Below are Hedgeye analysts’ latest updates on our eleven current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each. Please note we added ZOES (please watch the video below) and KATE this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

Despite a recent bounce, the euro has fallen 18% since this time last year.

IDEAS UPDATES

FNGN

FNGN still has room to grow. Our bullish thesis is built on the following:

- Independent advisory works and boomers need advice - “Help” services including independent advisory or proper use of target date funds empirically result in meaningful outperformance compared to “Non Help” returns which can greatly assist 401K participants in achieving their goals.

-

Glacial and not massive shift is occurring in the retirement market -

Much has been made of the Baby Boomers starting to redeem retirement assets and pull in their 401K wealth. While survey data is relaying that 2014 was the first year on record with more withdrawals than contributions, the drawdown is slight and won’t be immediately impactful.

-

AUC and providers win should rebound the stock - Our research shows that AUC and not earnings drive the stock, and with a new product in Income Plus and potentially a new provider coming on, the stock with very high short interest and positive near term catalysts should rebound. We see $55 per share before $35 per share as an outcome.

PENN

PENN remains one of our Gaming, Lodging and Leisure Team's favorite names on the long side and maintains the best new unit growth story in domestic gaming. PENN’s new property, Plainridge Park in Massachusetts, had a strong opening.

We expect slot win per day of $400, above Street expectations. In addition, June state gaming revenues will begin to roll out in 1-2 weeks. We expect June to be as strong as May, setting up Q2 to be estimate-beating quarter for PENN.

ITB

Builders and housing related equities turned in a 3rd week of outperformance alongside continued strength in the New Home Market, a notable uptick in 1st-time buyer activity in the Existing Market and strong results out of homebuilder Lennar (LEN).

EHS | 1st-time Buyers Stirring: First-time buyers represented 32% of Existing Sales in May, up from 30% last month and 27% in May of last year. It’s been our view that ongoing improvement in labor and income fundamentals along with maturation of the employment recovery beyond the 2-year mark for the key 20-34 year old age demographic would support household formation growth with slow flow through to demand in the single-family market.

It’s difficult to take a convicted view of a single month of data in isolation but with investor/distressed sales declining, mortgaged purchases rising and young buyer demand percolating the slow march towards market normalization is progressing.

Whether the mini-step function rise in 1st-time buyer demand in May represented a head-fake or an early inflection back towards the historical average of ~40% share of EHS remains to be seen but its evolution will represent a fulcrum factor for the direction of the existing market from here with transaction activity having retracted back to longer-term historical averages.

Indeed, the sequential +5.1% rise in May took aggregate existing sales up to 5.35MM units SAAR, marking the strongest level of housing demand since the artificially (tax-credit) amplified late 2009 period.

Further, the high-frequency weekly Purchase Application data from the MBA – which clocked purchase demand growth at +18% year-over-year in the latest week – suggests the strength observed across Pending and Existing Sales in March/April extended to May/June.

New Home Sales | Acceleration Continues: New Home Sales in May rose +2.2% month-over-month to +546K, the strongest level since February 2008 (88 months). On a year-over-year basis, sales growth registered +19.5% with the positive revision to the prior month (+1.3% MoM) taking April sales growth up to a remarkable +30% year-over-year. Given the favorable comp dynamics, it’s likely we see similar strength from a rate-of-change perspective in the coming months. For context, if sales were to hold flat at current levels, year-over-year growth would come in at +34%, +35% and +20% over the next 3-months, respectively.

LEN | Pick Your Metric: Similar to what we saw from KBH last week, LEN beat across basically every operating metric in 2Q15 with top and bottom line, deliveries, new orders, pricing and home sales gross margins all coming in ahead of estimates. Company Commentary was upbeat with management raising its outlook for deliveries, highlighting continued strength in rental demand/occupancy and pointing to ongoing improvement in demand in new single family construction.

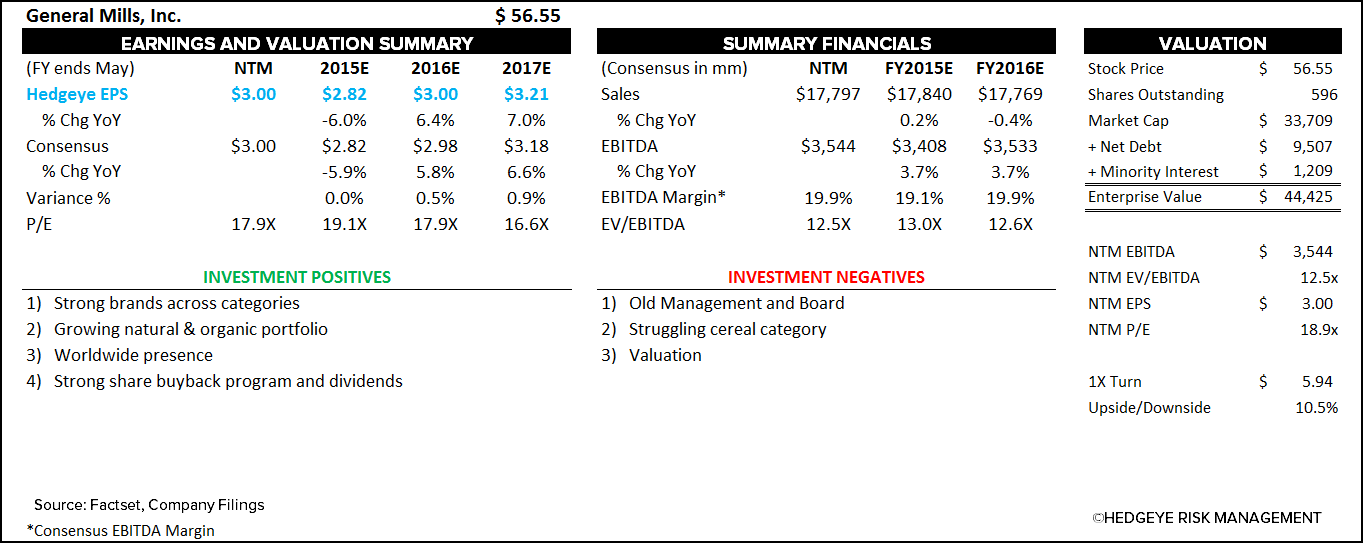

GIS

Nothing has changed to our bullish General Mills (GIS) thesis. We are still long for all the same reasons reiterated below. Earnings are coming up on July 1st, which will be a big date for us.

We remain very bullish on the strength of General Mills’ brands and the long-term growth potential of the stock. The 2015 fiscal year was a busy one for GIS as they underwent a major restructuring project and the $820MM acquisition of Annie’s.

As they enter FY16, they announced Project Compass on 6/25/15; this is a cost cutting initiative similar to Project Catalyst, which will be taking place in the International segment. This restructuring effort is expected to be completed by early fiscal 2017, and will generate approximately $45 to $50 million, with approximately $25 to $30 million of cost savings being realized in fiscal 2016.

We don’t believe this should be a sign that times are still bad at GIS. With Project Catalyst recently ending in February, the organization simply needed time to digest learnings and then implement the initiatives across the broader organization. Albeit small in actual dollars, management continues to impress us with their willingness to make the tough calls that are necessary to succeed.

We see multiple ways you can win being LONG GIS:

1. The current management transforms into an Activist management team -15% chance

2. Fundamentally – Gluten Free Cheerios is a home run – 40% chance

3. Management sells the company – 10% chance

4. An Activist shareholder takes a position – 35% chance

All-in-all this stock is built for growth and with it currently paying a generous 3.1% dividend, that has never been decreased or interrupted, it is a worthwhile bet that this ship will turn.

TLT | VNQ | GLD | EDV

After a Fed-fueled week of strength in slow-growth, yield-chasing asset classes and long duration fixed income, both the Dollar and interest rates re-couped their losses from Fed Week. The dollar declined, rates increased, and as a result, those long of gold took some pain:

- TLT: -2.9% on the week as the ten-year ripped 20 bps to the upside

- EDV: -4.7% on the week back below the pre-Fed lows

- VNQ: -4.5% on the week on the rates move

- GLD: -2.5%--> Gold does not like a strengthening USD and rising rates. It likes a declining USD and declining rates

Will this continue? Will a long, sustained rate liftoff ensue? We don’t think so.

The market traded this week as if Thursday’s trifecta of data points supporting the strength of the consumer (69% of GDP is consumption) signals that the economy is back, and we’re right around the corner from an interest rate tightening cycle. Following up on Thursday’s data releases, the UofM Consumer Sentiment reading on Friday for June accelerated markedly sequentially.

Specifically:

- Real Personal Consumption Expenditures (PCE) growth accelerated in May on a sequential, trending, and longer-term basis

- The savings rate ticked lower by 30 bps implying the strength behind our consumer-led economy (i.e. acceleration in PCE and more spending, less saving)

- For the second consecutive month, aggregate wage growth is accelerating on both a 1 and 2-year basis

Sure, the consumption side of the economy looks good for now, but how about the early-cycle manufacturing side which is the first to crack? Looks awful. To add to the apparent recent strength of the consumer, we outline a few headwinds for the consumer that has directional GROWTH, INFLATION, and POLICY implications into the second half of 2015:

- The labor market always looks great at the end of an economic cycle, as we’ve emphasized exhaustingly. An increase in hours worked and hourly wages, as reported with PCE on Thursday, speaks to the nature of our position in the current cycle.

- Retail gasoline prices are up +40% off of their March lows as we enter the height of driving season in the U.S.

- With our internal models signaling that the economy faces very difficult comparisons in 2H2015 vs. prior periods (Y/Y of course), we would need to continue seeing a trend in data supporting an inflection in the direction of the consumer.

We continue to repeat that the chance of further downward revisions to forward looking growth estimates from the Federal Reserve and consensus macro is much more likely than not. The attempted suspension of economic gravity from policy makers weakens the currency and puts pressure on bond yields. We remain long of this set-up with gold and long-duration fixed income.

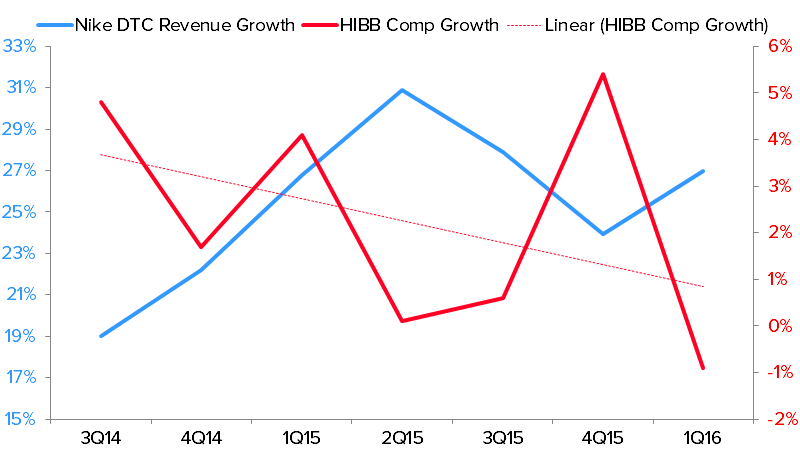

HIBB

Nike has been pushing the Direct to Consumer (DTC) envelope, which includes Nike Stores and e-commerce, and we think that poses a real threat to athletic retailers like Hibbett (HIBB) who now have to compete directly with the brand for sales.

To be clear, Nike has always had a brick and mortar presence and currently runs 180 outlet stores and 33 full price stores in the U.S. But, online is the greatest threat facing the traditional wholesale model because…

1) Customers continue to shift purchases away from brick and mortar

2) Customers prefer to shop directly with the brand over traditional wholesale accounts (one of the key reasons we’ve seen nike.com e-commerce growth outpace its wholesale partners) *based on our survey work

3) it’s a less capital intensive way to reach customers

4) the gross margin for NKE on a direct sale is 1800bps higher than a typical wholesale sale and the actual gross profit dollars are about 4x.

On Thursday, Nike reported their 4th quarter and 2015 fiscal year results. Its Direct to Consumer sales were up 27% with e-commerce sales up 51% accounting for about 45% of the company’s growth. That’s significant for HIBB when you consider the fact that Nike accounted for 55.7% of HIBB's purchases in FY15, and if you exclude equipment upwards of 70%.

As you can see from the chart below, we’ve seen a significant slowdown in the HIBB comp trend as NKE has pushed the pace on its direct business. That will continue to be a sizable headwind exacerbated by the fact that HIBB has no e-commerce operation so they are incapable of capitalizing on the shifting consumer behavior.