This note was originally published at 8am on June 04, 2015 for Hedgeye subscribers.

“Above all else, I want you to think for yourself to decide: 1) what you want, 2) what is true and 3) what to do about it.”

-Ray Dalio

If you’re reading this note, you are undoubtedly familiar with Ray Dalio and more than likely familiar with his book Principles. In that book, he details three things:

- The importance of having principles;

- His life principles; and

- How he applies those principles to managing Bridgewater, the world’s largest hedge fund.

While Keith would be the first to tell you that he’s no Ray Dalio, we are also big on principles at Hedgeye.

From a philosophical perspective:

- Transparency: “No banking” means you don’t ever have to worry about what we really think about a specific security or economy. We aren’t trying to sell you anything but our research views.

- Accountability: “No asset management” means we don’t earn a management fee. We only get paid when we add value to our customers’ research processes.

- Trust: “No broker-dealer” means you don’t ever have to worry about us front-running your order flow – or worse…

From a research perspective:

- History: For every indicator we come across, we strive to analyze as much historical data as we can, across cycles, in order to identify or dispel the existence of critical mean reversion thresholds.

- Math: Core to our process is an overt focus on rate-of-change, which is derived from a well-researched view that market participants react to incremental developments, rather than to absolute states. As such, we employ basic differential calculus methods to project accelerations, decelerations and inflections in growth rates.

- Behavioral Psychology: We believe there is a considerable degree of actionable information to be derived from market prices and that contextualizing investor sentiment and positioning is critical to immediate-term risk management. Moreover, we believe the supply/demand narrative surrounding any asset is heavily influenced by its own price trends.

Back to the Global Macro Grind…

Q: What [do] you want?

A: We want to determine whether or not this trending back-up in rates from the JAN 30th lows is a signal for us to: A) abandon our lower-for-longer thesis or B) double-down on said view.

Q: What is true?

A: Supportive of option “A” is 1) the recovery in Eurozone inflation expectations and 2) the recent breakdown in domestic fixed income, credit and equity income plays within our Tactical Asset Class Rotation Model.

Supportive of option “B” is 3) a likely trending deceleration in U.S. economic growth into a likely recession in CY16, 4) secular stagnation brought on by widely misunderstood demographic changes in both the domestic and global economies and 5) a trending material deceleration in global economic growth.

Addressing those factors in order:

- Eurozone CPI accelerated to +0.3% YoY in MAY from 0.0% prior and continues to accelerate on both a sequential and trending basis. Eurozone Core CPI accelerated to +0.9% YoY in MAY from +0.6% prior and is now accelerating on a sequential and trending basis. Moreover, our predictive tracking algorithm has reported inflation in the Eurozone accelerating through the balance of 2015. In light of these developments, it’s no surprise to see that Germany’s 5Y breakeven rate (as a proxy for Eurozone inflation expectations) has backed up +107bps from its JAN 13th low to the current 0.81% – with +38bps of that delta coming in the last week alone!

- Without running the risk of boring you with the details of how TACRM is constructed, it’s worth noting that the model issued a “DECREASE Exposure” signal for the “Domestic Fixed Income, Credit and Equity Income Plays” primary asset class during the week-ended MAY 8th. Since then, the Bloomberg U.S. Treasury Bond 10+ Year Index has declined -3.4%, extending its YTD decline to -5.0%. From a bottom-up perspective, the eight factor exposures (out of ~200) exhibiting the greatest degree of negative VWAP momentum across multiple durations on a marginal basis are explicit bets on lower interest rates: AGG, LQD, BND, FLAT, TLT, BNDX, ZROZ and EDV. Conversely, the three factor exposures exhibiting the greatest degree of positive VWAP momentum across multiple durations on a marginal basis are explicit bets on higher interest rates: KRE, STPP and IAI.

- We discussed this thesis in great detail in a note earlier this week (CLICK HERE to review).

- Ditto.

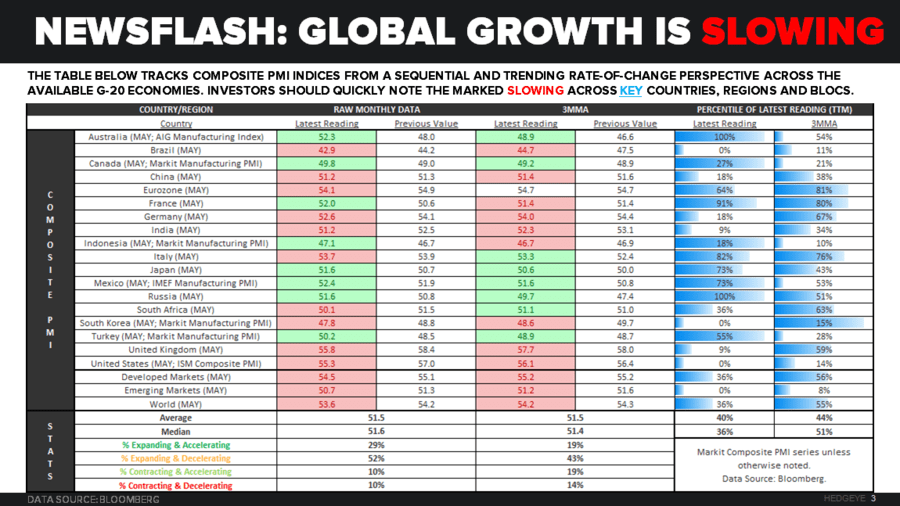

- Keith and I make a point to visit each of our top customers at least ~1x/quarter. That adds up to a lot of meetings over the course of a year and a lot of travel all across the country and globe (e.g. we’re in CA next week and in London the following week after having done Chicago, Boston, NYC, Greenwich and Kansas City in the past three). The point I’m making is that we hear the perspectives of all types of investors and can readily glean when a view is becoming consensus on the buyside. Currently, one of those consensus views is an assertion that global growth is accelerating and/or poised to accelerate.

Nothing could be further from the truth.

In fact, anyone who does the work will arrive at the conclusion that global growth is slowing on both a sequential and trending basis into the most difficult compares of the year (i.e. the 2nd and 3rd quarters).

As such, the probability for global growth to get cut in half on a YoY basis in 2015 is extremely great. That would represent the slowest rate of global growth in this cycle and ~100bps shy of the trailing 3Y average of +2.2%.

Fortuitously for you, you don’t have to do the work because you pay us to have your back on all things Global Macro. If you do nothing else for the rest of the week, the one thing you must do is download the following presentation which quickly contextualizes the rapidly deteriorating global growth picture: http://docs3.hedgeye.com/macroria/Is_Global_Growth_Falling_Off_A_Cliff.pdf.

All told, if Industrials (XLI) is your best idea on the long side of U.S. equity sectors, then now is the time to start working on thesis drift…

Q: What [do you want] to do about it?

A: All things considered, we want to take advantage of this weakness in long duration securities to double-down on our lower-for-longer thesis.

Going back to Draghi’s press conference yesterday, we will note that he was keen to address recent bond market volatility by reiterating that ECB QE will continue as planned throughout the stipulated duration of the program – which is at least through SEP ‘16 and until the ECB sees a “sustained adjustment in the path of inflation” towards its goal of +2%. As such, investors needn’t worry about an untimely removal of the ECB’s bid from European sovereign debt markets.

The immediate-term risk to that decision is that the MAY Jobs Report is strong and the Fed anchors on that as justification for pulling forward their guidance on “liftoff” timing in the JUN 17th FOMC statement.

The intermediate-term risk to that decision is that no matter how “data dependent” the Fed claims itself to be with respect to “policy normalization”, they are actually politically motivated to move the Fed Funds Rate well off of the zero bound no matter what. In light of the aforementioned global growth trends, that is definitely a view being intensely scrutinized across global macro markets right now.

The long-term risk to that decision is that “we are all dead” anyway…

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.03-2.39% (bearish)

SPX 2098-2130 (bullish)

USD 94.73-96.78 (neutral)

EUR/USD 1.07-1.14 (bearish)

Oil (WTI) 57.32-61.91 (bullish)

Nat Gas 2.52-2.67 (bearish)

Gold 1175-1210 (bullish)

Keep your head on a swivel,

DD

Darius Dale

Associate

Click to enlarge