Below are Hedgeye analysts’ latest updates on our ten current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each. Please note we added Financial Engines (FNGN) this week. We feature two additional pieces of content at the bottom.

Levels

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

"You're one bad jobs report away from no September or December rate hike."

-Hedgeye CEO Keith McCullough on Wednesday after FOMC statement

IDEAS UPDATES

FNGN

Editor's Note: The research summary below was written by Co-Financials Sector Head Jonathan Casteleyn.

We added Financial Engines to our Investing Ideas list as a long position this week. In a nutshell, this leading independent 401K advisor continues to grow its market share off of the back of a regulatory tailwind that alludes to corporate responsibility for the performance of retirement plans. Essentially for a annual fee of ~40 basis points or (0.40%), Financial Engines will professionally manage your 401K utilizing the plan’s underlying options. The company’s performance has been effective and the growth/maintenance of retirement assets is vitally important for an aging American population. While most of the Street sees an expensive small cap company with slowing growth, we see a future mid cap stock with more room to grow market share, revenue and EBITDA. With 20% short interest already in the stock, we think these overly Bearish positions will have to be covered as results turn higher adding incremental buying power to this stock.

Our 5 keys tenets for our positive disposition on FNGN stock are:

1.) Independent advisory services are effective, with over 300 basis points in annual out performance versus retirement accounts that do not have an independent advisor. This continues to make the case for ongoing penetration of independent managers and target date funds within the 401K channel.

2.) Regulatory tailwinds are persisting off of the back of the Pension Protection Act of 2006. With the outline of a QDIA in the retirement marketplace, employers may be liable for a retirement plan's under performance. As a result, plan sponsors are continuing to push independent advisory firms into their investment plans and as a QDIA.

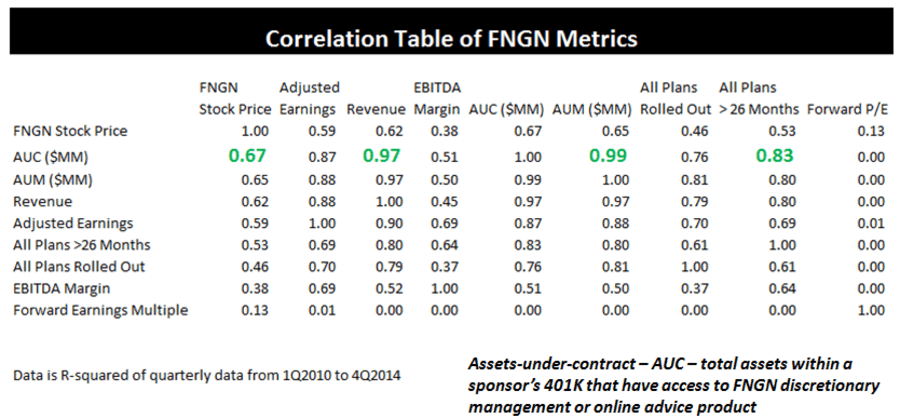

3.) The most important beacon of the health of the firm is assets-under-contract (AUC) in our view. AUC is now inflecting higher year-over-year for the first time in 4 quarters which should force improved revenue guidance for the firm. AUC is strongly correlated to both revenue and assets-under-management for the firm.

4.) The firm's Income Plus product has increased the overall adoption of its services. While there is some overlap with its existing services, Income Plus has almost doubled the uptake of the company's existing professional management product since 2011.

5.) The stock has discounted a lot and short interest balances are near record highs again. The last time open interest was over 20% of float, it was a good time to buy the stock.

OC

The largest player in the U.S. asphalt roofing industry, GAF/ELK, announced on Monday a price increase for its roofing products starting in August (click here to access the announcement).

While it is certainly a positive for Owens Corning that the leader is taking the initiative in announcing price increases – often followed by the rest of the industry – what really matters is the actual deal worked out with the distributor/retailer including rebates and incentives/discounts. If price increase announcements were indicative of what actually happened to prices (and shingle manufacturer margins), OC would be among the most profitable companies in history.

More importantly, the industry seems to have gotten past the 2014 finger-pointing stage. If true, the OC Roofing segment margins should be positioned for a solid rebound as its Insulation and Composites segments continue to strengthen.

PENN

Shares of Penn National Gaming are up approximately 9% since it was added to Investing Ideas on May 26. Our Gaming, Lodging & Leisure team reiterates their high conviction on the stock and notes that Ohio and Kansas have both been super-strong revenue generators in the month of May.

This positive development has has led our analysts to raise their estimates even higher (and we're already the highest on the street...)

ITB

It was a busy week across the housing space with a host of fundamental releases, builder earnings and notable regulatory updates. Net-net-net....the past week offered another positive update on the state of the residential real estate market with housing turned in a second week of strong, positive absolute and relative performance.

To highlight the major releases:

Builder Confidence

The NAHB HMI (Builder Confidence Index) for June surged across all categories and in all regions, posting its best reading in almost 10 years. Further, given the historical tendency for Builder Confidence to front-run negative inflections in headline Consumer Confidence, ongoing strength in the HMI suggests the confidence cycle is not yet past peak.

New Home Starts

Total Starts declined -11% MoM to +1.036 MM units with SF and MF starts declining -5.4% and -20.2% month-over-month, respectively. Context with respect to the Starts figures is key, however. The moderate retreat in May follows the largest sequential increase in 25 years in April which saw Starts rise +22% month-over-month. Indeed, average Total Starts in April-May are +9% above the TTM average and represent the strongest two-month period of activity since 2007. Permits, meanwhile, rose to an 8-year high advancing +11.8% sequentially and +25% year-over-year. The strength in permits augurs forward strength in Starts and suggest residential construction spending will be (increasingly) supportive of GDP growth over the next couple quarters.

TRID

The CFPB announced on Wednesday that it would be delaying the implementation of the new TRID regulations by two months – from August 1st to October 1st. As review, the slide below summarizes the background, challenges and goal of the new regulations. Industry angst has been building into the implementation date and its been our view that integrations challenges could have a modest-to-moderate impact on reported transaction activity. The delayed implementation along with the subsequent enforcement grace period will allow stakeholders to integrate the changes during a seasonally slow period, providing nearly 6 months of ‘live prep’ ahead of the 2016 spring selling season. It also effectively removes a headwind to 3Q performance – a period characterized by seasonally weak absolute and relative performance for the housing complex

KBH Earnings

KB Homes announced strong 2Q earnings results on Friday. The company beat top and bottom line estimates, reported improved gross margins and a rising backlog, offered positive commentary on the current pace of demand/pricing and stepped up their outlook for margins over the balance of the year. In short, the top down inflection in housing fundamentals (ie. demand and price) we’ve been calling for and highlighting since late last year is now showing up in the reported numbers and being embedded in forward guidance from management.

GIS

Nothing has changed to our bullish General Mills thesis. We are still long for all the same reasons reiterated below. Earnings are coming up on July 1st, that will be a big date for us.

We remain very bullish on the strength of General Mills’ brands and the long-term growth potential of the stock. The 2015 fiscal year was a busy one for GIS as they underwent a major restructuring project and the $820MM acquisition of Annie’s.

We see multiple ways you can win being LONG GIS:

1. The current management transforms into an Activist management team - 15% chance

2. Fundamentally – Gluten Free Cheerios is a home run – 40% chance

3. Management sells the company – 10% chance

4. An Activist shareholder takes a position – 35% chance

All-in-all this stock is built for growth and with it currently paying a generous 3.1% dividend, that has never been decreased or interrupted, it is a worthwhile bet that this ship will turn.

TLT | VNQ | GLD | EDV

Got Sturm und Drang?

After all was said and done, rates finished on their lows of the week. The 10-year Treasury yield finished at 2.26%, down -8 basis points on the day, -13 basis points on the week and down -28 basis points from last week's "breakout" highs.

Bottom line right now remains that Lower-For-Longer is firmly intact as long as US #GrowthSlowing is. As Keith pointed out on Friday, Consensus Macro is still stubbornly sticking to the tired idea that rates have to go higher - they just have to... because, they haven't?

All told, it was a great week sticking with the process on the long side of bonds.

Below we feature an in-depth discussion from Senior Macro Analyst Darius Dale which does a thorough job outlining where our macro team currently stands with respect to the Fed, interest rates, markets and economy. The prescient discussion occured just hours before release of the FOMC statement.

Click image to watch

HIBB

At last week's Investor Meeting (and this week at an e-Commerce conference) Wal-Mart management reiterated their commitment to investing for growth in the digital channel. CEO Doug McMillon stated that "priority one is run great stores and clubs right now. Equally important, we've got to build a great e-Commerce and mobile commerce business."

That last part spells trouble for a company like Hibbett Sports where the real estate strategy was centered around leveraging traffic from Wal-Mart stores.

The thought process was simple -- sell higher-priced sporting goods that Wal-Mart doesn't offer and benefit from the foot traffic flow. Hibbett was able to expand and grow in its core Southern market by following Wal-Mart's lead. But that growth strategy is tapped out now. And Wal-Mart is turning toward digital for growth which equals lower foot traffic.

The problem for HIBB is the company can't park next to Wal-Mart online. This means there is limited to no opportunity for growth in Hibbett’s core strategy. Any form of growth from here on out – in existing stores, new stores, and online, will all come at a lower margin.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

no easy fix at twitter

The problem with TWTR is the business model and expectations. Dorsey likely can't fix the former; managing the latter won't be much easier.

fund flows: rotation out of bond products

Investors reallocated funds away from bonds last week and continued to avoid active domestic equity mandates.