Editor's Note: Below is a chart and excerpt from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. Click here to learn more and subscribe.

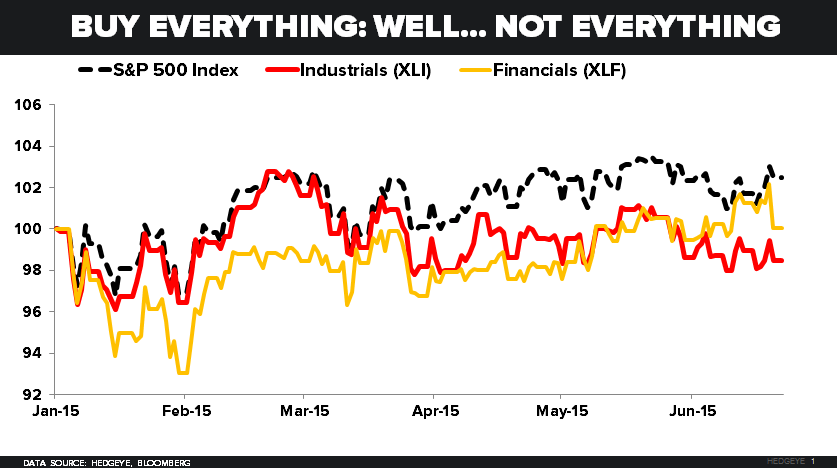

Actually let me take that back – not all “stocks” liked the Dovish Down Dollar + Down Rates move. Here’s how our two favorite S&P Sector Shorts and Global Equities did with the pin tucked in the front, and some USD devaluation tailwind:

- US Financial Stocks (XLF) down -1.2% week-over-week, taking them back to 0.0% for 2015 YTD

- US Industrial Stocks (XLI) down another -0.4% week-over-week to down -1.5% for 2015 YTD

- European Stocks (EuroStoxx600) down -1.0%, taking their 3-month correction to -3.8%