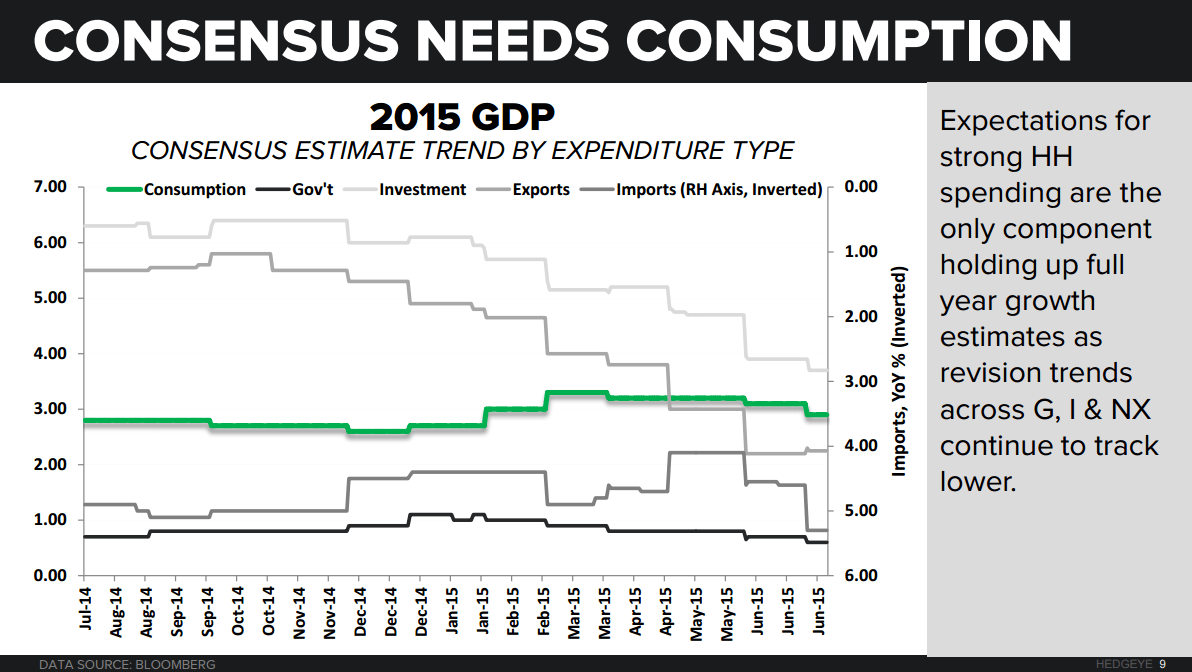

Editor's Note: The following chart was featured in today's morning strategy note written by Hedgeye U.S. Macro Analyst Christian Drake. For more info on how you can subscribe click here.

Editor's Note: The following chart was featured in today's morning strategy note written by Hedgeye U.S. Macro Analyst Christian Drake. For more info on how you can subscribe click here.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.