RH - Convert Deal Priced, Again at 0% Coupon

(http://ir.restorationhardware.com/phoenix.zhtml?c=79100&p=irol-newsArticle&ID=2060541)

Takeaway: The terms for the $250 convertible bond offering priced yesterday are similar to the deal the company priced in 2014 when it was, to the best of our knowledge, the only small/mid cap company to get a 0% coupon rate. 2015 deal terms are as follows: 0% coupon with a $118 convert price and a hedging mechanism that will offset dilution until the stock hits $189. When all is said and done, we will be looking at ~12% dilution from the two convertible deals once the stock clears $190.

Why now? As we’ve stated many times, RH is the kind of transformative and disruptive growth story that comes along maybe once every decade in retail. But growth does not come cheap. While the company is on the cusp of being cash flow positive, the market is presenting an opportunity – with the stock 5% from its all-time high – to lock up funding for new concepts should they test well. This deal also completely wipes out RH’s net debt position. Simply put, you don’t see great retail concepts with net debt. Now you don’t see it at RH either.

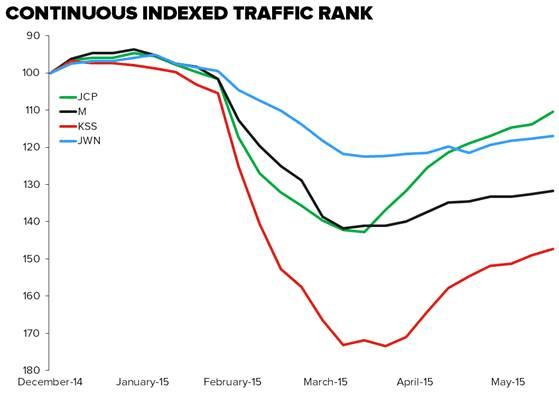

KSS, JCP, M, JWN - YTD DEPARTMENT STORE ONLINE TRAFFIC TREND. JCP/KSS SPREAD WIDENING

Takeaway: This looks at the YTD trends for four retailers in the department store space (JCP, M, KSS, and JWN). The current out performance out of JCP is notable for a couple of reasons.

- Consumers continue to shift online. On a YY basis, traffic ranks are up for the 4 companies charted below between 20-30%, which syncs with what we've seen in either reported numbers or in the case of KSS (which no longer reports DTC metrics) management anecdotes. It's important to note that e-comm sales for the most part in this group have not been incremental, but instead have been cannibalizing Brick and Mortar sales. Take KSS for example which has comped negative in its stores for 13 of the past 14 quarters with DTC growing at a high 20% CAGR.

- That's not a positive for margins as the added cost of fulfilling merchandise is a bps headwind. As the free shipping hurdle moves closer to $0 we should see added pressure.

- The spread between JCP and KSS is widening. That's especially notable given the survey work we’ve done that points to KSS as the biggest beneficiary of the prior JCP share loss (see chart below). The numbers suggest that KSS captured about $1bn of the $5.4bn JCP gave away. WMT is slightly higher, but as it relates to percent of each retailer’s sales, no one even comes close to KSS at 4.5-5.5% of total sales.

OTHER NEWS

NKE - Douglas G. Houser and Orin C. Smith notified Nike of their decision not to stand for re-election

(https://www.sec.gov/Archives/edgar/data/320187/000032018715000062/a8-kbodretirement.htm)

TGT - Target cuts 140 more jobs at Minneapolis headquarters

(http://www.startribune.com/target-cuts-140-more-jobs-at-minneapolis-headquarters/307900011/)

OXM - Thomas C. Chubb III Named Chairman of the Board of Oxford

(http://investor.oxfordinc.com/releasedetail.cfm?ReleaseID=918567)

MSO - Martha Stewart Living Shares Spike on Acquisition Talks

WMT - Report: Walmart puts greeters back in front

(http://www.retailingtoday.com/article/report-walmart-puts-greeters-back-front)