Editor’s Note: This is a special, complimentary excerpt from today’s morning strategy note written by Hedgeye CEO Keith McCullough. If you're interested in raising your Macro IQ and staying a step or two ahead of consensus, you may want to consider becoming a subscriber.

* * * * * * *

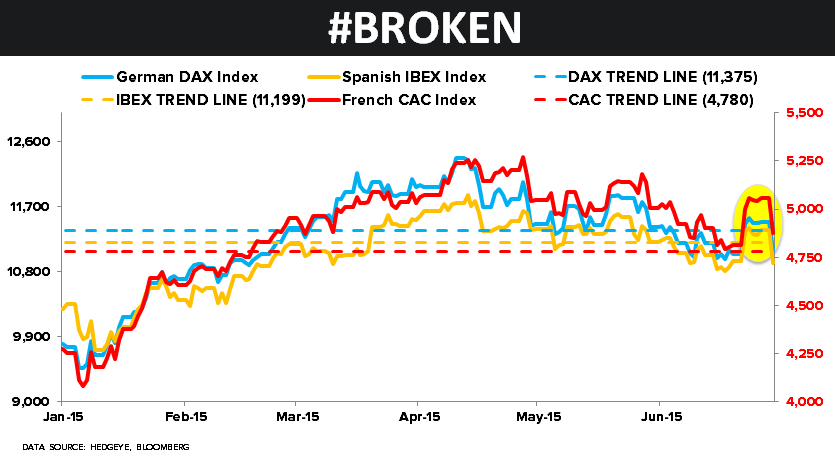

Are European Equities undergoing what we call a Bullish-to-Bearish TREND Phase Transition?

Since:

A) We have slower-for-longer estimates for real European GDP growth than consensus for 2H of 2015

and

B) My risk management signal says this recent 3-month breakdown (TREND duration signals) is real – for now my answer is yes.

To review some key European Equity market TREND levels that have broken:

1. German DAX = 11,375

2. French CAC = 4,780

3. Spanish IBEX = 11,199

Implied by those signals (since I have price, volume, and volatility calculated within each) is RISING VOLUME (on down days) and RISING VOLATILITY in terms of how I measure it within my immediate-term risk range #process.

The other obvious thing the manic-financial-media tends to miss when its pundits navel gaze at equity indices being “off the lows” is cross-asset-class risk management correlations and signals.

Look at this morning’s move in Global Bond Yields, for example…

Click here to begin your subscription.