BWLD is moving to the Hedgeye Restaurant Ideas List as a SHORT.

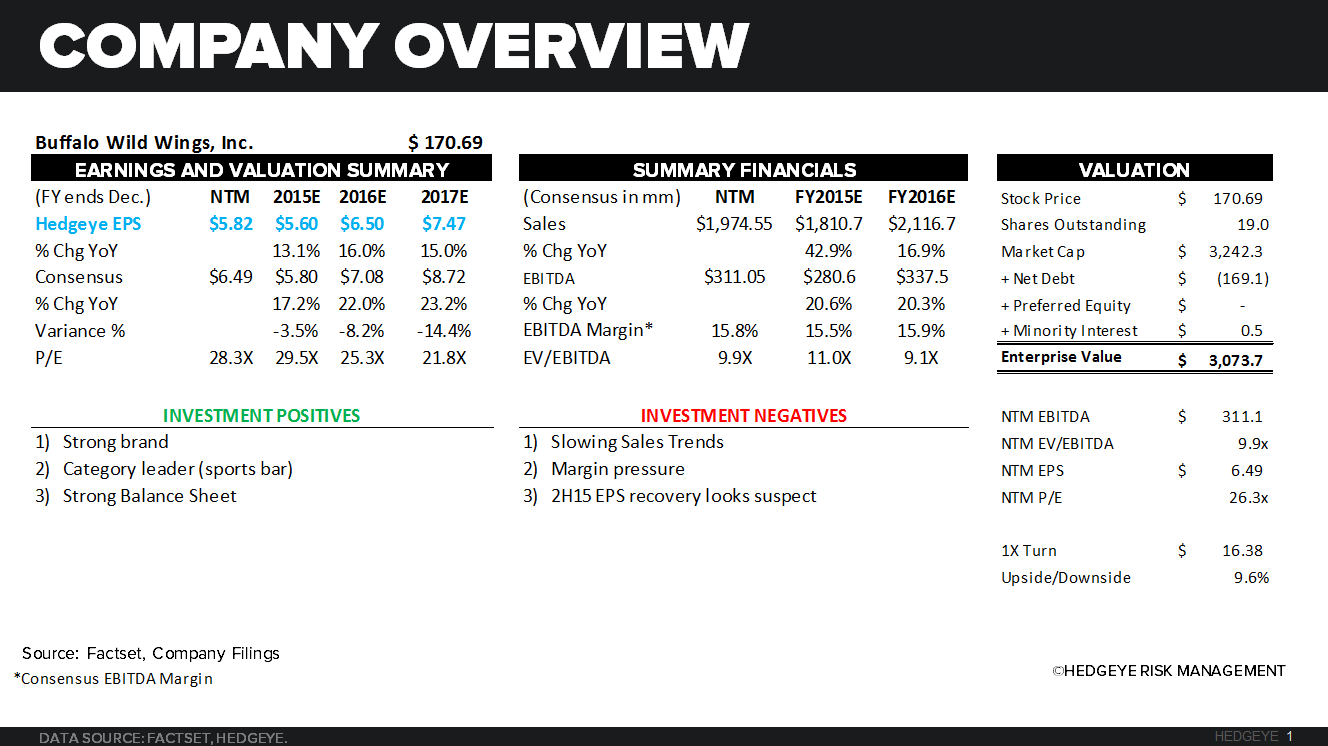

COMPANY OVERVIEW

Following the 1Q15 EPS miss, it’s now a back end loaded year. The company missed by $0.11 in 1Q15 and the street has now reduced estimated by $0.15-$0.20 for 2015. Is there another round of estimate cuts to come? At this point it looks like the street estimates are $0.20 too high for 2015.

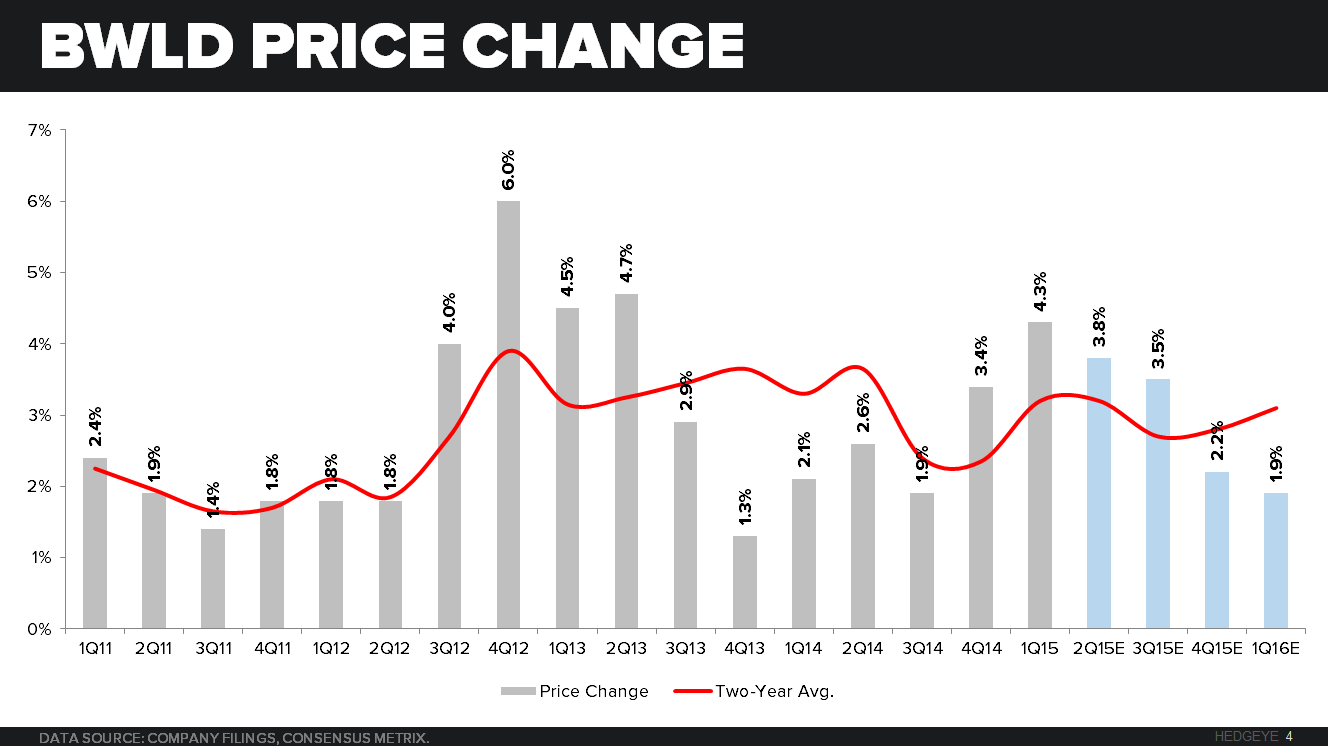

PRICE PERFORMANCE

BWLD is down 6.8% year-to-date, versus the average casual dining stock up 7.5%. Year-to-date BWLD is the worst performing restaurant stock we follow that is not considered broken. As of last night’s close, the stock has recovered $8 of the $24 it lost following the 1Q15 earnings miss.

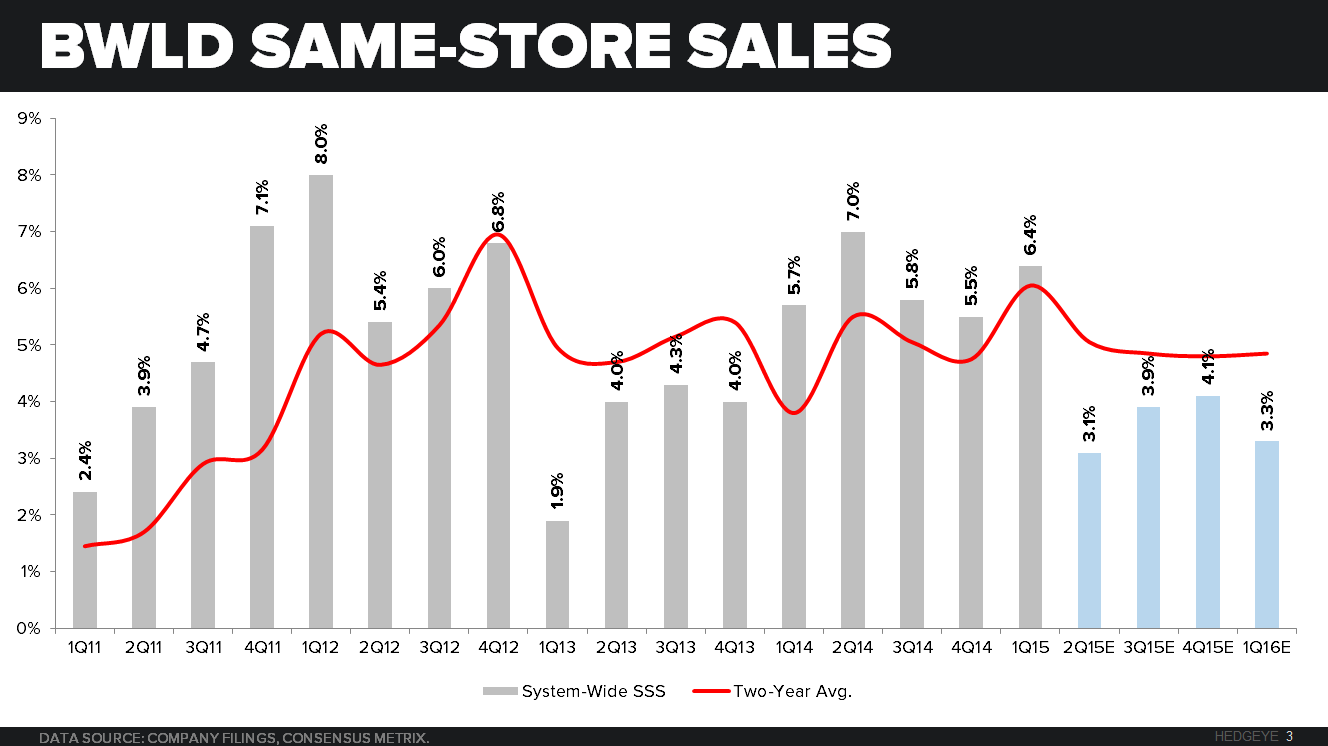

SAME-STORE SALES

After stringing together 17 straight quarters of positive sales and traffic BWLD is experiencing a significant sales slowdown. In 2Q15 we estimate that BWLD’s “Gap to Knapp” will shrink 220 bps to 2.0%, the lowest level since 2Q11.

What is causing the slowdown in BWLD sales trends?

Has BWLD been too aggressive raising prices over the last 4 years? Since 2Q11 BWLD has been running annual increases of 3% every quarter.

No concept has the ability to take significant price increases over a long period of time and not face a slowdown in traffic.

In 2Q15 the price/mix for BWLD will be 0%! This will be the first time since 2Q13 that this metric is flat or negative.

WHERE IS THE LABOR LEVERAGE?

In 2014, BWLD added about 100bps in labor costs to roll out its Guest Captain experience in the stores. The biggest increases to labor costs were seen in 2Q14 & 3Q14. Ironically, beginning in 4Q14 the company has not been able to make the consensus EPS estimates, despite seeing acceleration in same-store sales trends. While wing prices have increased over the same time, that issue should not have been a surprise.

Looking at the trends for 2Q15, if the Guest Captain initiative is a driver of incremental traffic, why are same-store (traffic/mix) slowing? Going forward, if BWLD has limited pricing flexibility and same-store sales are slowing it will be very difficult to leverage labor costs.

RESTAURANT LEVEL MARGINS

If same-store sales are slowing can the company leverage the incremental labor costs running in the P&L? Therefore, the recovery in restaurant level margins in the 2H15 and 2016 look unlikely.

OPERATING MARGIN

To offset some of the pressure on restaurant level margins BWLD management needs to get aggressive in cutting G&A to limit the damage to the EPS line.

EARNINGS ESTIMATES

Estimates for BWLD FY15 have been coming down, but they still seem aggressive. The EPS recovery story in 2H15 will likely not materialize.

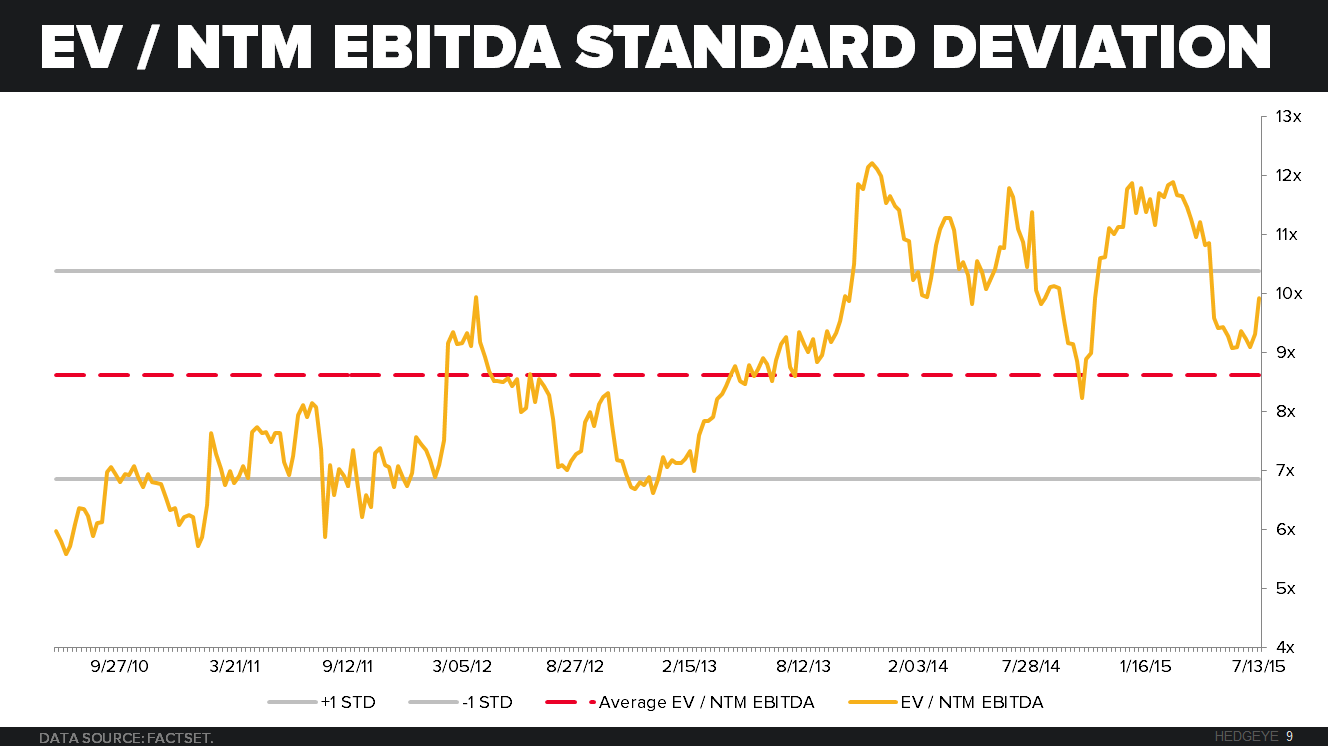

VALUATION

BWLD looks to offer good value relative to others in the space, but with estimates too high, the cheap valuation can be deceiving.

SHORT INTEREST

At 11.59% of the float, BWLD’s short interest is higher than most casual dining companies.

SELL-SIDE SENTIMENT

Sentiment is very positive on the company with 61% of the analysts having BUY ratings. This bias is reflected in the consensus estimates for a recovery in profitability which is unlikely to happen.

HEDGEYE RESTAURANTS IDEAS LIST