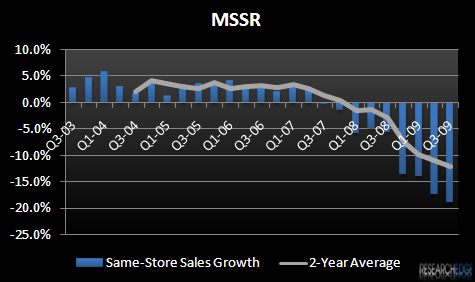

MSSR reported 3Q09 earnings after the close yesterday and same-store sales trends continue to be ugly. Management seems to take some comfort in the fact that traffic trends improved sequentially from Q2, but with traffic still down 14.2% in the quarter relative to -16.7% in Q2, there is little to get excited about. And, same-store sales growth actually got worse, -18.8% (from -17.3% in Q2) as increased value initiatives put pressure on average check, which was down 4.6% in the quarter relative to -0.6% in Q2.

MSSR did join the list of restaurant companies that experienced less bad trends in October. In response to a question, management stated, “Yes, actually we saw some deterioration month-over-month in the third quarter, July, August, September, which resulted in the 18.8% on the comp sales side. But what we've actually seen in October is an improvement. We're going to be at 13.9% on a comp basis – sales comp basis for P10. More importantly, as we've said, we've seen some improvement in the overall traffic. We're at a 10.4% year-over-year comp on traffic for October.”

In this challenging environment, most restaurant operators are talking about value and increased promotional strategies to drive traffic. At the same time, management teams do their best to assure investors (and themselves) that they are approaching value in a way that will not be detrimental to their concepts’ long-term brand image. This does not seem to be the case at McCormick and Schmick’s.

Though not a newly announced change in strategy yesterday; management is not being promotional as much as deliberately acting to change the brand. Management even used the term “rebranding” in reference to its latest efforts to increase frequency at its bars and is attempting to broaden its target audience. Management stated yesterday on its earnings call, “Over the past couple of quarters, I have outlined a broad strategy to evolve our concept with the primary goals of broadening our connection to a younger audience, increasing our brand relevance and improving our overall satisfaction ratings with our guests. This strategy involves rebranding our bar experience, expanding our culinary offerings and synergizing our marketing efforts. I am pleased to say we made good progress in all of these areas in the third quarter.”

Management is in the process of upgrading its audio-visual package to drive additional traffic during key sporting events and is offering significantly lower prices points on its menu such as 10 items under $10 at lunch. These initiatives may help traffic in the near-term, but they seem to highlight a fundamental change in brand image. With the 10 items under $10 lunch program already accounting for 34% of McCormick and Schmick’s lunch entrees, the value band offerings representing 8.4% of entree sales and the new $19.95 positioning on the culinary side running at about 11% of entree sales, it may be difficult to remove these offerings when economic conditions improve as they now make up a sizeable portion of sales.

These new offerings are in line with management’s communicated strategy “to broaden its guest space.” I just wonder if, over time, these initiatives will lead the concept into the casual dining “sea of sameness,” which as we have seen is not a much better segment to be in right now.