***JOIN US LIVE AT 8:30AM ET FOR A SPECIAL GREECE EDITION OF THE MACRO SHOW WITH HEDGEYE CEO KEITH MCCULLOUGH AND EUROPEAN ANALYST MATT HEDRICK. CLICK HERE.

“You learn a lot more from the lows because it makes you pay attention to what you are doing.”

-John Elway

What are you doing this morning? I assume what you need to do is a function of what you already did. Were you set up for Greece being “saved” again? Or were you taking down your exposure on last week’s European “bounce”?

Like any world class athlete, you have to really pay attention to what you are doing when risk is rising. From a cyclical investor’s perspective, that risk typically manifests at the end of a cycle, not the beginning.

With China, Europe, and the US slowing (at the same time) into the back half of 2015, you may very well have to get used to the manic media talking about markets being “off the lows” this summer – that’s what happens on the way down.

Back the Global Macro Grind…

Both levels and liquidity will matter most this morning. At 2AM EST, European Equity Futures had both the German DAX and French CAC indices down around -5% - four hours later, they were “off the lows” at -3%.

But unless you can contextualize risk (price, volume, volatility) across multiple-durations and cycles, what precisely does down -3% or -5% (or US Equity Futures down 35 or 22 handles) actually mean?

If your #process is chasing weekly charts and trivial moving monkey averages, would you say that on a week-over-week basis nothing actually happened within the aforementioned % moves?

- EuroStoxx600 was +2.9% last week

- Germany’s DAX was +4.1% last week

- Greece was +16.0% last week

Or no? As long as the Greeks don’t let their markets (or banks) open, no worries, I guess. Oh, and if you’re one of the poor bastards who doesn’t trade markets and just wants some of his money back, too bad – you get 60 euros, max, per/day.

On liquidity, #newsflash: there is none.

So that’s a pretty easy risk to contextualize in both equity and fixed income terms. But what about the levels? Are European Equities undergoing what we call a Bullish-to-Bearish TREND Phase Transition?

Since A) we have slower-for-longer estimates for real European GDP growth than consensus for 2H of 2015 and B) my risk management signal says this recent 3-month breakdown (TREND duration signals) is real – for now my answer is yes.

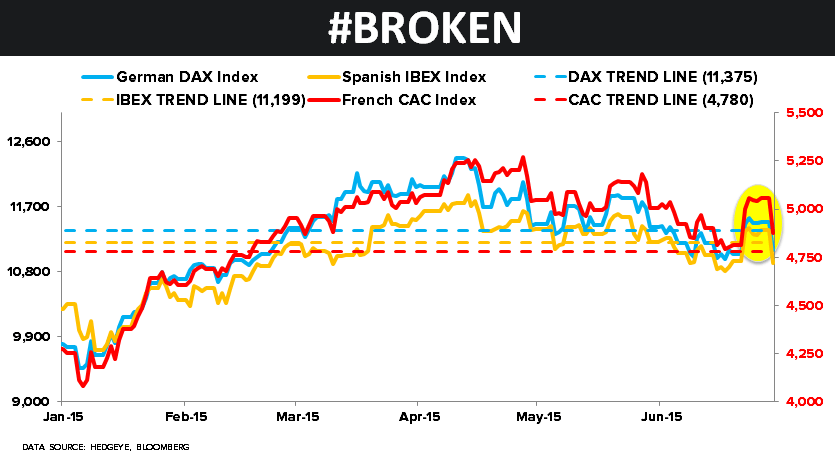

To review some key European Equity market TREND levels that have broken:

- German DAX = 11,375

- French CAC = 4,780

- Spanish IBEX = 11,199

Implied by those signals (since I have price, volume, and volatility calculated within each) is RISING VOLUME (on down days) and RISING VOLATILITY in terms of how I measure it within my immediate-term risk range #process.

The other obvious thing the manic-financial-media tends to miss when its pundits navel gaze at equity indices being “off the lows” is cross-asset-class risk management correlations and signals.

Look at this morning’s move in Global Bond Yields, for example:

- GERMAN BUNDS: after ramping to lower-highs again last week, 10yr Bund Yields -18bps to 0.74%

- ITALIAN BONDS: after making higher-lows (again) last week, 10yr Italian Yields +25bps to 2.39%

- US TREASURIES: after making lower-highs (again) last week, UST 10yr Yield -13bps to 2.34%

This all came after a horrific week for US Treasuries where the short-end of the curve (2yr Yield) was, allegedly, “breaking out” (for the 4th time since December) but failed, miserably, again at 0.75%, falling back to 0.64% this morning.

While last week was a Dollar Up, Rates Up (USD +1.5% on the week vs. the Euro) week, this morning is the ole Dollar Up (small), Rates Down (hard) move that reminds you of the mother of all risks you saw from SEP-JAN. #Deflation

Got Debt #Deflation?

Greek Bond Yields (10yr) are +346bps this morning to 13.94%. No Sir “growth is back” chart chaser, that is not “off the lows.”

I think we’ll all learn a lot from this momentum-chasing-cycle slowing; especially if you didn’t learn anything from the last two US cycle tops (2000 and 2007) or the long-term-secular one that’s driving Europe toward another devaluation.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.18-2.48% (bearish)

SPX 2079-2110 (bearish)

DAX 10,5 (bearish)

Nikkei 191 (bullish)

VIX 13.70-16.07 (bullish)

USD 93.96-97.11 (neutral)

EUR/USD 1.10-1.14 (neutral)

YEN 122.25-124.99 (bearish)

Oil (WTI) 57.87-61.13 (neutral)

Nat Gas 2.66-2.89 (neutral)

Gold 1165-1205 (bullish)

Copper 2.57-2.68 (bearish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer