As expected DRI put up a very strong quarter, management noting cost cutting, less discounting and an extra week as leading causes. That being said, management is doing a great job getting the cost structure of the company and the margins to return to normalized levels. At this point the stock currently reflects all the good news and is 10% above our sum-of-the-parts analysis.

The key points coming out of the earnings release are:

- Consolidated margins are benefiting from a slight sales tailwind from lower gas prices

- Olive Garden margins are benefiting from less discounting

- Cost cutting is a priority

- The margin structure of the company will change significantly from the REIT transaction

OLIVE GARDEN PERFORMANCE

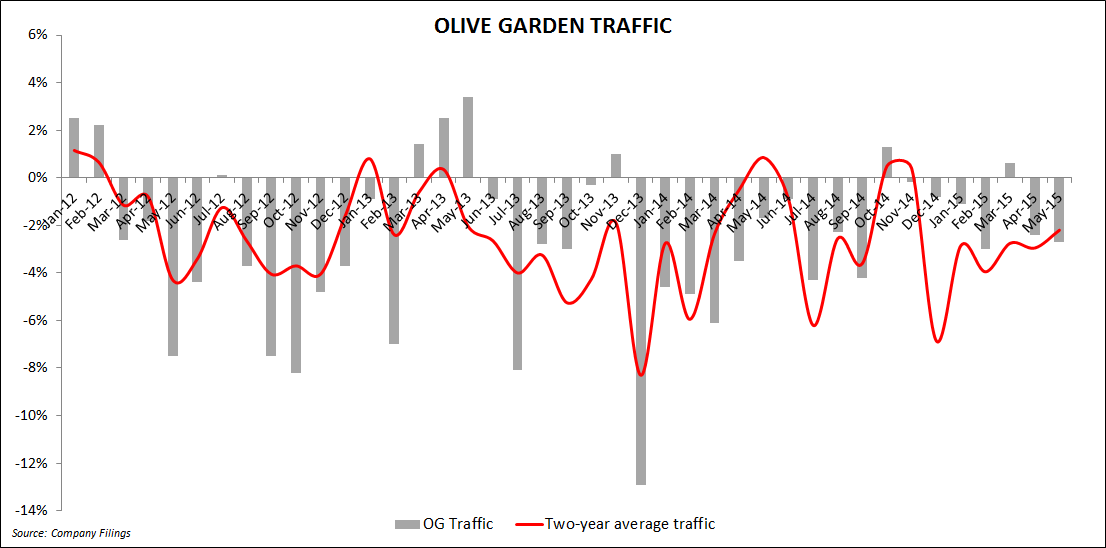

One of Starboard Values top priority’s when getting control of Darden was “substantially improving the value proposition and experience at Olive Garden to increase guest counts.” Part of Olive Garden’s operational improvement plan was to return the concept to its Italian roots, enhance the guest experience all while reducing costs. On this earnings call management provided little evidence that they were focused on returning the concept to its Italian roots. The focus on to-go sales is not a long –term solution. The Olive Garden team has been working on more contemporary concepts, designed to appeal to today’s consumer. And although these concepts may be resulting in improved sales, they are being implemented in a small number of stores and expanding slowly. The speed and breadth of these changes are ultimately not going to be enough to improve their very tired asset base!

While Olive Garden had a better year in 2015 there remains few signs of life that the concept is back on track. As we have said before, the improved profitability at the concept is due to industry tailwinds and less discounting. Management has now set expectations that traffic will be positive in FY2H16, providing little evidence to support that claim. As seen in the chart below traffic trends at the concept remain elusive. The improvements in 2015 same-store sales have been driven by price and mix as traffic remains slightly below industry trends.

FY16 GUIDENCE

- Adjusted EPS $3.05-3.20 vs FactSet $2.88 (before adjusting for the REIT transaction)

- Same-restaurant sales growth (52-week basis) of 2.0% to 2.5%

- Total capital spending of $230 to $255M (very little in this for remodels)

- New unit openings of 18 to 22 restaurants

- Does not include the impact of any fiscal 2016 real estate transactions and related cash and capital structure activities

THE OLIVE GARDEN REIT

Today, Darden announced that its Board approved a strategic real estate plan to pursue a separation of a portion of the company's real estate assets. The separation would be achieved through a combination of selected sale leaseback transactions and the transfer of a portion of its remaining real estate assets to a new REIT that will be separated by a spin-off resulting in the REIT becoming an independent, publicly-traded company.

According to the company there is “a significant amount of work remains and there can be no assurance the company will be able to successfully complete the transaction and establish a REIT.”

If the current plan is consummated, Darden will transfer approximately 430 of its owned restaurant properties to the REIT, with substantially all of the REIT's initial assets being leased back to Darden. The leases are expected to have attractive rent coverage ratios, fixed rent escalations and multiple renewal options at Darden's discretion. The proposed REIT would be well positioned to grow through real estate acquisitions of other assets.

In addition, Darden has been marketing selected properties for individual sale leasebacks. To date, the company has listed 75 properties, and over 30 of these properties have been sold or are under contract. The company expects an average cash capitalization rate of approximately 5.5% for all 75 properties, and expects to close most of these transactions by the end of August. In addition, the company is seeking to sell and lease back its Orlando Restaurant Support Center property and buildings under a long-term contract with multiple renewal options at the company's discretion.

After receiving proceeds from the completion of the strategic real estate plan, the company expects to retire approximately $1B of its debt over time and maintain its investment grade credit profile.

SUMMARY

It is clear that the new Board has DRI headed in the right direction. With the financial engineering aspects of the turnaround nearly complete, the hard part begins, fixing Olive Garden!