In-line Q for a company that ‘everyone knows will beat’ is never good – especially when the driver was outsized SG&A reduction. We’re negatively predisposed here, but there’s no catalyst on the downside near-term. We’ll be patient.

Judging by the massive run up in Warnaco’s shares into the close on Tuesday afternoon, one might have thought this was about to be a blowout to the upside. After all, it wouldn’t e the first time for WRC –which artfully manages expectations. Yes, Warnaco managed to print an inline quarter, but it did so with a massive 17% y/y decline in SG&A. As a result, in an environment where expectations are high, inventories are tight, and even the junkiest of companies are beating – this is hardly an impressive result from WRC.

So what’s next? After going through our model and recognizing management’s guidance of $2.70-$2.80 for the year, we are shaking out at $2.77. If there’s upside it’s likely to be driven by a massive swing in F/X, which goes from being a 4% drag in revenues in 3Q to a 6.1% benefit in 4Q. Overall, we remain negatively biased on this one as it is our belief that that the company has been starving itself of investment spend (in the brands) while predominantly focusing on its higher margin, non-US retail expansion (CK stores are still carrying 20% four wall margins). We can’t argue that this strategy should and will continue to work in the near-term as the company maintains a 20+% square footage growth rate for CK retail expansion (even though backing into new store productivity gets us to abysmal incremental profit metrics). Over the longer the run, we worry about what will happen when the rate of growth slows and mix-driven margin expansion reverses. Admittedly, being short WRC as F/X turns into a substantial tailwind, inventories are cleaner than they have been in a year, and same-store sales are showing signs of acceleration, doesn’t make a ton of sense to us. We’re still skeptical, but realize the factors line up for what is a classic case of “getting by”.

3Q Results

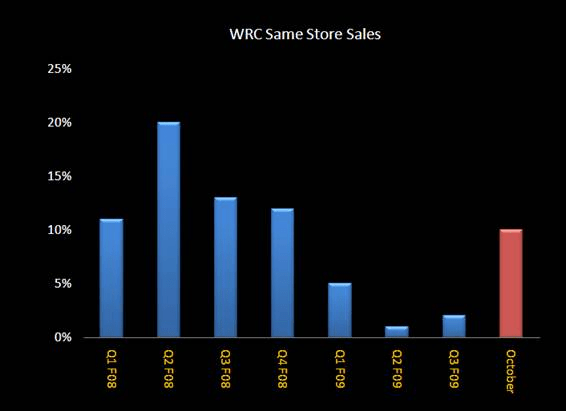

Overall topline came in slightly below our forecast, driven by weaker than expected intimate apparel revenues. Offsetting this was weakness was a slightly improved retail segment comp, which increased by 2% in the quarter. Same store sales now appear to have bottomed, after a substantial deceleration over the past year. In fact, management pointed out that comps for October were up 10%, reflecting a major rebound across both Europe and Asia. For those of us primarily focused on domestic trends, the interesting takeaway here is that both “weather” and easy comparisons were key drivers of recent strength no matter what region across the globe.

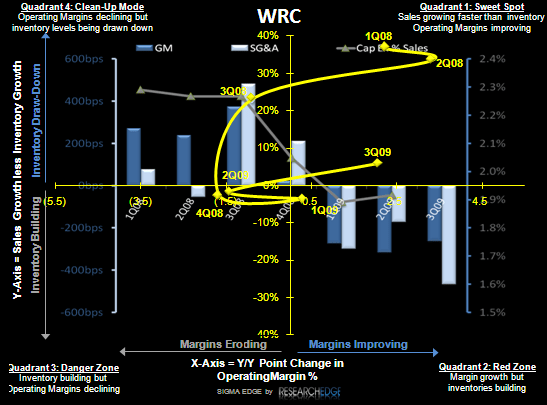

For the first time since 2Q08, Warnaco’s sales/inventory spread turned positive, with revenues down 5% and inventories tightly managed, down 11%. Despite this favorable dynamic, gross margins were still down 260 bps year over year (clearance wasn’t a major theme on the call but it may have played some part here). The negative impact of foreign exchange, promotional activity and a slight mix shift to lower margin products were to blame. Offsetting the margin decline was a massive 550bps reduction in SG&A as a percentage of sales. The decline in expenses of 17% y/y was the largest quarterly decrease we’ve seen since the company announced its plans to eliminate $70 million in annual costs in 2009. Aside from cost savings initiatives, F/X was a substantial y/y benefit, as last year’s 3Q included $15mm of F/X related expense that reversed this year. All told, the quarter was inline at $0.75 per share.

Eric Levine

Director, Retail Vertical