SIGMA Update - Bad 2H inventory setup just in time for higher wage and shipping costs

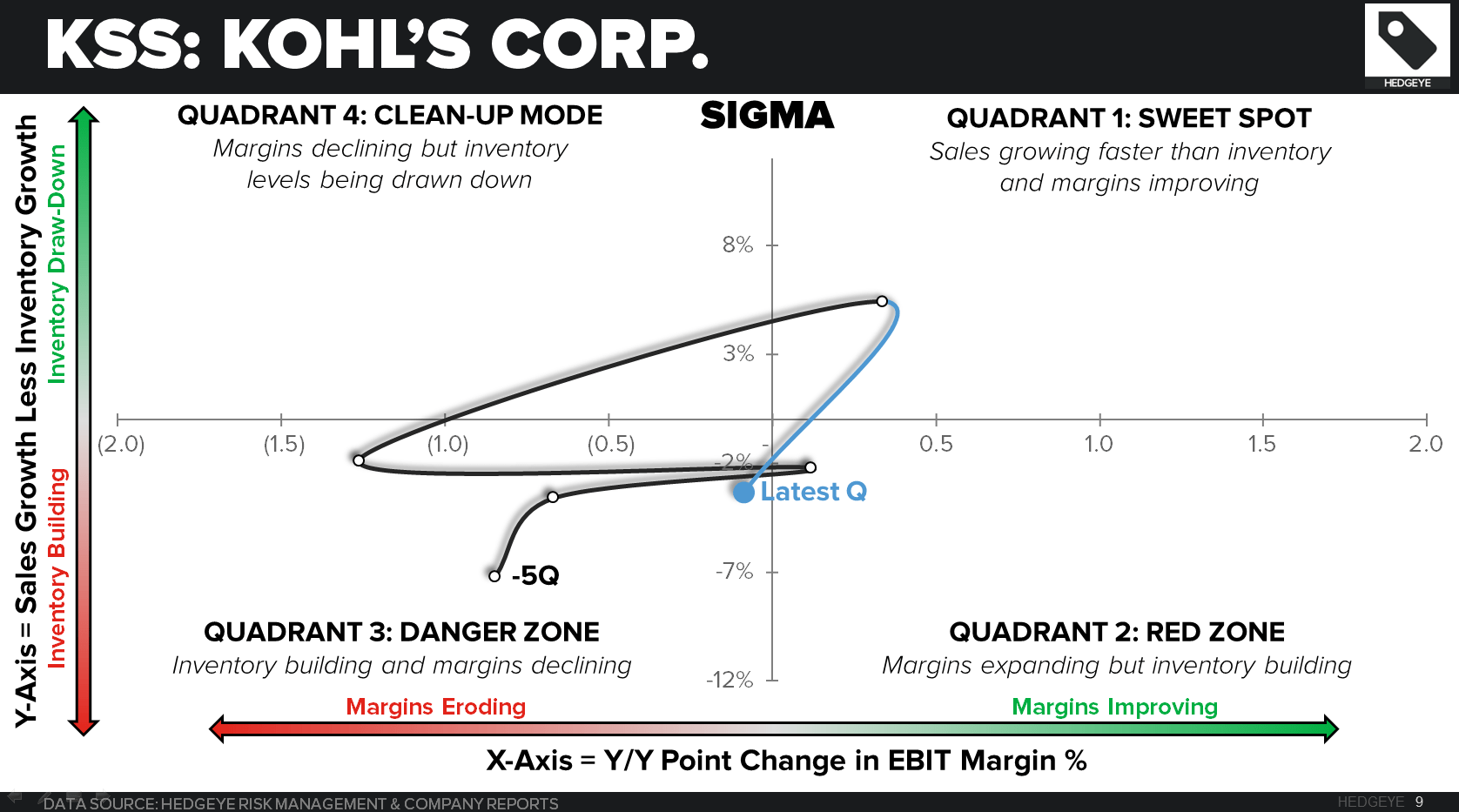

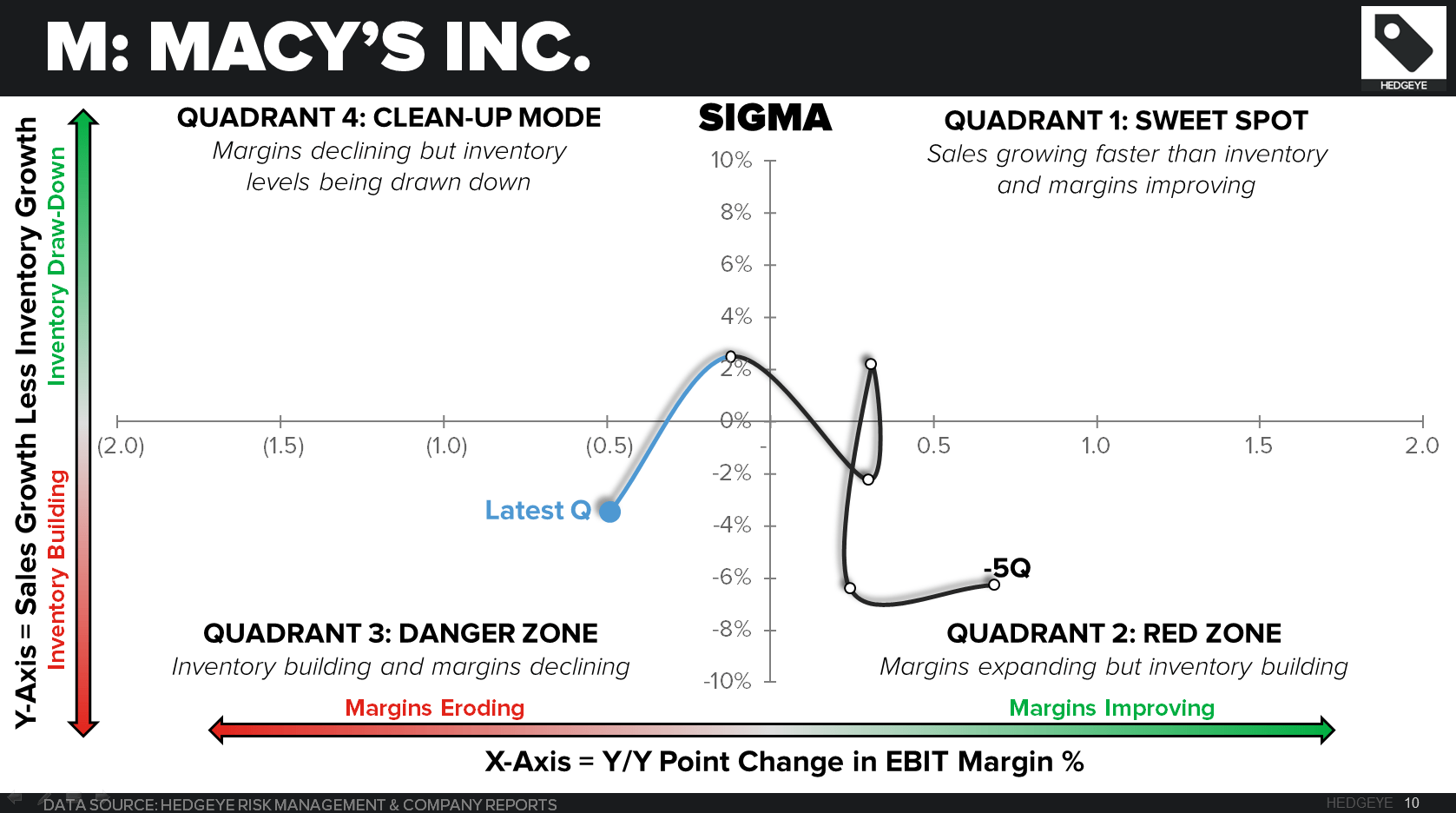

We sent out our updated SIGMA book for about 100 companies on Thursday. We picked out a few of the gnarlier looking charts. Most them are department stores -- or companies with no square footage growth. We're not playing favorites. They simply looked the worst. Regardless, there's one thing that is undeniable...these retailers are heavier on inventory heading into 2H than they'd probably like. With wage pressure building beginning in August (courtesy of Wal-Mart, McDonalds, etc...) and higher dot.com costs (freight) headed into holiday, we still think we're going to see a sharp deceleration in EPS growth for US Retail.

Notable Employment Callout

This is from one of Keith McCullough's notes to clients last night.

With Greece, it’ll be convenient for the Bullish Growth (rates up) camp to forget Friday’s jobs report. But this cycle data doesn’t cease to exist. Instead of writing more words, you can follow the cycle (in rate of change terms) using Crayola. I still say the US labor cycle peaked in FEB 2015.

Don’t forget that NFP peaks, on average, 3 months AFTER the economic cycle (GDP) has peaked. The US employment cycle peaked, right on time.

OTHER NEWS

NKE - World Cup: Nike adds a third star to United States uniform

(http://fansided.com/2015/07/05/united-states-world-cup-third-star-uniform/)

Ashley Furniture HomeStore to Open Multiple Canadian Locations

(http://www.retail-insider.com/retail-insider/2015/7/ashley-furniture-homestore)

PYPL - PayPal on hunt for takeovers after eBay split

(http://www.ft.com/intl/cms/s/0/0f17aa34-2134-11e5-aa5a-398b2169cf79.html#axzz3f6fKPL6U)

BRIEF-Puma and Kering Eyewear sign partnership agreement for optical frames and sunglasses

(http://in.reuters.com/article/2015/07/06/idINFWN0ZM00920150706)

SHLD - Sears Holding Corporation Announces Expiration And Over-Subscription Of Seritage Growth Properties Rights Offering

(http://searsholdings.mediaroom.com/index.php?s=16310&item=137374)

Tory Burch Sets Paris Flagship

(http://wwd.com/retail-news/designer-luxury/tory-burch-paris-flagship-10174738/)

BLKIA - Bain, Sycamore Circle Belk Inc.

(http://wwd.com/retail-news/department-stores/bain-sycamore-circle-belk-inc-10175037/)

Joe’s Receives Forbearance From Creditors

(http://wwd.com/business-news/financial/joes-forbearance-creditors-loan-10174919/)