“Now we can sit and wait.”

-Wallace Stegner

Allegedly, I’m on vacation this week. There’s nothing like time, fresh air, and space up here on the Big Lake they call Gitche Gumee. “The lake, it is said, never gives up her dead – when the skies of November turn gloomy.”

For those of you who aren’t familiar with either Thunder Bay, Ontario or that Gordon Lightfoot classic… fire it up on your mobile and listen to the ringtone. It will put the manic nature of our profession in context.

The aforementioned quote was one I underlined while I was sitting on the deck yesterday, reading The Angle of Repose. Instead of reacting to every basis point move in the bond market, that’s going to be my call for the summer – sit and wait.

Back to the Global Macro Grind…

After playing with my kids down by the lake yesterday, I came up to the house to see if anything was “going on” in the marketplace.

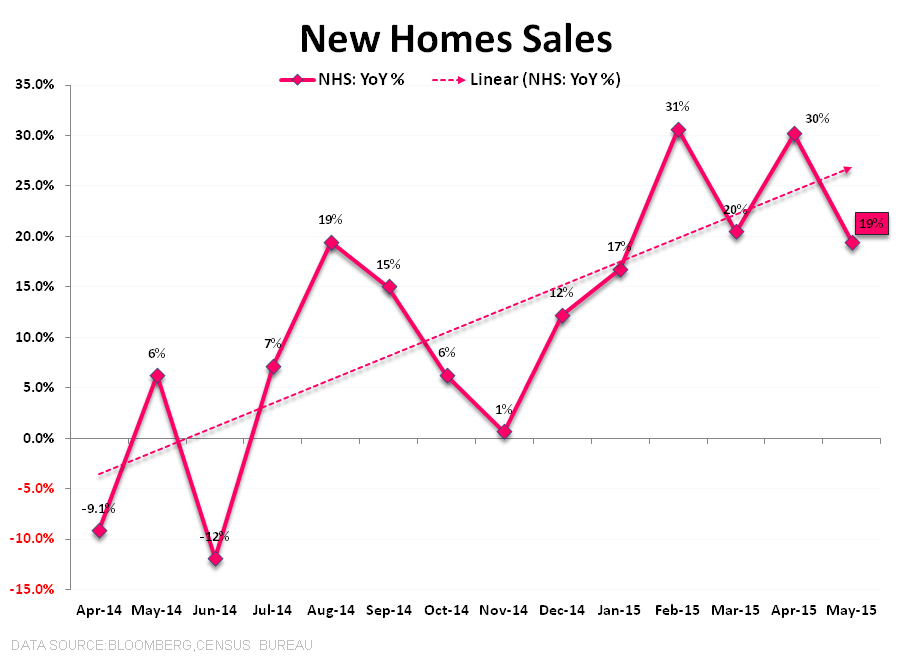

Oh my god – oh my god – after realizing that Hedgeye might be right on US #HousingAccelerating (New Home Sales +20% y/y), the Atlanta Fed “raised its Q2 GDP forecast”. Bond Yields Up, Dollar Up – oh my god… what should I do?

- SHORT US Dollar (UUP) on the overbought signal

- BUY Long-term STRIPS (EDV) on the oversold signal

- SHORT Regional Banks (KRE) on the overbought signal

Crazy Mucker, fading the move. I know.

But does the consensus that had been looking for:

- > 3% GDP

- > 2% “inflation”

- > 3% 10yr Yield

… really think that the US Federal Reserve is going to thwart the only thing other than #LateCycle employment gains that’s shocking bears to the upside right now (US #HousingAccelerating) with a pre-emptive rate hike?

I hope so, because that’s what makes a market.

In other US economic news yesterday:

- USA’s Markit PMI reading for JUN slowed small to 53.4 (vs. 54.0 in MAY)

- US Durable Goods orders dropped -1.8% m/m coming in at -2.5% year-over-year

Yes. That’s a down -2.5% year-over-year recession (post a -3.4% decline in April) in a classic #LateCycle gone bad component of the US economy (and one the Atlanta Fed model didn’t seem to notice).

But the internals of the US stock market did:

- US Industrials (XLI) were down another -0.3% on the day to -1.2% YTD (in a green tape)

- US Healthcare (XLV) was +0.2% day-over-day to +11.8% YTD

But, but… “how can you be bullish on Housing and not the US economy?” That’s easy. Because I am. So tell your friends to stop whining about it and buy ITB (Housing) vs short Industrials and Transports (XLI and ITB).

Housing is early-to-mid-cycle, whereas Industrials are classic #LateCycle. This, of course, is frequently perpetuated by the broader economic slow-down because the Fed typically eases in response to slowing data à rates fall, and housing works.

Oh, but you’re long stocks on a socialization of leverage in Greece?

Roger that. While that wasn’t my catalyst to “buy everything” into and out of the recent Fed acknowledgment of economic slowing (cutting its 2015 US growth estimate to 1.8-2.0%), I certainly didn’t want to fight that “catalyst.”

That said, every macro catalyst comes and goes. Alongside Greek central-planning-spokesman Tsipras driving Bloomberg.com ad revs today with the latest whatever, you’ll get a reminder of Q1 final US GDP this morning.

While US GDP in Q1 wasn’t nearly as bad as where Durable Goods orders and capex have been (year-over-year) in Q2, to the macro headline chasers Q1 will look bad.

So sit and wait. For Long-term Bond Bulls, bad economic data is good. It’s good for Housing and rate sensitive stocks that look like bonds too. If you want to buy something that’s not at its all-time highs, buy those on down days.

If you need me to react to every tick in between, sorry - I’ll be on my deck reading.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.18-2.41% (bearish)

SPX 2105-2130 (bullish)

RUT 1 (bullish)

Nikkei 208 (bullish)

VIX 11.88-14.12 (bullish)

USD 93.94-95.84 (neutral)

EUR/USD 1.11-1.14 (neutral)

YEN 122.39-124.91 (bearish)

Oil (WTI) 59.34-61.90 (bullish)

Nat Gas 2.66-2.89 (bullish)

Gold 1170-1200 (bullish)

Copper 2.55-2.69 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer