“Think left, and think right, and think low, and think high – oh, the thinks you can think up if you only try!”

-Dr. Seuss

Apologies in advance for keeping it too simple this morning, but after introducing single-shot Hedgeye Cartoons in the last year we may have to resort to full-form illustrative children’s books in order to explain this Greek debt drama.

Oh “No!”, you say? Or is that what they said? And now that’s just a visceral feeling about being levered long beta instead of rotating all of your stock market gains into Treasury Bonds as Global Equity market volatility breaks out to the upside?

Think about managing inflation expectations risk during #deflationary shocks. Think sell high and buy low.

**Join Keith McCullough live at 8:30am ET on The Macro Show. Just click here.

Back to the Global Macro Grind…

As our new Hedgeye European Strategy Contributor, Daniel Lacalle, wrote in his risk management note about Greece last night (read it here): “The referendum is not the end of the Greek drama. It is the beginning of the real drama.”

And I’ll piggy back on that by linking the drama that is this clown Varoufakis to the real story in Global Macro markets this morning which is #Deflation.

To review how the #Deflation blew up many a levered long “guy” from July 2014 to January 2015:

- Euros were being burnt to a crisp as Draghi did whatever it took to “reflate” asset prices

- #StrongDollar was born out of that and the inverse-correlation trades perpetuated by it

- Almost everything Inflation Expectations (Oil, levered Energy stocks, Junk Debt, EM, etc.) deflated

And what are you seeing in marked-to-market terms this morning?

- Down Euro, after failing @Hedgeye TREND resistance of $1.13

- #StrongDollar breaking out again > @Hedgeye TREND support of $95.51

- Oil (WTI) -3.7% to $54.78, Peripheral Debt Down, Emerging Markets Down, etc.

Contextualizing this immediate-term reaction obviously matters, so let’s do that vs. last week’s moves:

- US Dollar Index +0.6% last week = +19.7% year-over-year

- Euro (vs. USD) -0.5% last week = -18.4% year-over-year

- Oil (WTI) -6.7% last week = -42.4% year-over-year

- Energy Stocks (XLE) -2.0% last week = -25.8% year-over-year

- Russian Stocks (RTSI) -2.5% last week = -33.9% year-over-year

- Emerging Market Stocks (Latin America) -0.9% last week = -25.9% year-over-year

Oh, and don’t tell anyone, but Long-term Treasuries (one of the best hedges against Global #Deflation Risk) had a great end to the week (-8 basis points week-over-week and down another -8 beeps this morning to 2.30%) after a not-great US jobs report.

Oh, No!

No you didn’t. You didn’t think I’d do what all of the mainstream financial media (and most sell-side strategists) are doing this morning and ignore another rate-of-change #GrowthSlowing in US employment, did you?

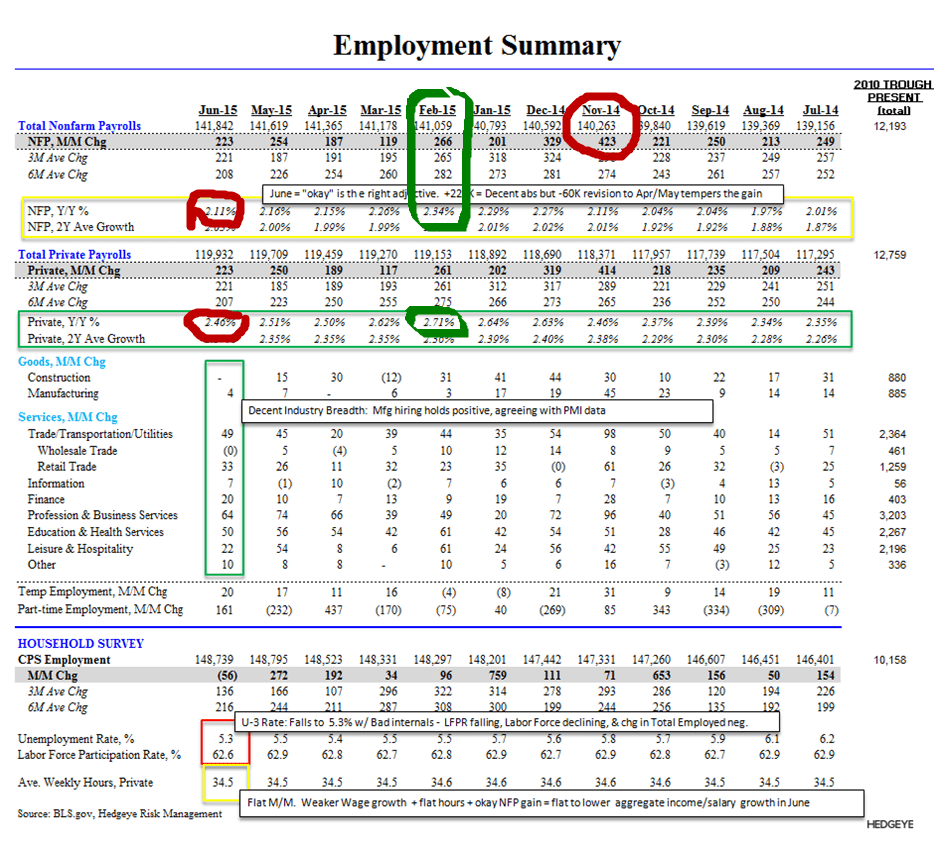

As you can see in today’s Chart of The Day (I did the Crayola coloring myself over the weekend), the peak in a classic #LateCycle US economic indicator (non-farm payroll growth) was 4 months ago (February 2015) at 2.34% year-over-year.

Oh right. I am sure European and US equity beta has bounced “off the lows” again on some kind of a “summit” of central-market-planners in Europe tomorrow. So let’s stop with the US cycle slowing analysis and get back to the Greek drama:

- Italian Stocks (MIB Index) -2.8% lead losers this morning after deflating -5.4% last week

- Italian and Portuguese 10yr Yields are +10-11 basis points to 2.34% and 3.02%, respectively

Oh, that’s not Greek. That’s the Italian and Portuguese stuff. Right, right. I’m hearing things are fantastic in both of those places from a secular growth perspective and that their “credit” risk should trade in line with US Treasuries…

Or should they trade higher? Thinking lower? I thought every market risk eventually meant higher prices (after the central planning response)? “Oh, the thinks you can think up, if you only try!”

Our immediate-term Global Macro Risk Ranges are now (intermediate-term TREND views in brackets):

UST 10yr Yield 2.21-2.40% (bearish)

SPX 2043-2092 (bearish)

RUT 1 (bearish)

Nikkei 20004-20554 (bullish)

VIX 15.02-19.94 (bullish)

USD 95.51-97.42 (bullish)

EUR/USD 1.09-1.13 (bearish)

YEN 122.21-124.4.60 (bearish)

Oil (WTI) 54.53-57.94 (bearish)

Nat Gas 2.69-2.87 (neutral)

Gold 1161-1191 (neutral)

Copper 2.51-2.66 (bearish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer

Click to enlarge