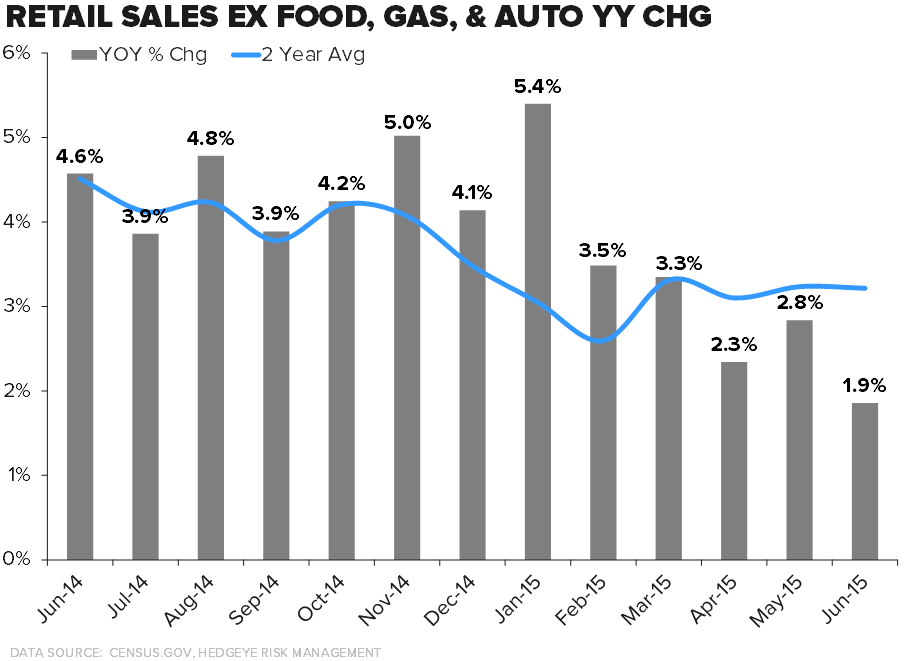

Retail Sales Slowing

Expectations were definitely out of whack headed into this Retail Sales print given the big headline miss. Two things… 1) The level of sales growth relative to last year is absolutely positively decelerating. In January we saw 5.4% growth, and we've steadily decelerated to 1.9% in the following five months. 2) We're scratching our heads as to why this is a big 'surprise'. Commentary from large and small retailers alike have supported a decelerating growth rate. In addition, while the 2-year run rate in the real discretionary categories is below what we witnessed in 2H14 (4%) it is consistent with what we've seen over the past 3-months. The bottom line...Yes growth is slowing. Yes we expected it. Compares throughout the rest of the summer, and fall, AND holiday, don't get any better.

M - Macy’s Sells Downtown Pittsburgh Building for Redevelopment; Store to Close

(http://investors.macysinc.com/phoenix.zhtml?c=84477&p=irol-newsArticle&ID=2067241)

Takeaway: The Pittsburgh store sale doesn't appear to be a deviation from the company's prior store strategy or indicate any change in management's willingness to monetize other assets through a sale leaseback transaction. Fact is Macy's didn't belong in the downtown Pittsburgh market -- the co-tenant list alone surrounding the store confirms that. This is an opportunistic move by the company to monetize a 1mm+ sq. ft. property that was much too big for the market it catered to.

VNCE - CEO Jill Granoff To Depart After Transition Period

CEO out just three weeks after the CFO 'resigned immediately'. Should this be a real surprise to anyone given that the stock is down 73% in seven months, but is 56% owned by Private Equity? With today's announcement flushing out the last of the bulls, we think the stock is starting to look pretty intriguing. The reality is that the brand remains relevant. Management did not do any damage, it just failed to execute on a brand/distribution growth plan. With a total Enterprise Value below $500mm, and an achievable EBITDA level of $125mm, we're looking at a sub-4.0x EBITDA multiple. This name might be damaged goods for the investment community for a while, but we'd be surprised if it isn't part of a bigger company in 1-2 years (or sooner if the stock drifts into the single digits).

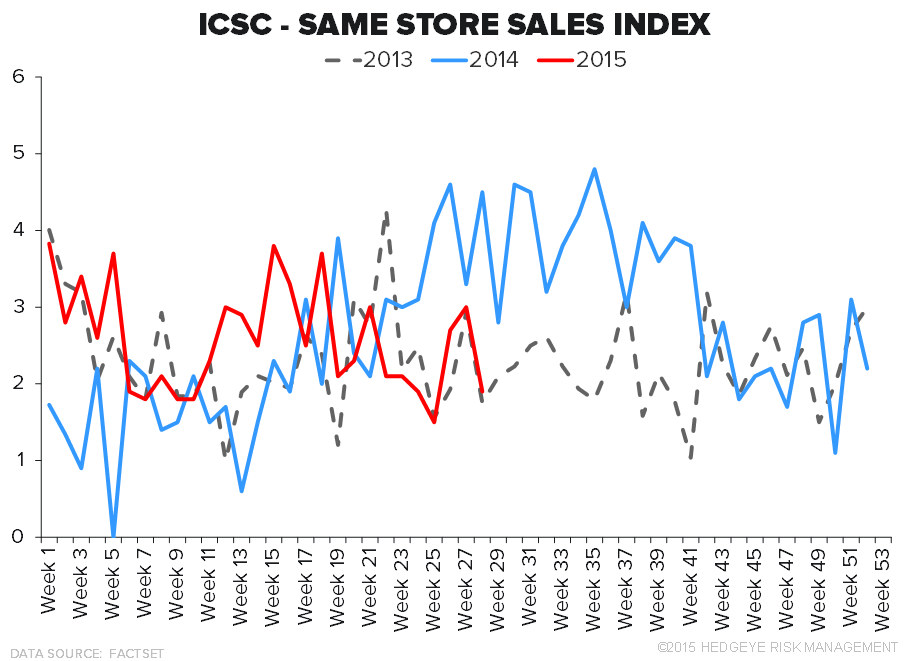

Chain Store Sales - Retail Sales slowed through June, and July doesn't appear to have picked up based on this morning's ICSC reading.

OTHER NEWS

CASY - Casey’s General Stores CEO to Retire

(http://www.wsj.com/articles/caseys-general-stores-ceo-to-retire-1436819564)

Kate Hudson athleisure line going brick-and-mortar

(http://www.retailingtoday.com/article/kate-hudson-athleisure-line-going-brick-and-mortar)

World’s largest mall slated for 2016 opening

(http://www.chainstoreage.com/article/world%E2%80%99s-largest-mall-slated-2016-opening)

DLTR - Dollar Tree plans South Carolina distribution center

(http://www.chainstoreage.com/article/dollar-tree-plans-south-carolina-distribution-center)

RCII - Rent-A-Center sells 14 Canadian stores to easyhome Ltd.