TICKERS: LVS, PENN

EVENTS

- June 23 - CCL Q2 2015 earnings 10am

- June 23 - Virgin Cruises Announcement 11am

- June 24 - PENN Opening of Plainridge Park Casino

- June 25 - AC tax bill

Headline News

Macau Junkets - Portion of hotel bookings for Junkets collapses. VIP gaming promoters seeking to accommodate their clients now book between 30% and 40% of all the city’s hotel rooms vs 80-90% previously.

Takeaway: More hotel rooms will have to be sold on a cash basis. RevPAR was already heading lower even before the upcoming room supply increases over the next few years, including 25% growth in 2016.

COMPANY NEWS

LVS - The Venetian Macau rips up their sporting event contract. Initially scheduled to broadcast big sporting events, the Venetian rescinded the contract on June 19th. Spokesperson for the Venetian Macau declined to comment on the matter.

PENN - Plainridge general manager Lance George reported only minor problems during a trial testing. “The restaurants stressed out at lunch time, in the kitchens and in seating people, but that’s a minor stumble. The machines performed beautifully. We are certainly optimistic about opening for real on Wednesday,” he said.

MA Gaming Commissioner James McHugh explained that Massachusetts has the most restrictive gambling law in the country. More casino profits will go into treatment and prevention of gambling addiction than in other states. Slot machines can warn customers when they hit a self-imposed spending limit. There are no free alcoholic drinks. Taxes are higher. And there will be no smoking allowed inside Plainridge or other casinos being developed in Massachusetts. But, at the invitation-only soft opening Monday for the first of those gambling venues, some customers said they like the smoking ban.

Takeaway: We expect stronger than projected results from Plainridge following tomorrow's opening. We're projecting $400 win per day per slot, well above the Street, and our estimate could prove conservative.

INDUSTRY NEWS

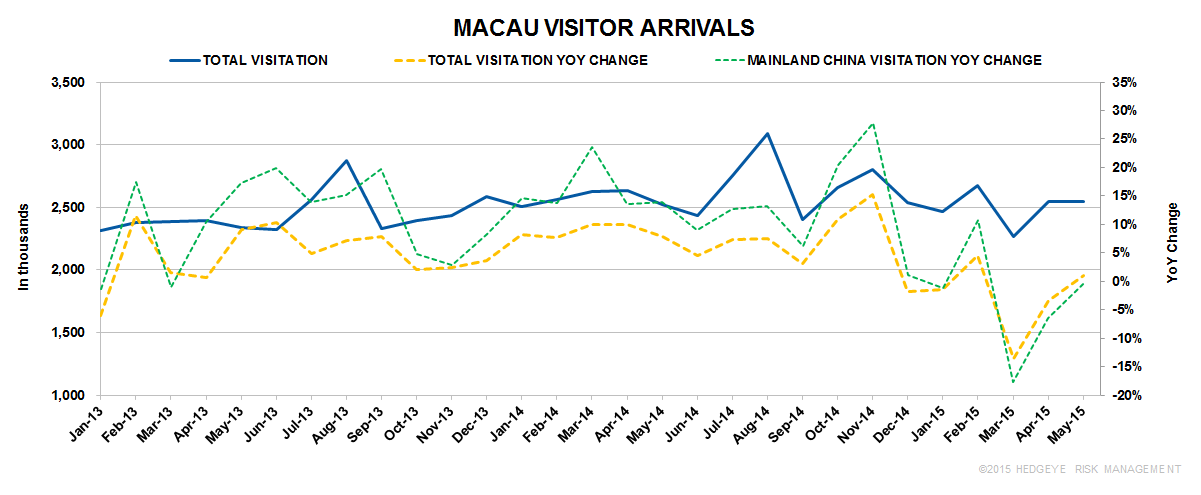

Macau Visitors - The DSEC indicated that visitor arrivals edged up from April 2,547,435 to 2,548,562 in May 2015, an increase of 0.9% YoY.

- Same-day visitors totaled 1,386,839 (54.4% of total), up by 2.6% YoY. The average length of stay of visitors increased by 0.1 day YoY to 1.1 days.

- Visitors from Mainland China totaled 1,690,987, up by 3.6% MoM but down slightly by 0.5% YoY; those traveling under the Individual Visit Scheme increased by 3.5% YoY to 752,982. Guangdong visitation was up 2.4% in May.

Takeaway: Visitation broke a losing streak in May but Mainland China visitation remain negative. June is not looking good.

Massachusetts - Residents of New Bedford, MA, will vote on a proposed $650 million Foxwood resort casino for the city's waterfront. Polls open at 7 a.m. Tuesday and close at 8 p.m. Voter approval is critical for the plan to advance in the competition for the state's third and final resort casino license.

Takeaway: If approved, it is likely that the proposed New Bedford location would lure people from the Cape Cod region, whereas Plainville will service the Central Mass and South of Boston customer base.

MACRO

Asia Macro

- Macau - May CPI +4.93% YoY, up from +4.51% in April

- Singapore - May CPI -0.5% YoY, up from -0.5% in April

- China - Flash PMI 49.6 vs. Consensus 49.4 and 49.2 in May

Hedgeye Macro Team remains negative on Europe

Takeaway: European pricing has been a tailwind for CCL and RCL but a negative pivot here looks increasingly likely in 2015.