UPS Bulk Item Rate Hikes Bad For Retailers

Takeaway: Any way you cut it, this is bad news for retailers. The fact is that consumers increasingly expect retailers to offer up free shipping. In fact, we think that 'free shipping' will be an industrywide standard by the end of 2016. So the question is this -- If the shippers are starting to push back on pricing due to capacity constraints, and if consumers are highly unlikely to broadly accept paying for shipping when it was otherwise free -- then who is going to foot the bill? Yes, the retailers. If the retailers can find a way to push it back to their suppliers, then they'll do it. But very few have that power. This is not what we want to see when retail margins are tracking at an all-time high, and makes it increasingly difficult to be bullish on this group, broadly speaking.

UA - Class C Stock Dividend to Maintain Plank's Control

Takeaway: We rarely see stock splits structured in this manner, but this is all about Plank keeping control of the Board. He's currently sitting on 66.5% of the vote with 100% of the class B stock, but his ownership position has fallen almost 2 percentage points in a year from 18.5% in 2014 to 16.8% in 2015. At an ownership position below 15%, Plank's class B shares would be converted to class A and his grip on the company would be far less secure than it is today. The new class C structure the company announced yesterday is designed 100% to mitigate that risk.

UA, NKE - Sold-Out Curry MVP Shoe Price Doubles Online

Takeaway: This is the first time we've seen UA basketball kicks hit the resale market in a material way. Nike engineered its distribution process to build hype in the aftermarket long ago, and has a few SKUs (The Air Yeezys for example) that are listed on eBay for $10k+. For UA, it's likely more supply than demand related...but whichever way you slice it, it's a win for UA. The company has found a star in Curry. The company has a lot of wood to chop both on the product and infrastructure side before it declares victory -- its footwear sales in 2014 at $430mm were only 25% greater than what Lebron James did for Nike alone. But it now has an asset it can use to grow the platform and demand is building evidenced by the activity in the resale market. The reality is that the technical merits of a product become far less important when they are for an athlete who is as universally likeable as Curry.

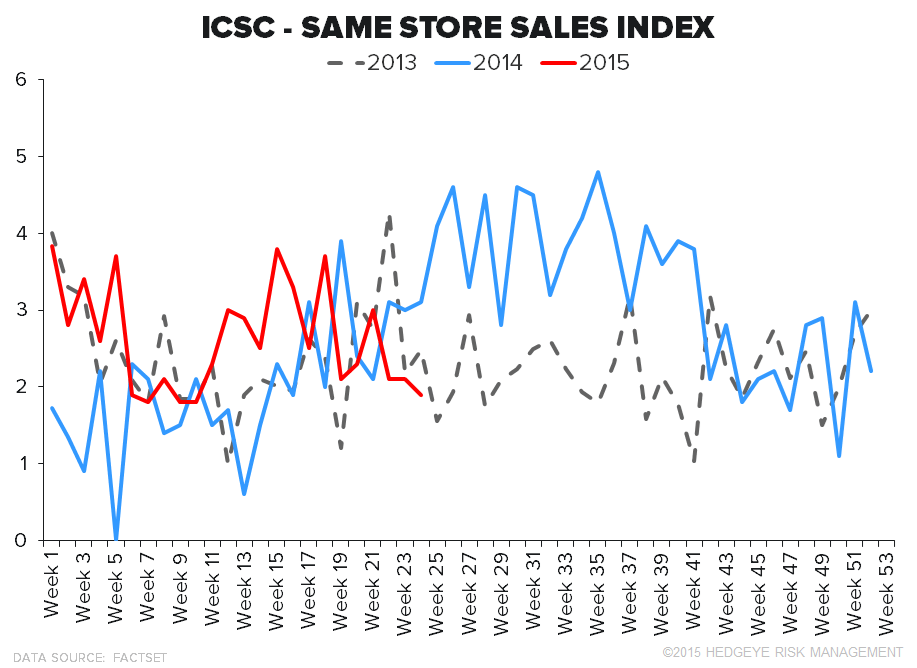

Retail Sales Begin What Should be a 15-Week Deceleration

And so it begins… sales this week according to the ICSC index were up only 1.9%, the lowest rate in 15 weeks. Unfortunately, the weekly sales growth rate should be under added pressure through the end of September (i.e. through back-to-school) as we comp against a solid Summer of 2014.

OTHER NEWS

House Bill Aims to Close Internet Sales Tax Loophole

(http://wwd.com/retail-news/direct-internet-catalogue/internet-sales-tax-loophole-10154767/)

GPS - Gap Closing 175 North American Stores

(http://wwd.com/retail-news/specialty-stores/gap-closing-175-stores-in-north-america-10154542/)

LL - Lumber Liquidators promotes marketing head, cuts merchandising chief

OLLI - Ollie’s eyes IPO and 950 stores

(http://www.retailingtoday.com/article/ollie%E2%80%99s-eyes-ipo-and-950-stores)

Kmart taps DSW executive as marketing chief

(http://www.chainstoreage.com/article/kmart-taps-dsw-executive-marketing-chief)