The question everyone needs to ask is why is a highly levered 38 year old regional QSR chicken chain trading at 17.8x EV/NTM EBITDA?

Only one reason - market insanity!

Currently Bojangles’ (BOJA) shares are trading at approximately 17.8x EV/NTM EBITDA, or an approximately 27.7% premium to the mean of three other regional chicken companies (LOCO, FRGI, and PLKI). That being said, it’s also not hard to make the case that LOCO and FRGI are overvalued too, making BOJA even more ridiculously overvalued.

What this extreme valuation does not account for is:

- It’s a hybrid asset light business model

- Bojangles’ operates in highly competitive segment with many well-established and well run peers companies, especially Chick-fil-a

- Decelerating SSS growth

- Decelerating traffic trends

- Declining margins due to persistent commodity pressures (specifically, chicken)

- Poor unit economics outside the core markets.

KEY TAKEAWAYS

BULL CASE IS UNLIKELY - The bull case for BOJA is grounded on BOJA’s strong fundamental momentum will continuing for years. If this scenario holds true, the current estimates could prove conservative in coming quarters and years, making the stock a LONG. This seems like a scenario that is grounded on aggressive assumptions that may prove unsustainable. My read on the fundamentals suggest that there is little leverage in the business model or upside to the current estimates, making the stock severely overvalued.

The concept would need to generate high-single digit same-store sales to provide enough upside to justify the numbers. The street has modeled 4.2% system SSS in 2015E (4.3% company; 4.2% franchised), driven by the combination of: (1) 3%+ menu pricing (significantly above pricing taken in recent years); (2) continued market-share gains; and (3) growing brand awareness in non-core markets.

NEW UNIT ECONOMICS DON’T ADD UP - Consistent with our other calls on overvalued small cap restaurant stocks, centers around unit economics and the company’s ability to grow successfully. On the surface the numbers don’t add up for Bojangles’.

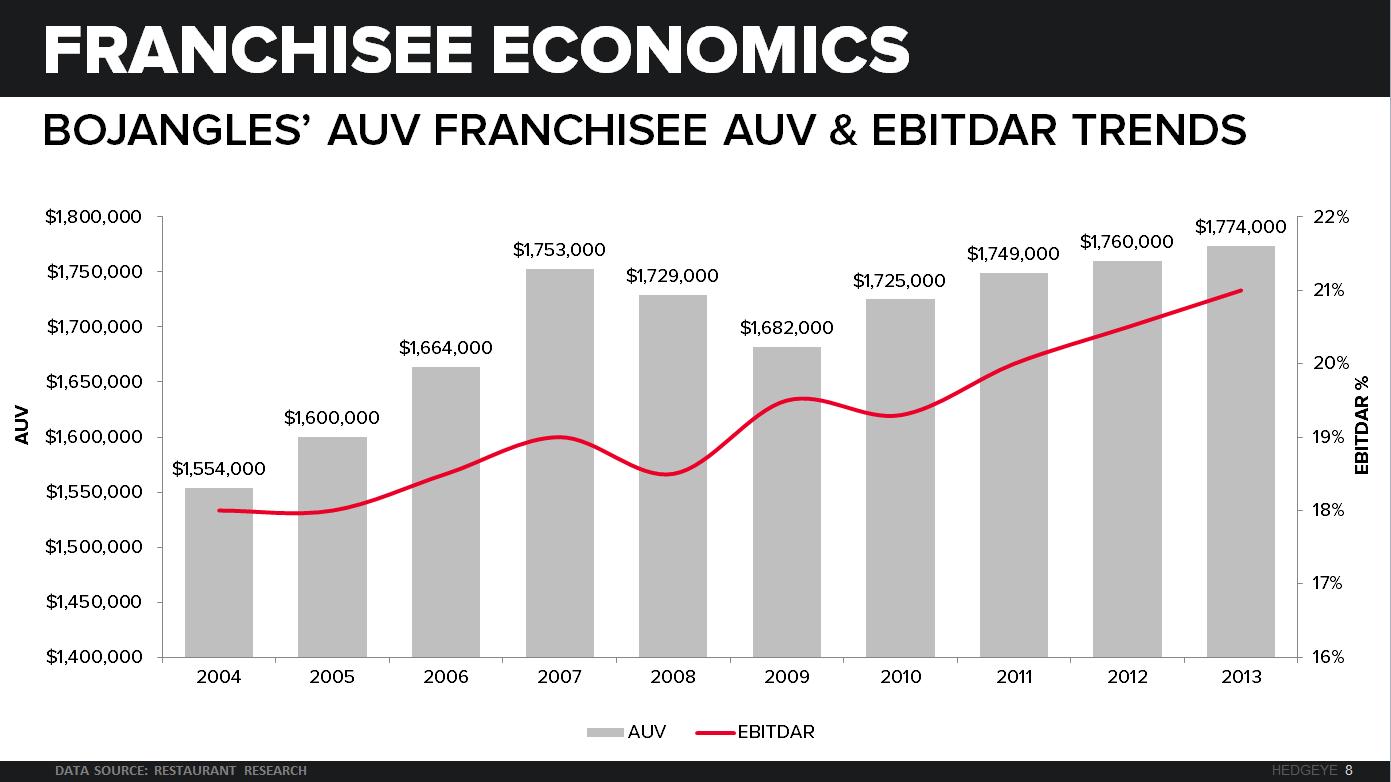

A new Bojangles’ restaurant has an average total investment cost of slightly more than $2.1 million, which includes the building, site development costs, soft costs (environmental costs, legal, etc.), furniture, fixtures, and equipment and land. The average unit volume of a Bojangles’ is $1.7MM and $1.5MM for new units in non-core markets. This puts the concepts sales to investment ratio (including real estate/rent) at .76, one of the lowest in the industry and suggests you should not be allocating capital to that investment.

Unless you are using someone else’s capital!

Does that make the Bojangles’ 20-year-plus history of using build-to-suit financing to fund its company-owned development the right strategy? I suspect there is significant limitation to this strategy and part of the reason why the company is only a regional chain after being in business for nearly 40 years.

While the financing strategy allows the company to control all aspects of site selection and construction for a very low net cash investment (up-front cost to open a restaurant go from $2.2 million to $145,000 per location), it puts significant limitations on site selection and geographic expansion. The company’s unique “build-to-suit” financing is available only for freestanding locations where the underlying land is available to purchase. In-line development options are not option for this strategy.

The developers who are putting up the capital, front the cost of everything but the equipment. This implies that the company pays a high-single-digit to low-double-digit occupancy costs as a percentage of sales over a fixed 15-year lease term.

On the franchise side, Bojangles’ delivers a high-teens fully capitalized return for franchise restaurant development when accounting for a 4% franchise royalty, which is in line with the unit-level economics performance seen by the quick-service peer group. The average ROI characteristic, its build-to-suits strategy suggests that BOJA has limited regional opportunities further supporting why BOJA is overvalued.

In preparation for its IPO, Bojangles’ system-wide unit growth has accelerated over the last three years, increasing from 5.9% in 2012 to 7.2% in 2013 and 7.8% in 2014. Consensus estimates have unit growth to remain in the 7% to 8% range annually. New store development is largely focused on increasing the concept’s penetration within its existing geographic region of the southeast.

As a result, we expect adjacent market openings to represent 60% to 70% of new locations in 2015 and more than 75% over the next five years. By 2020, 47% of concepts total locations will be in adjacent markets 34% in 2014. New stores in adjacent markets have lower margins dragging down the company margins.

SAME STORE SALES - In the recent past BOJA has used price as the primary driver of same-store sales. Going forward, guidance is for low-single-digit same-store sales primarily driven by 2%-3% pricing and flattish to traffic. In 2015, we expect the price benefit to be above average at roughly 3.5%, reflecting 1% of incremental price taken in March and another 1% planned for July to offset higher chicken costs.

COMMODITY COSTS - Chicken represents Bojangles’ largest single commodity exposure at approximately 38% of cost of goods sold, and will likely drive the majority of the mid-single-digit commodity basket inflation expected in 2015. After chicken, the next largest components of Bojangles’ food basket are wheat/grain at 14%, vegetables at 12%, and pork at 10%. Again, why is a chain that uses price to protect margins, with no traffic growth trading a premium valuation?

LOW AND DECLINING MARGINS - Restaurant level margins are trending downward, expected to decline ~154 basis points from 15.46% in FY14, to 13.92% in full year FY15, primarily driven by higher cost of sales as planned price increases will not fully offset the impact of higher chicken prices. While we project some moderation in commodity costs beginning in 2016, we expect restaurant-level margin to remain in the mid to low 14% range, given an increased skew toward lower margin adjacent markets.

IN CLOSING – BOJA appears to be a company with decent growth, but we must harp back on the fact that it is a 38 year old regional chicken chain. We strongly doubt that they are going to experience the same success they do in their core market in new markets as they expand. Additionally, same-store sales are being led by price increases as they try to compensate for rising commodity costs. This company is not deserving of its current valuation ― as margins decline to their final resting place and same-store sales are recognized for their inflation due to pricing, the company will be seen for what it truly is, a 38 year old regional chicken chain.