Below are Hedgeye analysts’ latest updates on our EIGHT current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each.

Please note we removed Gold from the long side this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

PENN

Gaming, Lodging and Leisure Sector Head Todd Jordan reiterates his team's bullish high-conviction thesis on Penn National Gaming. The company remains one of our favorite names on the long side and boasts the best new unit growth story in domestic gaming.

Jordan further notes that with more states releasing their June gaming revenues this past week, we feel more confident in our higher than consensus Revenue, EBITDA, and EPS estimates.

KATE

We held a "Flash Call" on Kate Spade recently to address the concerns we’ve been fielding about the brand and company from institutional investors in light of the selloff since the company reported earnings in early May.

Here were our conclusions from the call:

- Some concerns are valid, some are not. We’ve had more questions and concerns from investors on KATE over the past two weeks than we’ve had all year. Given the weakness in the stock, we wanted to address these issues.

- The business is absolutely on track. Comp trends, ecommerce, and margins look fine from where we sit. The company actually managed to get estimates for the quarter and the year to very achievable levels.

- Why no one cares is the bigger question. But new investors largely don’t care, as they perceive “The Space” to be broken, and KATE to be expensive, volatile, and unmodelable. In the end it’s too small for them to ‘have to care’.

- In the end, execution wins. We think that “The Space is Broken” argument is laughable. The softer concerns like disclosure and management stock ownership are more valid. But when all is said and done, watch what they do, not what they say. This stock is flat-out cheap and growing at 50%.

GIS

General Mills remains on the Hedgeye Consumer Staples Best Ideas list as a LONG. Closing out the year, many people are looking at the sales miss and as a result are bearish on the stock. But those people appear to be sheep, listening to and following whatever the media tells them. If you look at the full story GIS has a lot of things going for it and they are going to show it in the top and bottom line this year.

Over the last couple of months, the company has announced the removal of artificial colors and flavors from their cereals. More recently, they have committed to using only cage-free eggs. Many of these small actions that management is taking are going to have a snowball effect as they go throughout FY16.

FY16 Hedgeye Guidance ―

Looking into FY16 we are excited about the possibilities. Management is working hard on their “Consumer First” initiative and making great changes to current product while also introducing new products. Below is not a comprehensive list but some of the biggest things that we are looking forward to this year:

- Yoplait in China

- Gluten-Free Cheerios

- No artificial colors or flavors in the cereal

- Granola innovation / Muesli

- Greek Plenti / Whips

- Original yogurt sugar reduction

- Renovation on Grain Snacks

- Strong push on Natural & Organic products

- Delivering Value to consumer on brands like Totino’s and Hamburger Helper

- Bringing U.S. innovation International

Bottom line is they are still struggling; we don’t want to shy away from that. But the core of the portfolio is growing and management seems to be working tirelessly on implementing changes to grow the rest of the portfolio, especially cereal. We also still believe that to have continued growth into the future a sizeable acquisition or divestiture would be beneficial to the business.

DE

Flooding in key farming areas has helped to reduce expected crop yields, pushing grain prices higher in recent weeks. Higher grain prices are a key short-term risk for our bearish view of Deere.

While we have used this wet weather and DE’s 2Q beat as an entry point, sustained higher prices would likely delay the downward normalization of farm equipment sales.

While we cannot accurately forecast the weather, we can look at normalized fleet dynamics. On that basis, we continue to view DE’s results as cyclically inflated and at risk of a sharper than expected decline.

VIRT

Financials Sector Co-Head Jonathan Casteleyn reiterates his view that shares of Virtu Financial are very richly valued. Despite principal risk in their daily trading operations, the stock is being priced in-line with the exchanges.

He adds that VIRT has no tangible equity capital to absorb a potential trading loss. It would have to draw down credit lines should their historical track record in trading break down. He estimates shares are worth $18 per share or the mid point of our scenario analysis.

TLT | VNQ | EDV

It looks like more deflation on our screens.

We’re removing GLD from Investing Ideas as a result. As we’ve attempted to communicate through all of the central planning hoopla, we like gold most when both the USD and rates are declining.

- The USD broke out to the upside this week and is now BULLISH on an intermediate-term trend duration (3 Months or more)

- With the correlation risk to commodities flashing red, we now have a BEARISH bias towards commodities as an asset class over the intermediate-term

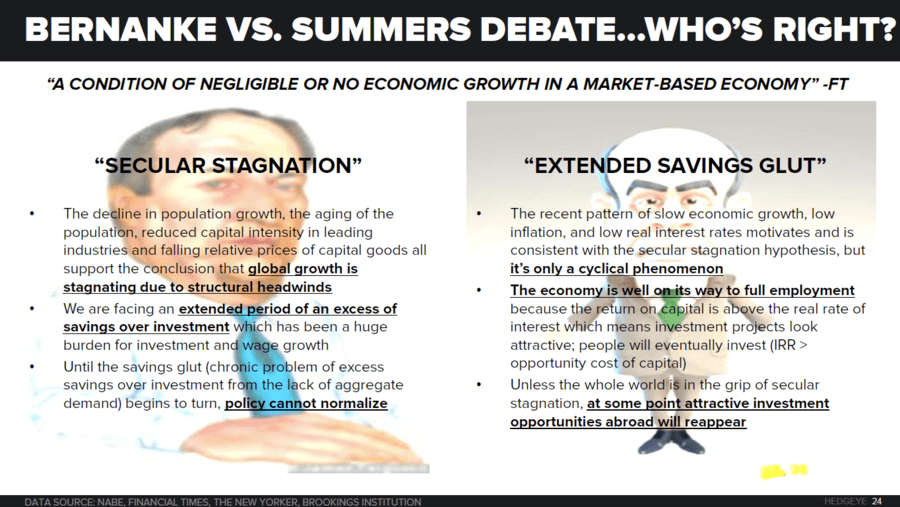

Earlier this week, we presented our Q3 2015 macro themes deck to our institutional customers. In it, we outlined the case for #LowerForLonger on interest rates highlighting our work on #SECULARSTAGNATION and our view on the #CONSUMERCYCLE (hint: It’s autumn).

The third component of the deck was devoted to #EUROPESLOWING. On Europe slowing, we expect the relative central planning monetary policy from Draghi in reaction to Europe’s woes to weaken the Euro (EURO down, USD up, COMMODITIES come under pressure).

We have no doubt the economy will cycle as it always has; additionally, the empirical evidence for #SECULARSTAGNATION is hard to refute. If the up cycle has officially run-out of steam, and the facts supporting the secular stagnation thesis come to fruition, we’re more confident than ever in #LowerforLonger.

Long-term Treasury rates remain the best proxy for forward-looking growth expectations.

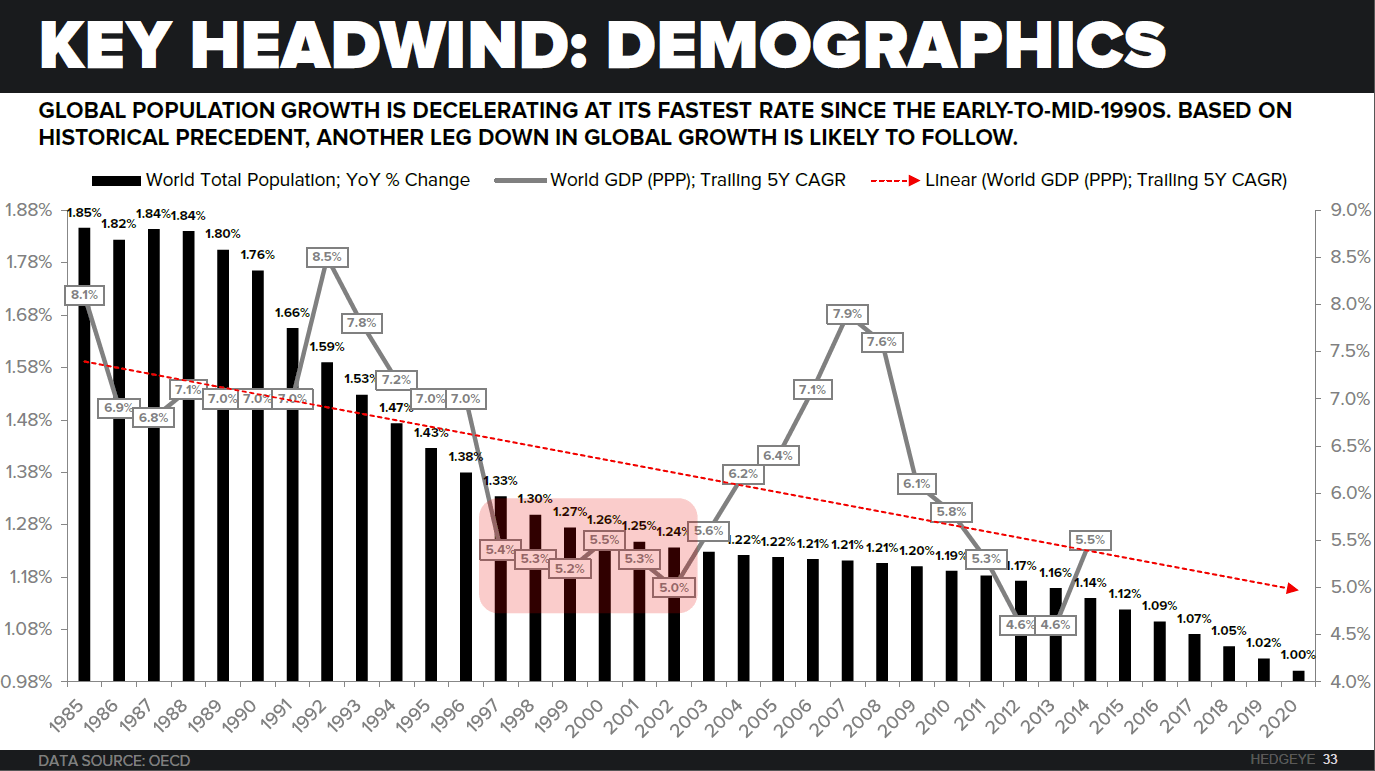

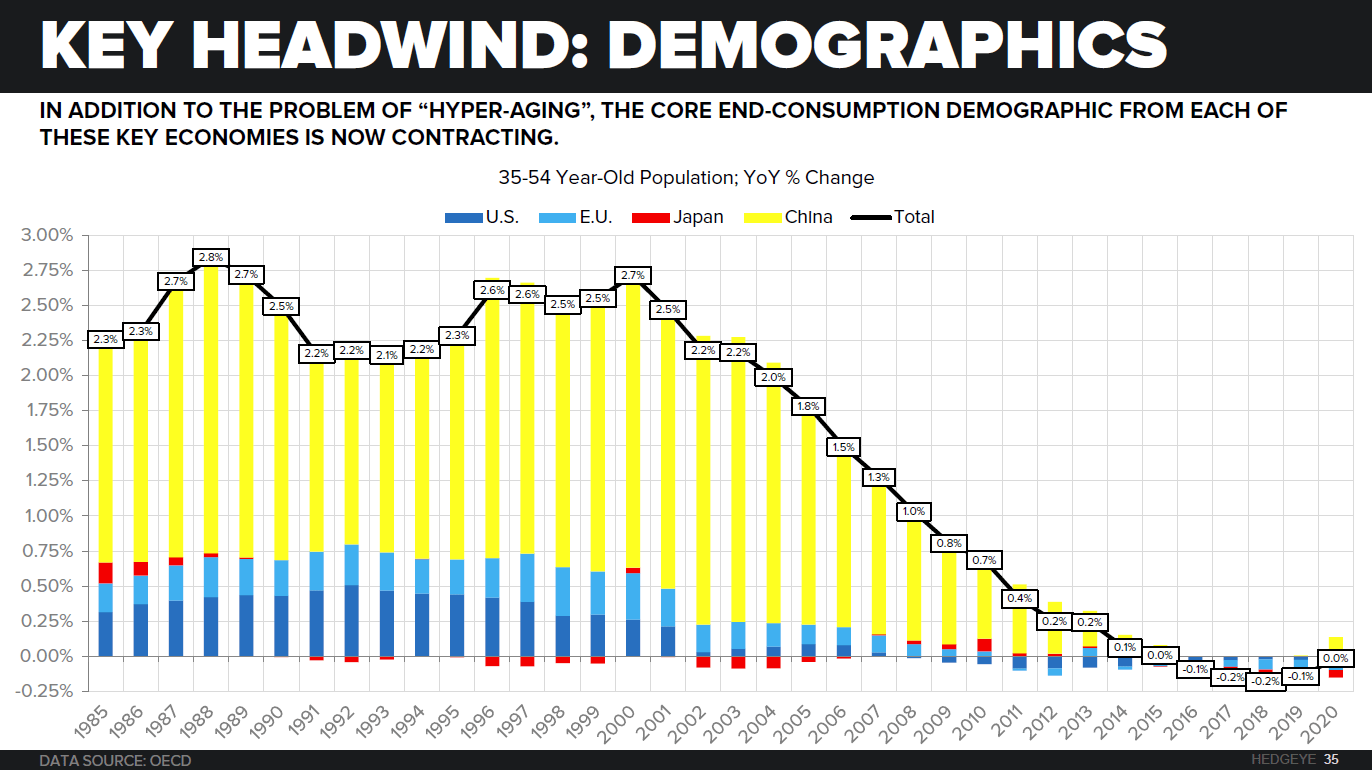

We outline three components of secular stagnation below to explain the SAVINGS/INVESTMENT GLUT that is at the heart of the academic argument for current policy measures:

- Negative demographic trends globally (decline in population growth and aging population)

- Reduced capital intensity in leading industries (think of the capital and labor required to start Facebook over U.S. Steel)

- Falling relative prices of capital goods

Please see the three charts below supporting our thesis:

Finally, as you may have read, Ben Bernanke and Larry Summers have been going back and forth with one another on the secular stagnation debate. While one agrees and the other disagrees that the savings to investing glut has perpetuated secular stagnation, and is a real structural hindrance to growth, they’re both in agreement on the most highly debated topic in macro right now:

We’re nowhere near ready policy normalization (rate hikes)