Our macro math suggests declining discretionary spending over the next 5 quarters. It could be even worse for casinos since their share of the discretionary wallet is already on the decline.

GDP = C + I + G + (EX – IM). While the G may be expanding, C probably won’t. Discretionary sectors are likely to see a smaller and smaller proportion of the consumer’s “wallet” over the next year or so. As shown in the table below, our macro forecasts and healthcare cost projections indicate that 2010 will bring an accelerating drop in non-essential consumer spending, culminating in a $124 billion year over year decline (-11.4%) in Q3 of 2010. Q3 2009 is looking more and more like an anomaly which makes it a very difficult comparison. Due to leisure spending, both lodging companies and the cruiselines reported better than expected Q3 revenues. For all of 2010 Research Edge projects a 5.2% decline in discretionary consumer spending.

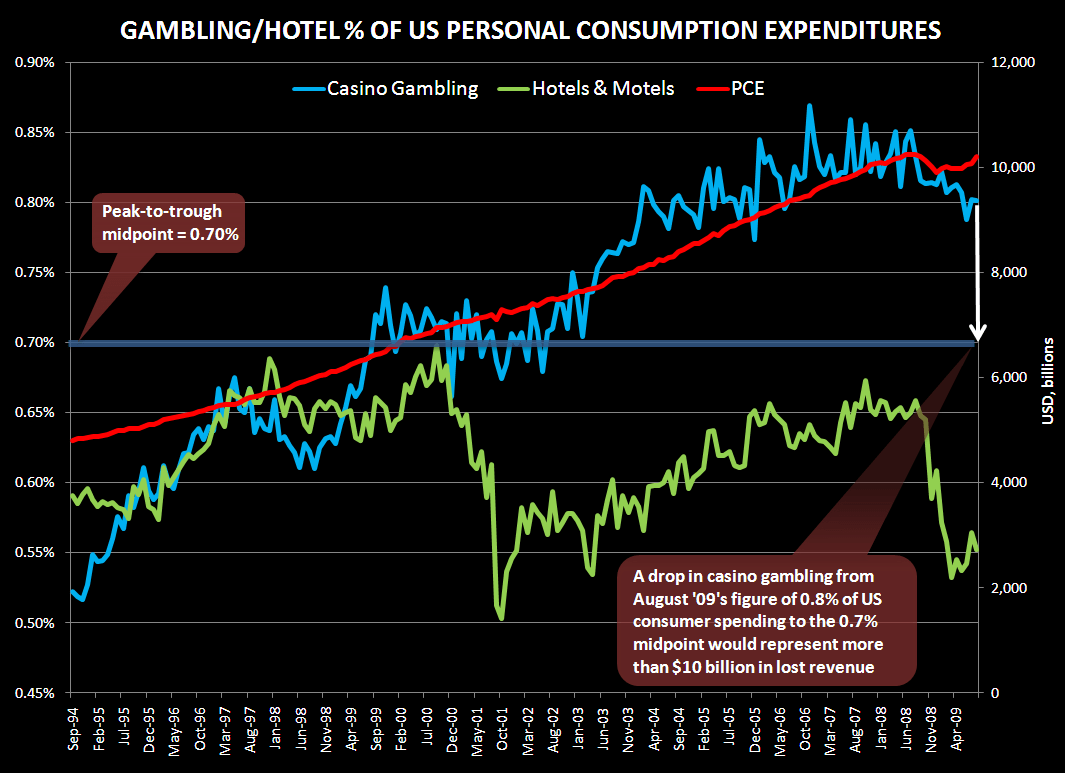

Despite GDP growth and the market rally since March, unemployment continues to increase. As we have written about at length recently, gas prices are also going to negatively impact consumers’ spending power for the remainder of 2009 and into 2010. For consumer spending on casino gambling and hotels, in particular, our post, “WHAT GOES UP…” (09/10/2009), shows that gaming is in a mean reversion period in terms of a percentage of personal consumption expenditure. Gaming was strongly levered to the fifteen-year rip in housing-fueled PCE that ended in 2008. A one-two punch of a smaller allocation of a more frugal consumer’s wallet could meaningfully impact the gaming industry’s top line next year.