“There exists limitless opportunities in every industry. When there is an open mind, there will always be a frontier.”

-Charles Kettering

Charles Kettering may be one of the most accomplished men you’ve never heard of before. He passed away some 60 years ago, but his ingenuity lives with us today. As Wikipedia describes him, he was an inventor, engineer, businessman, and holder of 186 patents. The last point is what got me: 186 patents! Now that’s a lifetime of work.

His handwork and ingenuity touched a number of industries– he was responsible for the Freon refrigerant for refrigeration and air conditioning systems, he developed the first aerial missile, and the electric starter for the automobiles. To the point of his quote, Kettering was not afraid of new frontiers.

Speaking of new frontiers, tomorrow the FOMC gives us their rate decision. We aren’t expecting any surprises. We continue to stick with our view (as emphasized in the Hedgeye cartoon below) that economic growth will remain lower for longer, which in turn means that the Fed is likely to be dovish for longer.

The new frontier in monetary policy of course is the Fed’s decision to remain at effectively zero percent interest rates for the last, oh, seven years. Not only has the Fed been more accommodative than any time in its history, but it has been accommodative longer than at any point in its history. In exploring this new frontier, though, the question we should ask ourselves is whether the Fed has completely missed the economic cycle.

Back to the Global Macro Grind...

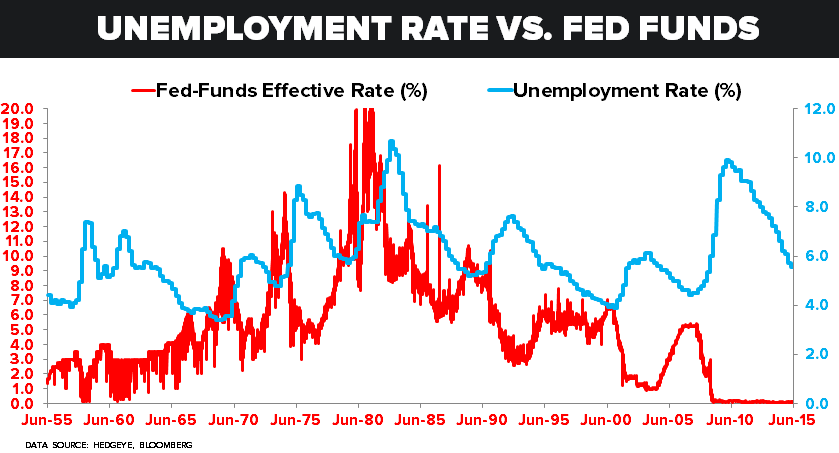

In the Chart of the Day below, we show the Federal Funds rate versus the unemployment rate going back to the 1950s. We don’t need an advanced degree in mathematics to see that this period is different than many others. Despite the unemployment steadily coming down (albeit unemployment is not necessarily the best measure of the health of the employment market domestically), the Fed has, well, not moved.

The challenge now with potentially starting to increase interest rates is that we are very near the top of the business cycle. As we highlighted in our Q2 Themes deck, we are at month 74 of the current expansion. This is in comparison with a mean expansion of 59 months and median of 50 months over the past century.

As it relates specifically to the employment market, initial claims are probably one of the best leading indicators. Currently, jobless claims are in the 300K range, which are literally as good as they get. Historically, going back to the mid-1960s, jobless claim improvement has peaked 7 months before the economic cycle peaks.

So, as it related to a new frontier, we are certainly in one. In fact, we would submit that never before has the perceived plan been to tighten monetary policy into the peak of an economic cycle! Of course, maybe the Fed will actually stay dovish longer than expected...

But if you need any insight of where consensus is on interest rates, look no further than a poll from CNBC (as consensus as consensus gets) this morning. According to the poll, 92% of respondents see a rate hike this year, which is up from 84% in the April survey. The only poll we’ve seen this morning with more certainty is the poll of whether July follows June (93% of respondents believe that to be true).

Other than the FOMC decision tomorrow, the other topic that is dominating global macro market headlines this morning is Greece. Some are calling it a tragedy, some are calling it a victory, and some may even see it as an opportunity. Back in small town Canada, they would probably call it a gong show, but here we are . . . on the brink of another Greek default.

As U.S. centric equity investors, the central question of course is whether Greece defaulting or leaving the Euro really matters. The short answer is probably not. As it relates to Europe, the answer is much less clear. Setting aside the actual financial implications, perhaps the most significant fact is simply that the ECB has provided 118 billion euros in loans to the Greek banking system, which is equivalent to 2/3rds of Greece GDP. That, my friends, is a lot of euros!

The larger issue though is one of confidence- confidence in the euro by outside investors, confidence in the economies in the peripheries such as Italy, Portugal and Spain, and confidence in a European sovereign debt market that is all but priced to perfection. It seems like an elixir for sustained weakness in the euro.

Certainly, though, it is possible that the proposed emergency summit on Greece tentatively scheduled for this Sunday may forge some cooperation between Greece and her creditors. Of course, the reality of that happening is, well, not very realistic. Or as John Lennon said:

“Reality leaves a lot to the imagination.”

Indeed.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.11-2.48%

SPX 2070-2095

Nikkei 20032-20661

VIX 14.20-15.93

Oil (WTI) 58.01-61.90

Gold 1167-1199

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research