All the data points we monitor on the health of the consumer continue to flash RED.

HOUSING CONCERS CONTINUE - Today, the Mortgage Bankers Association’s index of applications to purchase a home or refinance a loan increased 8.2% to 608.3 from 562.3 last week; this was the first increase in a month on the back of lower mortgage rates. The refinancing gauge jumped 15%, while the index of purchases fell for the fourth consecutive week. The purchase Index includes all mortgages applications for the purchase of a single-family home. It covers the entire market, both conventional and government loans. The trends in the purchase index does not bode well for the next data point, existing home sales.

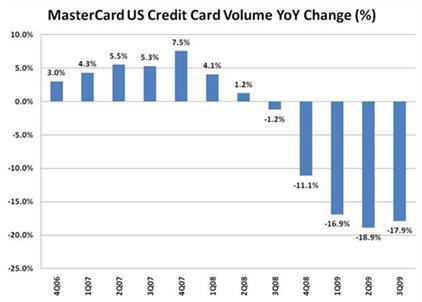

CONSUMER SPENDING PATTERNS - The Research Edge Retail team pointed out that the current results from MasterCard do not support a rebound in underlying consumer discretionary spending patterns.

From the Retails team’s post today – “While showing continued progress on a number of fronts this quarter, MasterCard’s US credit card volume continues to show no meaningful signs of turning around. In fact, credit card volumes for the last three quarters now, on a year over year basis, have been: -16.9%, -18.9% and -17.9%; not the kinds of numbers that signal a recovery. Granted, the volumes have stabilized and importantly they have arrested the decline that was in place from 2Q08 through 1Q09, but since then we have yet to see them move decisively back towards the positive column, which is what we’d expect to see amid the backdrop of a real (vs. perceived) recovery. For reference, credit card volumes are a better proxy than debit cards for the discretionary side of the US consumer’s wallet, as consumers tend to revolve discretionary items, whereas they put staples on debit cards which are paid in full at the time of purchase.”

A DECLINE IN NON-ESSENTIAL CONSUMER SPENDING – The following is from a post that the Gaming, Lodging and Leisure team did on the subject of consumer spending:

TODD JORDAN: GAMBLING ON THE CONSUMER

Our macro math suggests declining discretionary spending over the next 5 quarters. It could be even worse for casinos since their share of the discretionary wallet is already on the decline.

GDP = C + I + G + (EX – IM). While the G may be expanding, C probably won’t. Discretionary sectors are likely to see a smaller and smaller proportion of the consumer’s “wallet” over the next year or so. As shown in the table below, our macro forecasts and healthcare cost projections indicate that 2010 will bring an accelerating drop in non-essential consumer spending, culminating in a $124 billion year over year decline (-11.4%) in Q3 of 2010. Q3 2009 is looking more and more like an anomaly which makes it a very difficult comparison. Due to leisure spending, both lodging companies and the cruise lines reported better than expected Q3 revenues. For all of 2010 Research Edge projects a 5.2% decline.

Despite GDP growth and the market rally since March, unemployment continues to increase. As we have written about at length recently, gas prices are also going to negatively impact consumers’ spending power for the remainder of 2009 and into 2010. For consumer spending on casino gambling and hotels, in particular, our post, “WHAT GOES UP…” (09/10/2009), shows that gaming is in a mean reversion period in terms of a percentage of personal consumption expenditure. Gaming was strongly levered to the fifteen-year rip in housing-fueled PCE that ended in 2008. A one-two punch of a smaller allocation of a more frugal consumer’s wallet could meaningfully impact the gaming industry’s top line next year.

TOM TOBIN: HEALTHCARE AND THE CONSUMER

The Consumer is a dominant factor in understanding the future of Healthcare spending and Healthcare equities. What is typically thought to be a defensive sector and a safe haven in turbulent times, has been tightly linked with the health of the consumer since the beginning of 2009. Healthcare consumption has been taking larger percentages of consumption, currently riding above 21.8% today. There is a limit to how high this percentage can go, and further deceleration in consumer spending will accelerate the discovery process. The leverage points vary across the Healthcare landscape. There are the obvious Healthcare Discretionary stocks such as Aestheticsn (AGN, MRX) where the consumer impact is well known, but virtually no Healthcare Subsector has been left untouched in 2009. Managed Care is the only group positively exposed to pressure on healthcare consumption through the Medical Loss Ratio. Knowing where the consumer is heading will tell us where we need to be focusing both long and short.

We remain short the XLY (Consumer Discretionary ETF) in the Virtual Portfolio.

Howard W. Penney

Managing Director