We would like to introduce a note that we will be releasing periodically called, Just Charts. The purpose of this will be to revisit our restaurant dashboard and analyze our Long and Short names as well as other notable names in the industry.

There won’t always be a definitive call made, but we will give you our perspective on current trends and expectations.

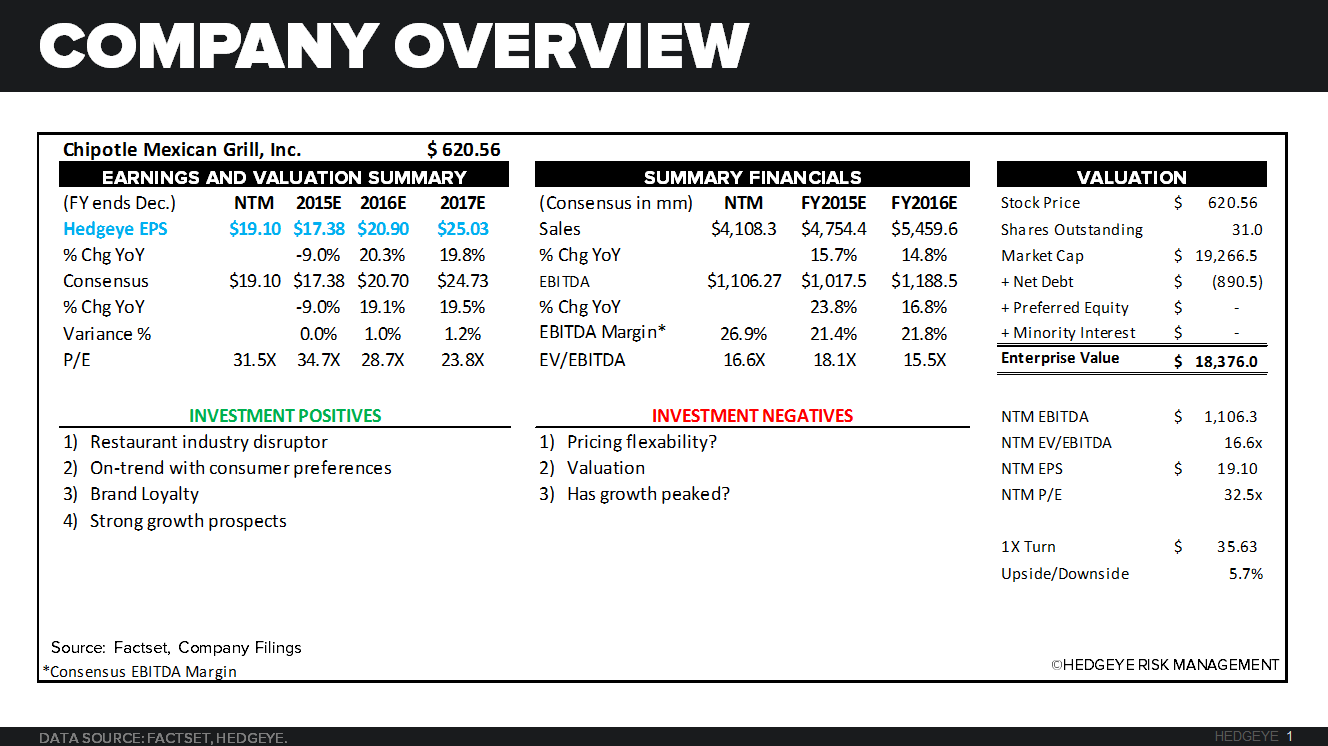

That being said, the first name we would like to revisit is Chipotle (CMG). CMG remains on the Hedgeye Restaurants ideas list as a LONG.

CMG has been under significant selling recently as we approach the 2H15, when the company will be up against very challenging comparisons. Despite these near-term challenges we like CMG for the tail duration. How to trade this stock going into the 2Q print is difficult to call. I suspect that a “better than bad” same-store sales print could cause some short covering.

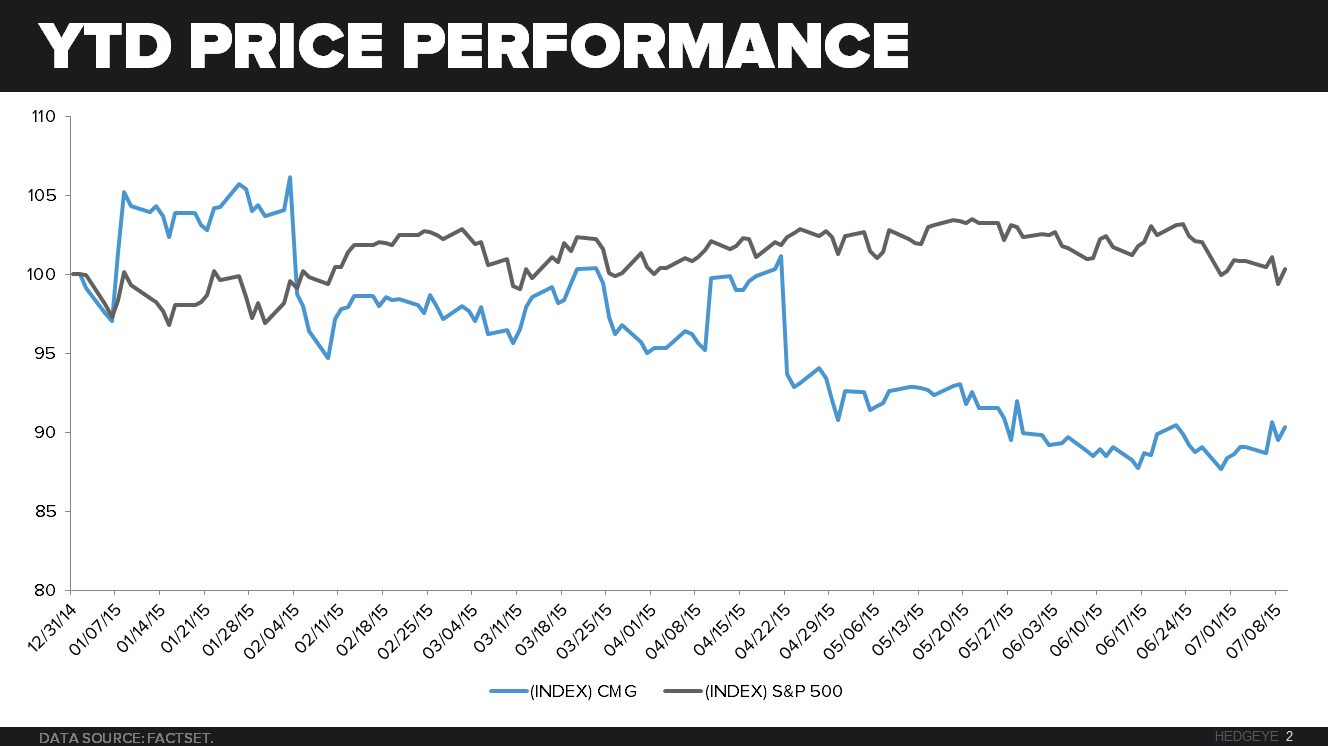

PRICE PERFORMANCE

CMG shares are down 9.6% year-to-date versus up 0.3% for the S&P 500. The short-term sales comparisons are a cyclical and not secular problem for the company. One turn on the EV/NTM EBITDA multiple suggest 5.7% upside/downside in the name.

FINANCIALS

SAME-STORE SALES

CMG is facing some very difficult comparisons over the next three quarters and that has the street nervous. Will CMG post declining same-store sales over the next three quarters? The 2Q15 print will set the tone for the balance of the year. The consensus estimate of 6% for 2Q15 suggests only a slight slowdown in two-year trends from 11.9% in 1Q15 to 11.7% in 2Q15E. I suspect that 6% might be an aggressive estimate for 2Q15.

MARGIN TRENDS

RESTAURANT LEVEL MARGINS

Restaurant level margins are expected to be 28.04% in 2Q15, up 74 bps year-over year. The company should benefit from lower food, labor and other costs in the quarter. The trend in margins supports our LONG thesis.

EBIT MARGIN

Operating margins will also improve nicely in 2Q15. G&A should come down by 88bps to help push operating margins up 18.8%, up 164bps year-over year. There continues to be significant leverage in the business model.

SENTIMENT AND VALUATION

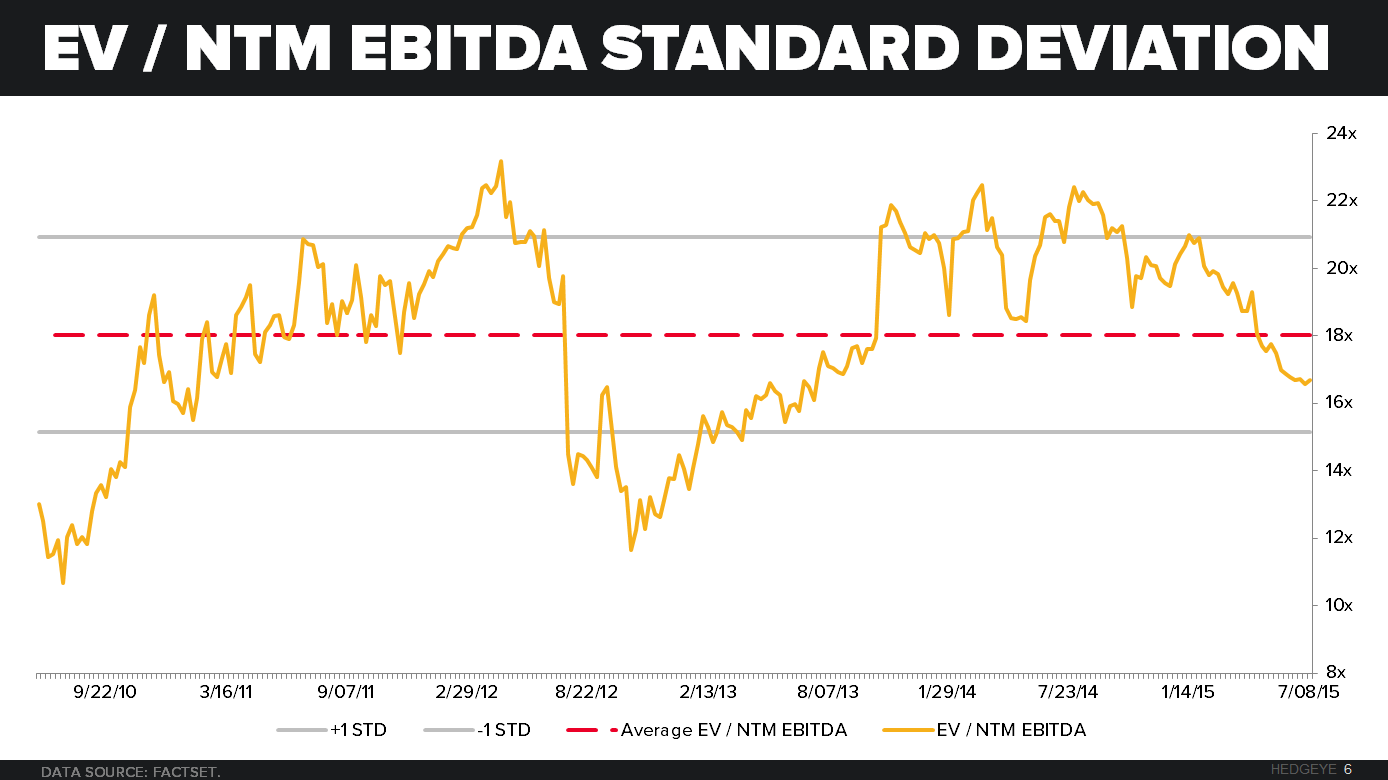

EV / NTM EBITDA

Trading at 16.6x EV/NTM EBITDA the stock is not cheap, but it’s not aggressively overvalued given the opportunities for the company. Yes, CMG is trading at a premium to its peer set, but deservingly so, as we said previously, it will grow into the valuation.

SHORT INTEREST

CMG’s short interest is low hovering right around 4-4.5% of the float. While it has moved up in 2015, there is not a big negative bet against this company.

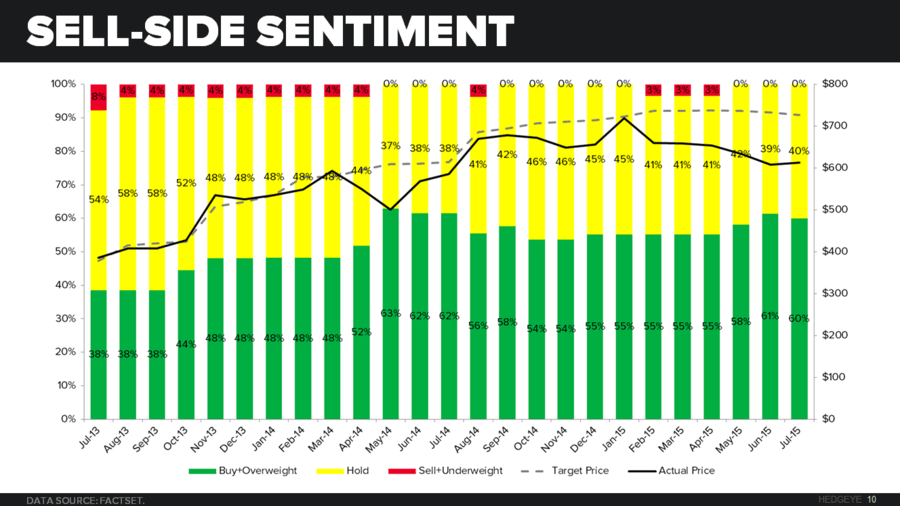

SELL-SIDE SENTIMENT

With 60% of the analysts having a buy on the stock and no sell ratings, there is also a positive bias to the name. Given the financial performance of the company for the past two years, the bullish bias appears to be justified.

HEDGEYE RESTAURANTS IDEA LIST