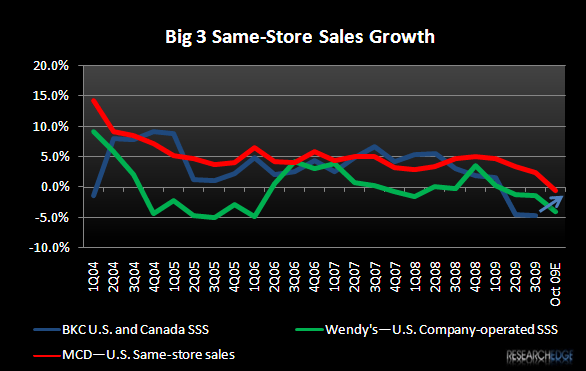

WEN stated on its earnings call that Wendy’s October same-store sales declined 4%. Although management stated that 2-year average trends are still up 1% as the company is lapping a difficult 5%-plus comparison from October 2008, this -4% number is a significant sequential step down from the +0.1% result in 3Q09 (-1.4% on a reported basis, which includes the negative impact of 300 fewer units YOY serving breakfast, as shown in the chart below). Management commented that this -4% excludes the impact of removing breakfast so this number is even lower on a reported basis.

When asked specifically whether BKC’s $1 double cheeseburger could be somewhat responsible for the sequential fall off in trends, management attributed the softer result to both a tougher comparison and marketing in early October that focused on more thematic, brand repositioning “You Know When It's Real" advertising rather than value/price point advertising.

Based on MCD’s guidance for October U.S. same-store sales of flat to negative, both MCD and Wendy’s experienced a sequential slowdown. Again, BKC did not provide any specific color around October trends, but it did say the $1 double cheeseburger had provided a lift to traffic trends in the markets where it had already been launched in fiscal Q1, and it was launched nationally on October 19. If this product’s success continues, October will not experience the full benefit as a result of the mid-month launch, but I would expect to see some sequential improvement and then see trends move higher for the balance of the year. My expectation mirrors TAST’s recent comments about its Burger King comparable sales trends. Earlier this week, TAST said that it expects its Burger King same-store sales to turn positive following a -5% result in October. Even this -5% number already showed marginal improvement from TAST’s reported -6.1% comparable sales growth result in 3Q09.