Key Takeaway:

While most US investors are looking at the big carnival in Greece and Europe this morning, we'd suggest they look in the other direction, towards China, where the real action is happening.

Chinese equity prices are down ~30% in a month. In a month! Meanwhile, prices of Chinese steel continue to collapse (see our chart below) - an indicator we've long watched as a representation of the real underlying activity of China's economy - falling another 2.7% week-over-week. The bottom line is that real economy in China is under growing pressure and the stock market is now collapsing.

As we pointed out last week, the real gauge of whether Europe poses risk to the US is best reflected in the overnight interbank lending markets. This risk can be measured in the TED Spread domestically and in Euribor-OIS in Europe. Neither of these measures have done much of anything on the Greece news. In other words, contagion fears are unfounded for now. If this changes, and those spreads begin to widen we'll be on top of it, but for now Greece/Europe are not pressing issues for the US Financials.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 12 improved / 7 out of 12 worsened / 4 of 12 unchanged

• Intermediate-term(WoW): Negative / 0 of 12 improved / 7 out of 12 worsened / 5 of 12 unchanged

• Long-term(WoW): Positive / 3 of 12 improved / 2 out of 12 worsened / 7 of 12 unchanged

1. U.S. Financial CDS - Swaps widened for 19 out of 27 domestic financial institutions. Once again, financial protection providers MBIA and Assured Guaranty led the way, widening by +132 bps to 749 bps and by +59 bps to 396 bps respectively.

Tightened the most WoW: CB, MTG, RDN

Widened the most WoW: MBI, AGO, MMC

Widened the least/ tightened the most WoW: SLM, SLM, SLM

Widened the most MoM: MBI, MMC, AGO

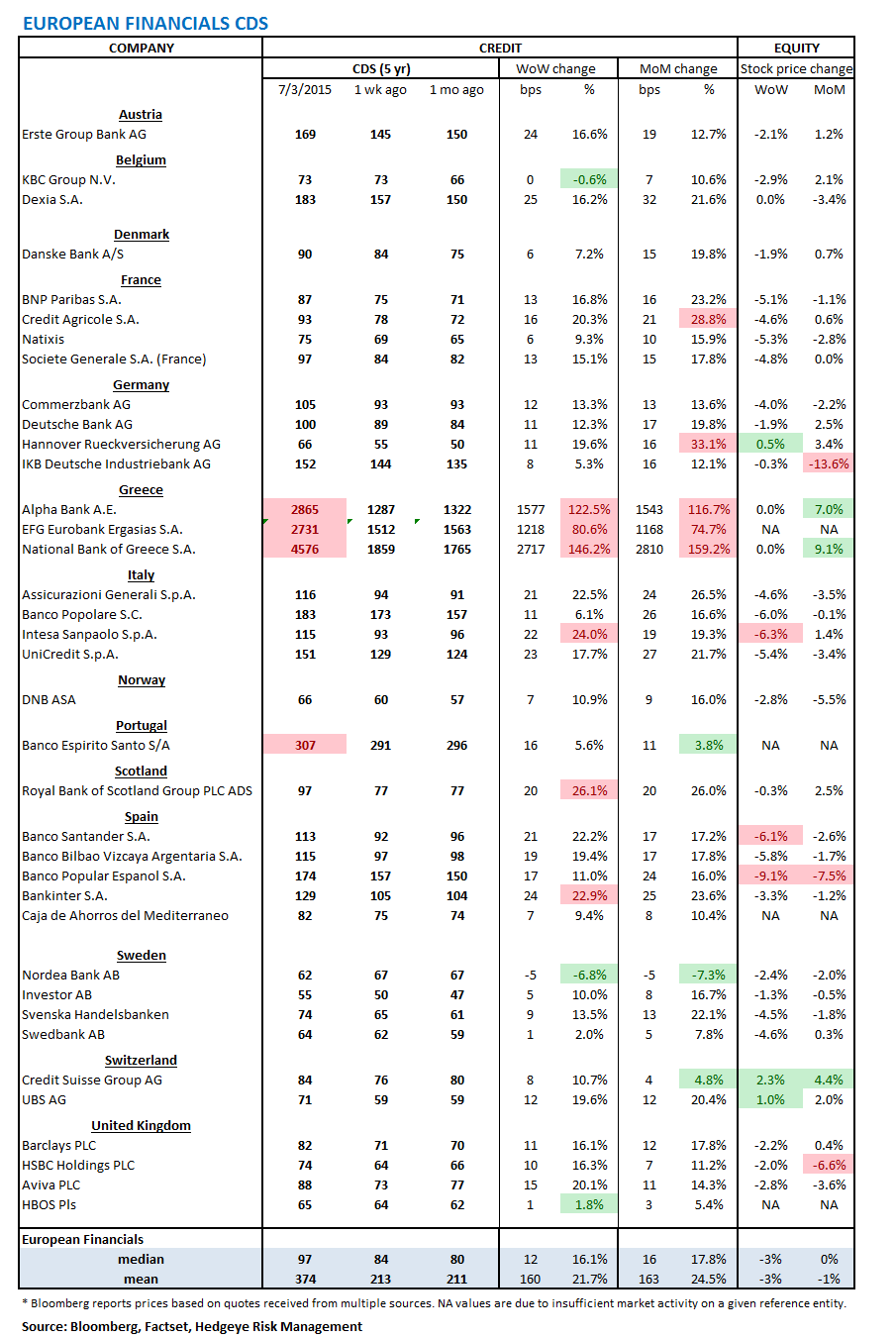

2. European Financial CDS - Swaps mostly widened in Europe last week in anticipation of Greece's referendum. Over the weekend, that referendum took place, and Greek citizens voted to reject the terms of the bailout package offered by the country's creditors. The median and average changes in swap spreads were +12 bps and +160 bps, week-over-week. CDS for Greek institutions blew out by over 1000 bps each.

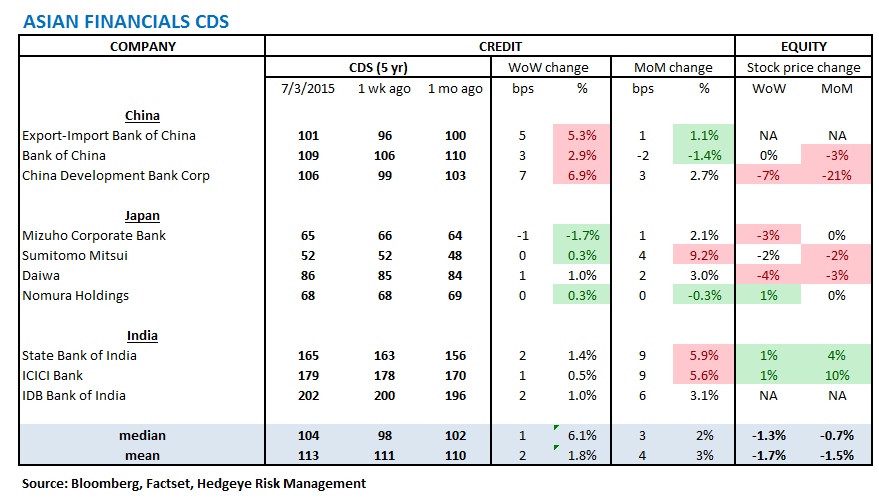

3. Asian Financial CDS - Swaps on Asia banks mostly widened last week with an average change of 2 bps.

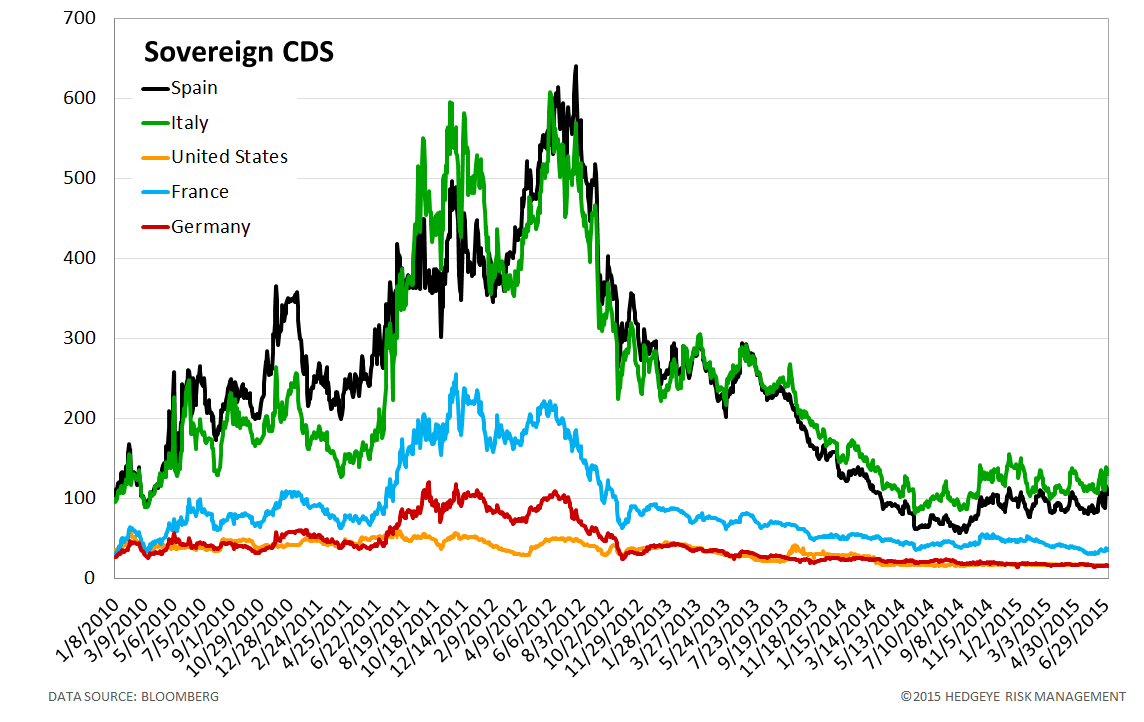

4. Sovereign CDS – Sovereign Swaps mostly widened over last week, led by Italy, Spain, and Portugal on contagion worries. Those sovereigns' CDS widened by 24 bps to 134, 20 bps to 109 and 39 bps to 202 respectively.

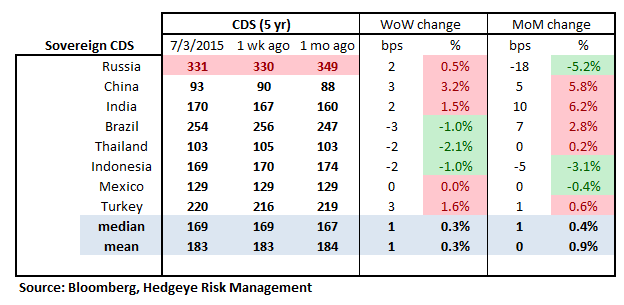

5. Emerging Market Sovereign CDS – Emerging market swaps mostly widened last week. Movement was moderate; the most significant was the 3 bps widening in Chinese CDS to 93 bps.

6. High Yield (YTM) Monitor – High Yield rates rose 24 bps last week, ending the week at 6.62% versus 6.38% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 2.0 points last week, ending at 1891.

8. TED Spread Monitor – The TED spread was unchanged last week at 28 bps.

9. CRB Commodity Price Index – The CRB index rose 0.2%, ending the week at 225 versus 224 the prior week. As compared with the prior month, commodity prices have increased 0.9%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 11 bps.

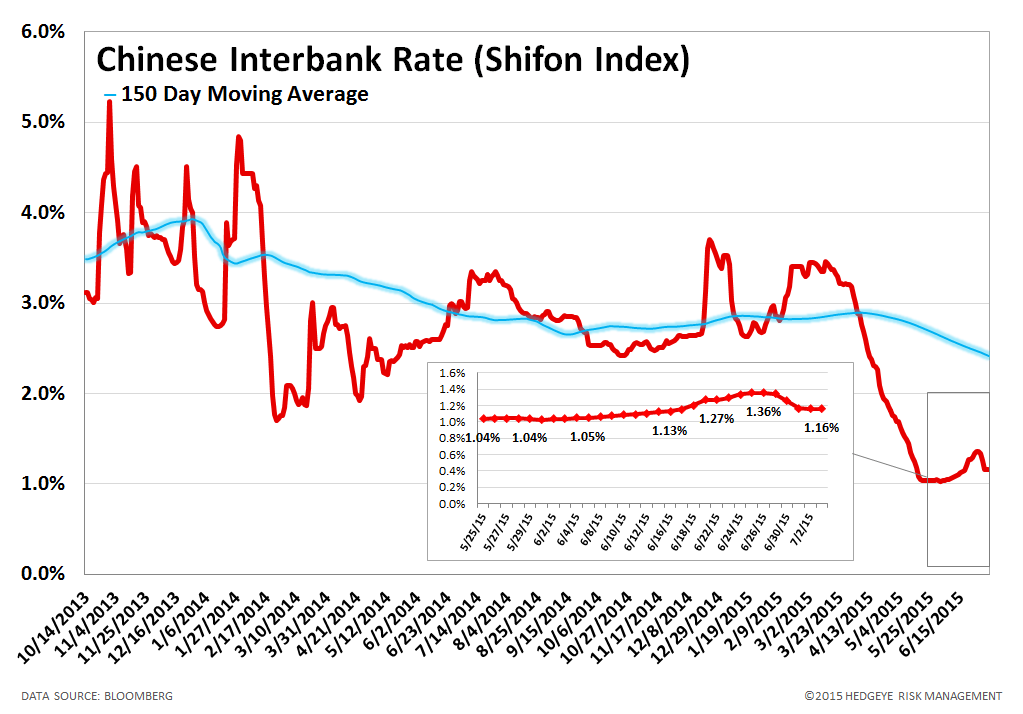

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 20 basis points last week, ending the week at 1.16% versus last week’s print of 1.36%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 2.7% last week, or 61 yuan/ton, to 2165 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

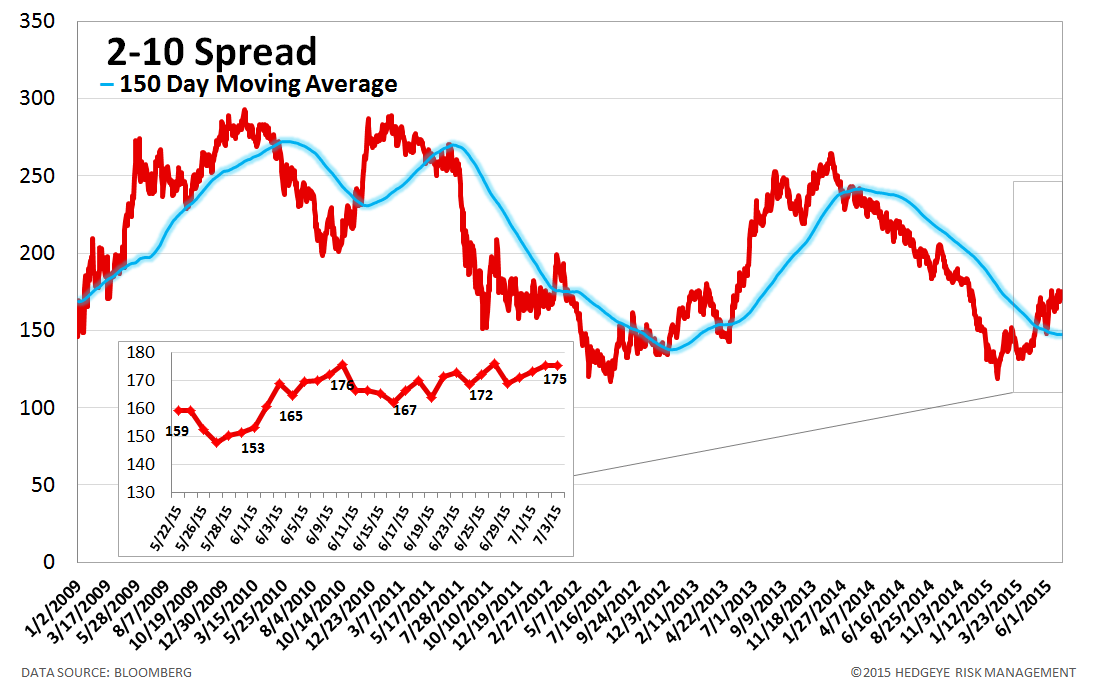

13. 2-10 Spread – Last week the 2-10 spread tightened to 175 bps, -1 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

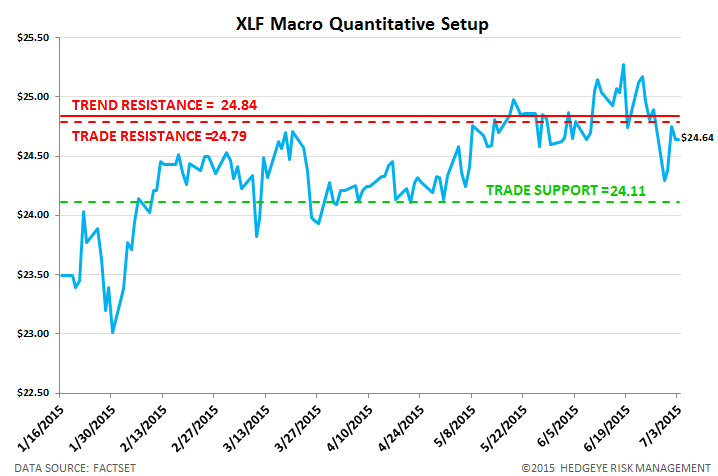

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.6% upside to TRADE resistance and 2.2% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT