On Monday the UUP, which is the etf for the U.S. dollar index, was down 0.4%, although the dollar is still above the trade line. As a consequence the S&P 500 closed at 1,042, up 0.6% on the day.

On the MACRO front, the S&P 500 started the week on a positive note as the RECOVERY theme came back into focus following some better-than-expected economic data on the continued manufacturing expansion in China. Additionally, in the USA the ISM manufacturing index rose to 55.7 in October from 52.6 in September, ahead of consensus expectations of 53. The headline reading was the strongest since April of 2006, as was the employment component, which jumped to 53.1 from 46.2 in September, moving into expansionary territory for the first time since July of 2008.

The earnings and outlook from Ford was another positive, as was an upgrade of MOT by our Technology analyst Rebecca Runkle, one of her favorite names. While the market finished higher on the day there seemed to be plenty of concerns surrounding last week's selloff and technical deterioration – only one sector is bullish on both the TRADE and TREND. In addition, there is a defensive tone to the market despite some better MACRO data points. Not to mention some cautiousness surrounding Wednesday's FOMC meeting and Friday's release of the October non-farm payrolls data.

Also on the MACRO front, pending home sales increased 6.1% in September following a 6.4% rise in August, significantly above the consensus of 0.00%. September marked the eighth straight monthly gain and the highest level since December 2006, leaving sales up nearly 40% from the January low. This is probably as good as it gets as I would expect to see October pending home sales may see a sharp pullback with the looming expiration of the homebuyer tax credit.

On the day the VIX declined 3.0%, taking a breather from last week’s massive move up.

The three best performing sectors were Industrials (XLI), Consumer Staples (XLP) and Consumer Discretionary (XLY), while Technology (XLK), Healthcare (XLV) and Utilities (XLU) were the bottom three. The only sector down on the day was Utilities.

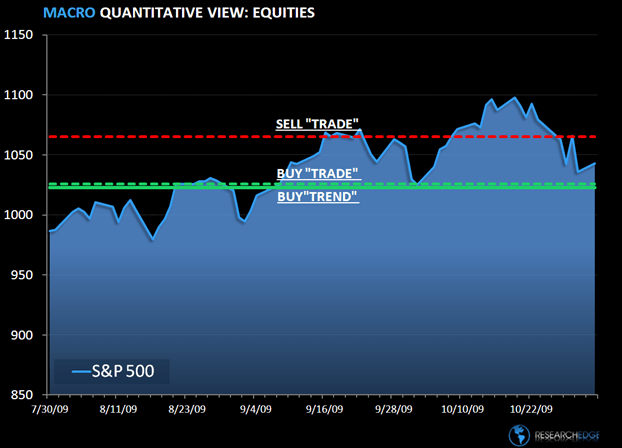

Today, the set up for the S&P 500 is: TRADE (1,026) and TREND is positive (1,023). The Research Edge quantitative models have 7 of 9 sectors in the S&P 500 positive on TREND and 1 of 9 sectors are positive from the TRADE duration. Consumer Staples is the only sector positive on both durations.

The Research Edge Quant models have 2% upside and 2% downside in the S&P 500. At the time of writing the major market futures are poised to open up small to the down side.

The Research Edge MACRO Team.