Coincident to our MCD Black Book, please note that we have added SONC to our main short list and WEN / JACK to our short bench as potential market share losers due to MCD’s resurgence.

RECENT NOTES

7/12/15 JUST CHARTS | YUM

7/10/15 DFRG | COVERING THE SHORT

7/9/15 JUST CHARTS | CMG

7/9/15 REPLAY | LONG MCD BLACK BOOK PRESENTATION

6/29/15 BOJA – ADDING TO THE BEST IDEAS AS A SHORT

RECENT NEWS FLOW

Friday, June 10

DFRG COO resigns (click here for article)

Black Box same-store sales show an increase of 2.1% for the month of June (click here for article)

Thursday, June 9

FDA delays menu-labeling requirements until December 2016, previous deadline was December 2015 (click here for article)

DRI names Jeffrey Davis Chief Financial Officer (click here for article)

PNRA upgraded to neutral from sell at Goldman Sachs

Wednesday, June 8

MCD initiated neutral at Cleveland Research

WEN announced final results of tender offer (click here for article)

Tuesday, June 7

BOJA has signed a new multi-unit development agreement for units in West Virginia and Kentucky (click here for article)

Monday June 6

FRGI subsidiary Pollo Tropical to open two new locations in Tennessee (click here for article)

SECTOR PERFORMANCE

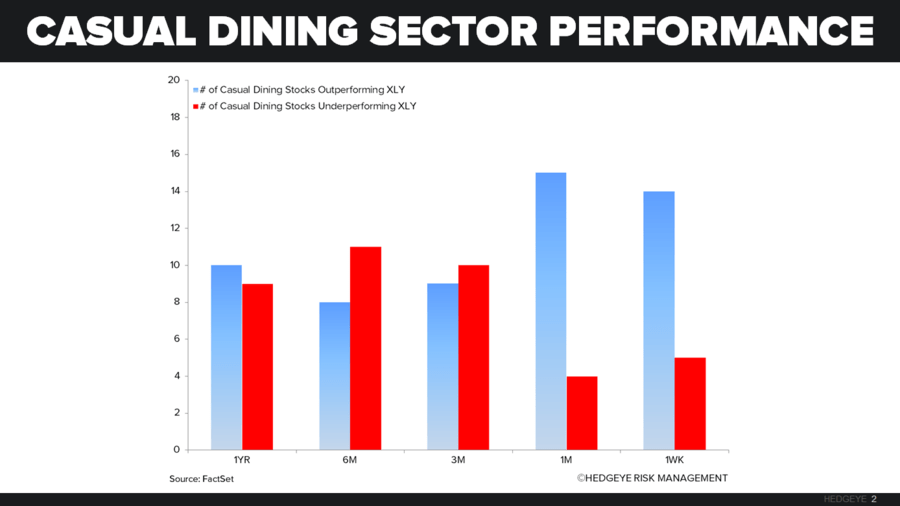

Casual dining and quick service stocks, in aggregate, outperformed the XLY last week.

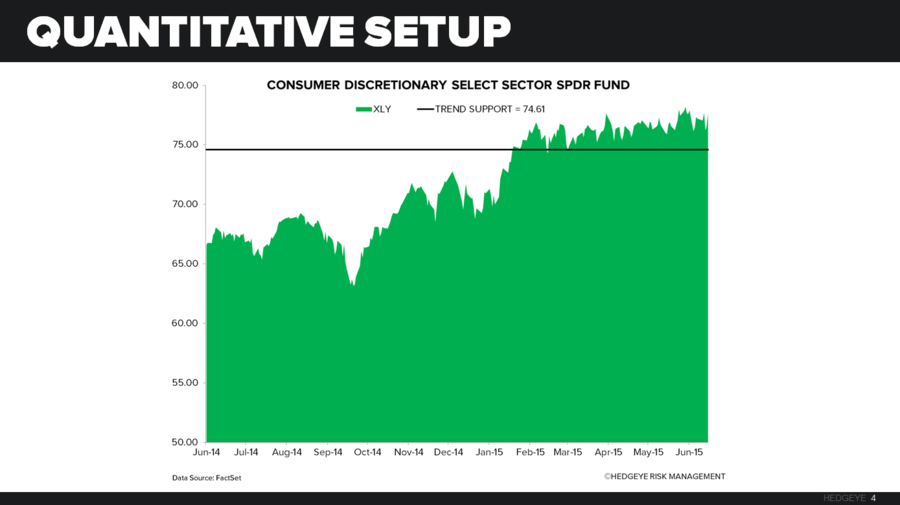

QUANTITATIVE SETUP

From a quantitative perspective, the XLY remains bullish on an intermediate-term TREND duration.

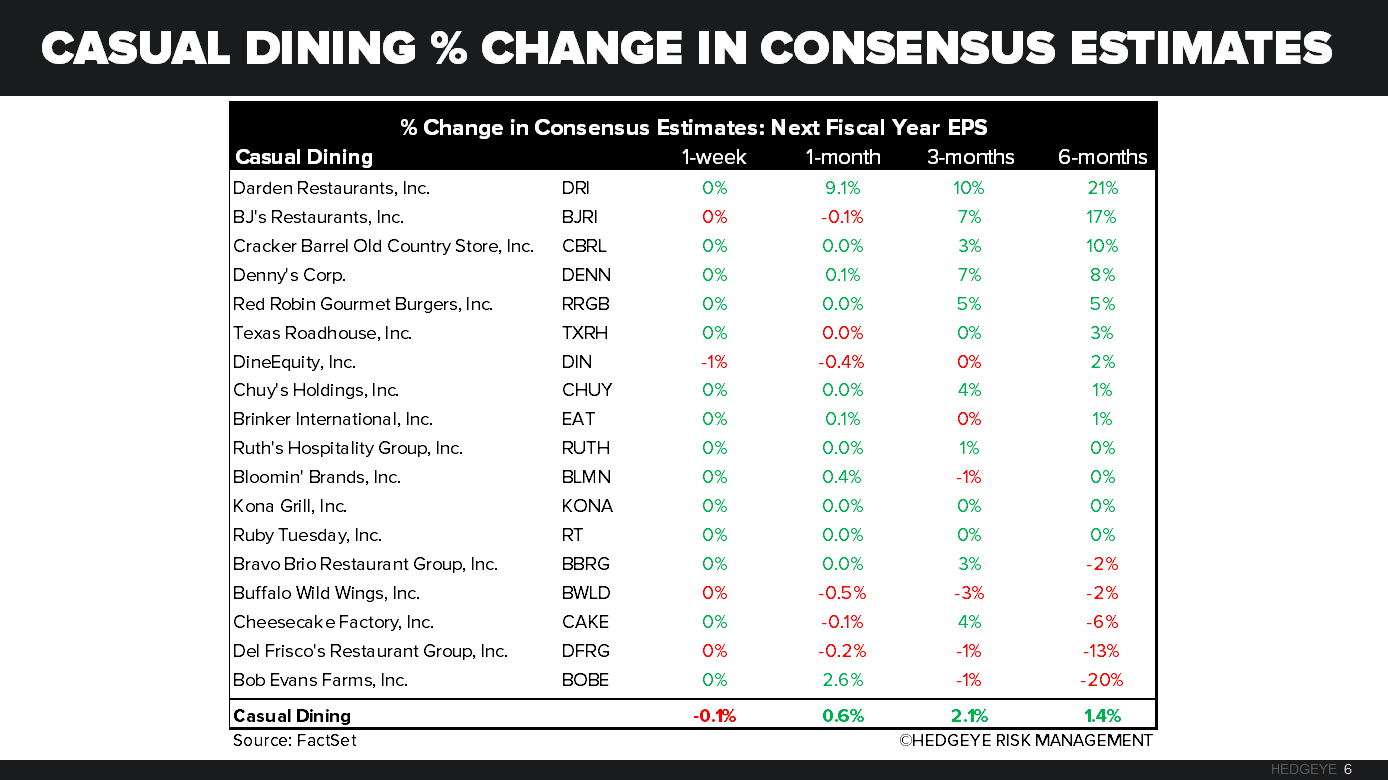

CASUAL DINING RESTAURANTS

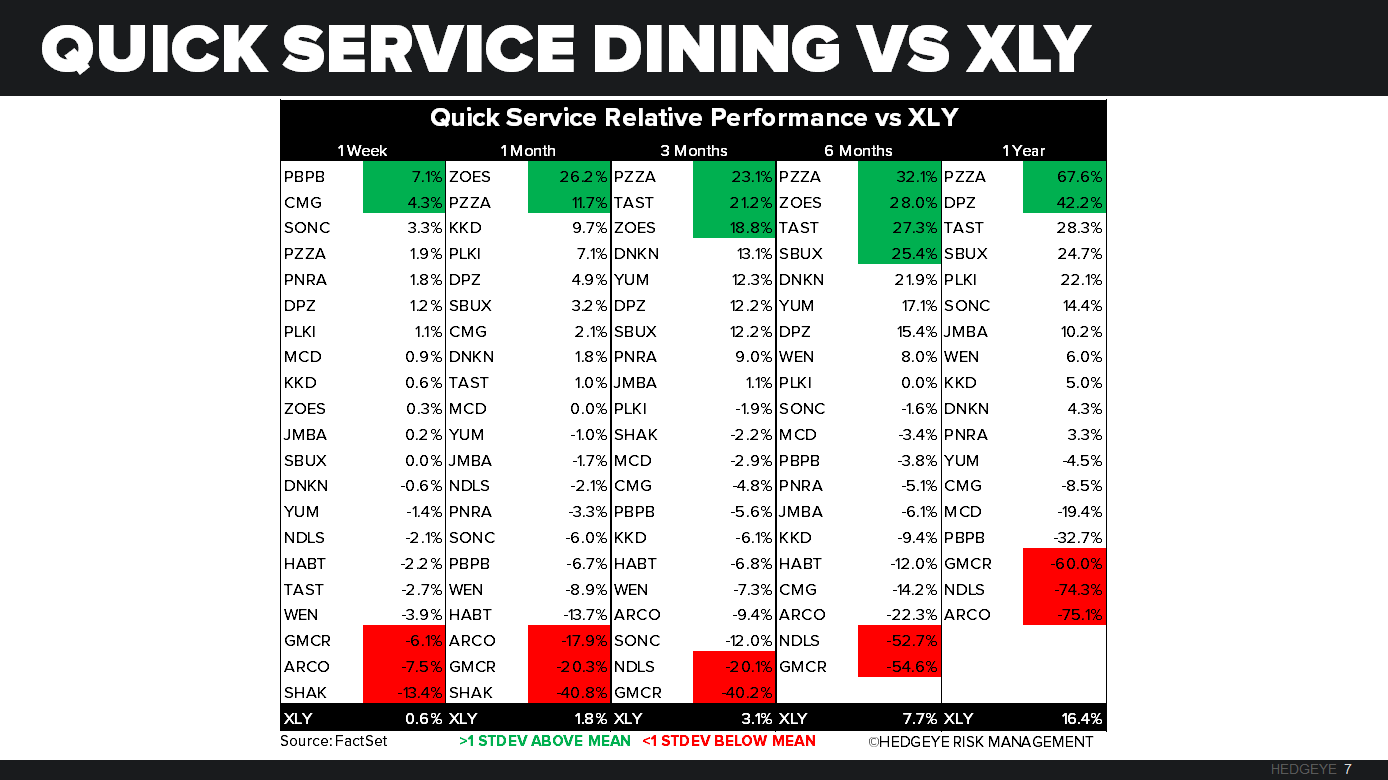

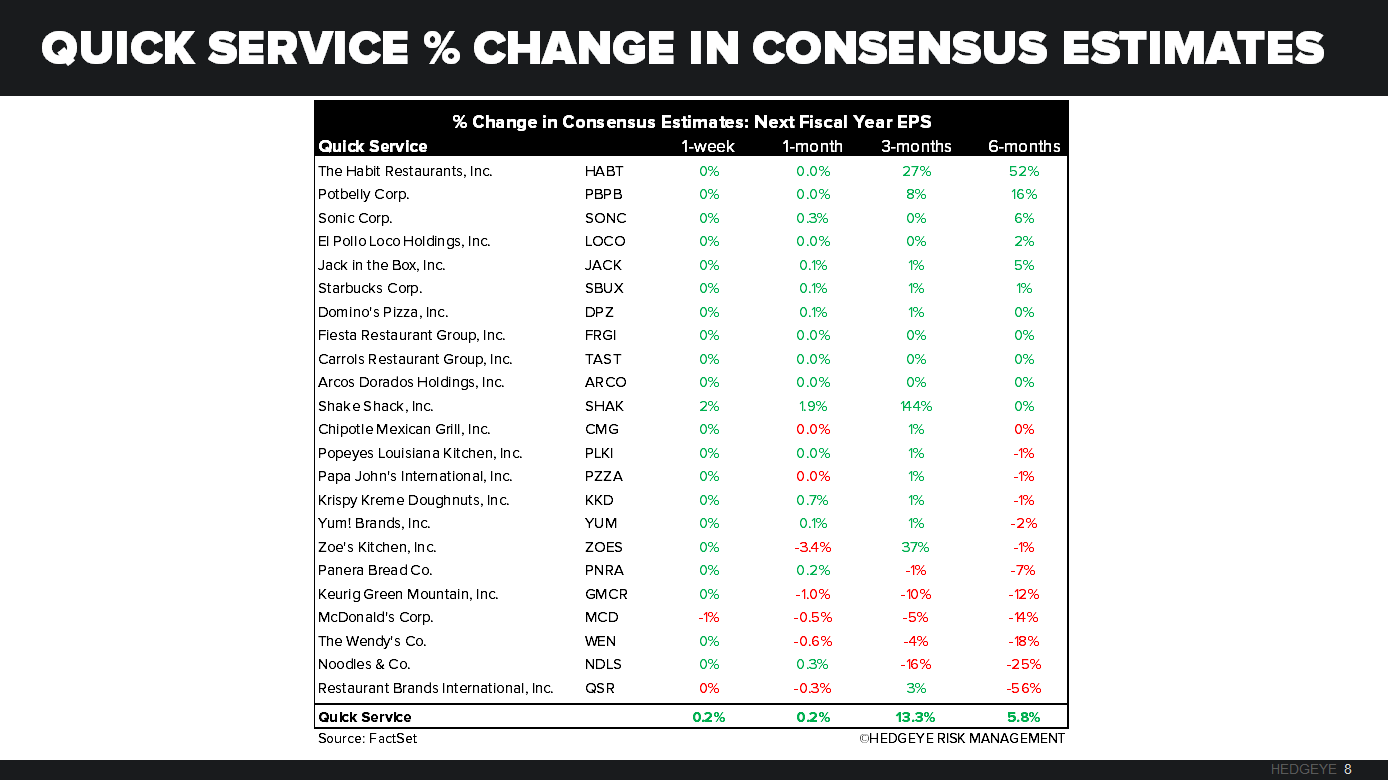

QUICK SERVICE RESTAURANTS