Initial jobless claims rose by 15k to 297k in the latest week, though it appears to be due at least partly to the dual volatility of the July 4th holiday and summer auto furloughs, as unadjusted claims in Michigan more than doubled while those from Ohio were up 50%. We'll reserve judgement until we see the next few weeks of data.

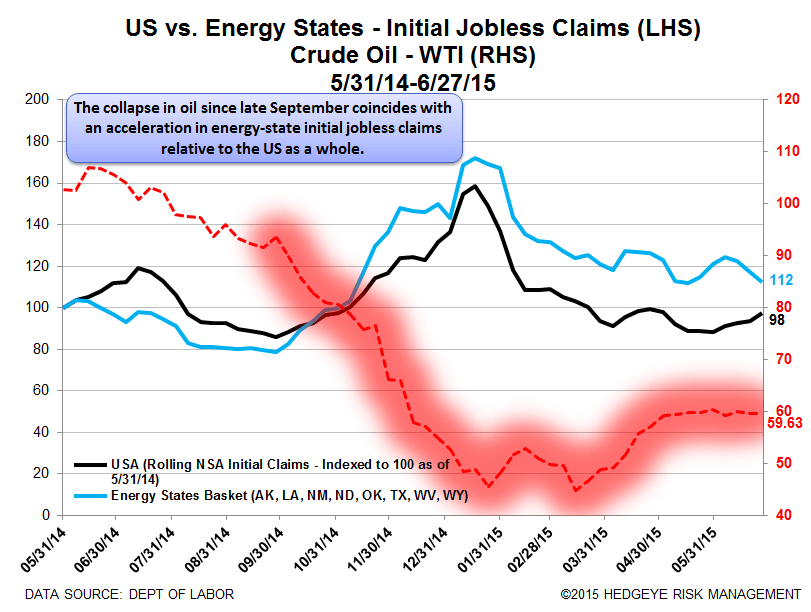

The chart below shows that indexed claims in energy heavy states fell in the week ending June 27th while rising for the country as a whole. The spread between the two series tightened from 24 to 15.

Meanwhile, courtesy of our Macro team, the chart below shows the Challenger job cuts announced for June running at close to zero for the energy sector for the first time in 7 months. Meanwhile, the total ex-energy climbed slightly in June.

The Data

Prior to revision, initial jobless claims rose 16k to 297k from 281k WoW, as the prior week's number was revised up by 1k to 282k.

The headline (unrevised) number shows claims were higher by 15k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 4.5k WoW to 279.5k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -10.9% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -12.6%

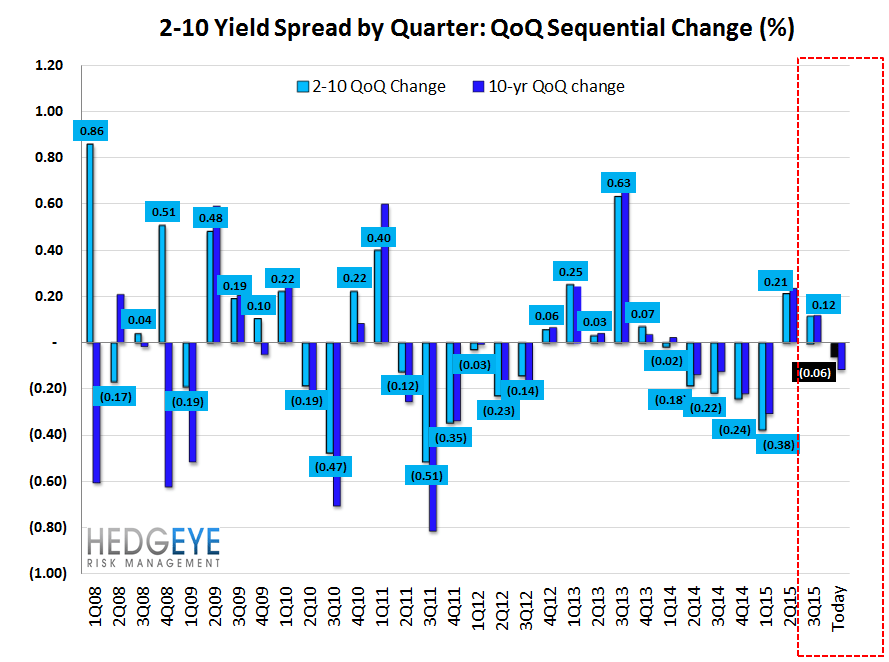

Yield Spreads

The 2-10 spread fell -9 basis points WoW to 165 bps. 3Q15TD, the 2-10 spread is averaging 170 bps, which is higher by 12 bps relative to 2Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT