actually some decent Canadian home price data reported this week. For June, Canadian home prices were 5.1% from a year ago, which was an acceleration from May. The two “hottest” markets Toronto and Vancouver (which account for more than 50% of the index) were up even more y-o-y at 8.5% and 7.8% respectively.

So, was Home Capital Group's pre-announcement just a blip, or a crack in the foundation of the housing market? We believe it's the latter and primarily this is based on affordability as the Canadian Home Price-to-Income ratio is 2.3 standard deviations above its long run average.

Want another proxy for valuation? The Canadian home price to rent ratio is currently at 19.4x. That's almost double its pre-bubble long run average of 11.7x.

The reason housing is such a risk for the Canadian economy is potential credit risk. The Canadian banking system is both concentrated and levered. The largest Canadian bank RBC has about 0.5x assets to Canadian GDP, which compares to JPM in the U.S. at a ratio of 0.15%. Further, Canadian bank assets in aggregate are at 2.1x GDP versus 0.5x for the U.S. You wanna banking leverage? The Canadian have it!

So if the next unraveling of the global economy comes from north of the border, you are probably safe to Blame Canada, but don’t Blame Hedgeye because we warned you.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.20-2.46%

SPX 2040-2120

RUT 1

Nikkei 20138-20768

VIX 12.51-20.01

Oil (WTI) 50.07-52.98

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research