After declining nearly -60% in a 9-month period, WTI crude oil has moved 41% off the March lows. The logical question to ask is: what’s changed?

* * * * * * *

Aside from the obvious inflection in expectations for the direction of the U.S. dollar, a good argument can be made that not much has changed from a fundamental perspective. Below we outline the Bull/Bear debate:

BULLISH VIEW

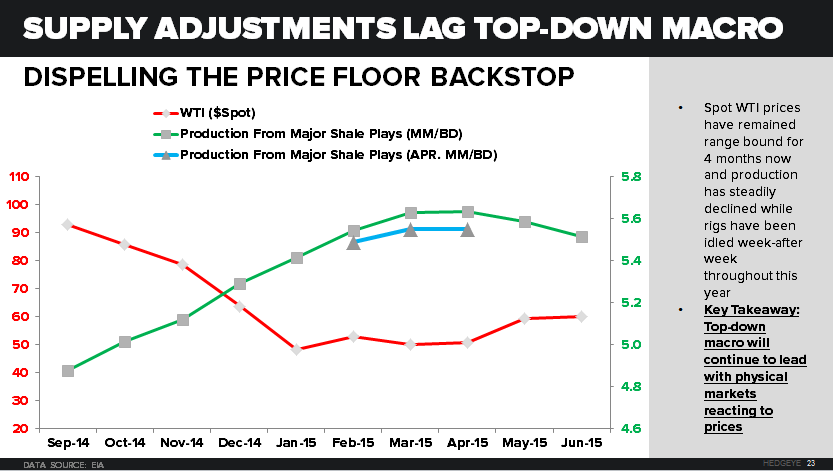

Domestic production growth is decelerating and expected to go delta negative within the next couple of months (production has been much more resilient than originally expected—See below)

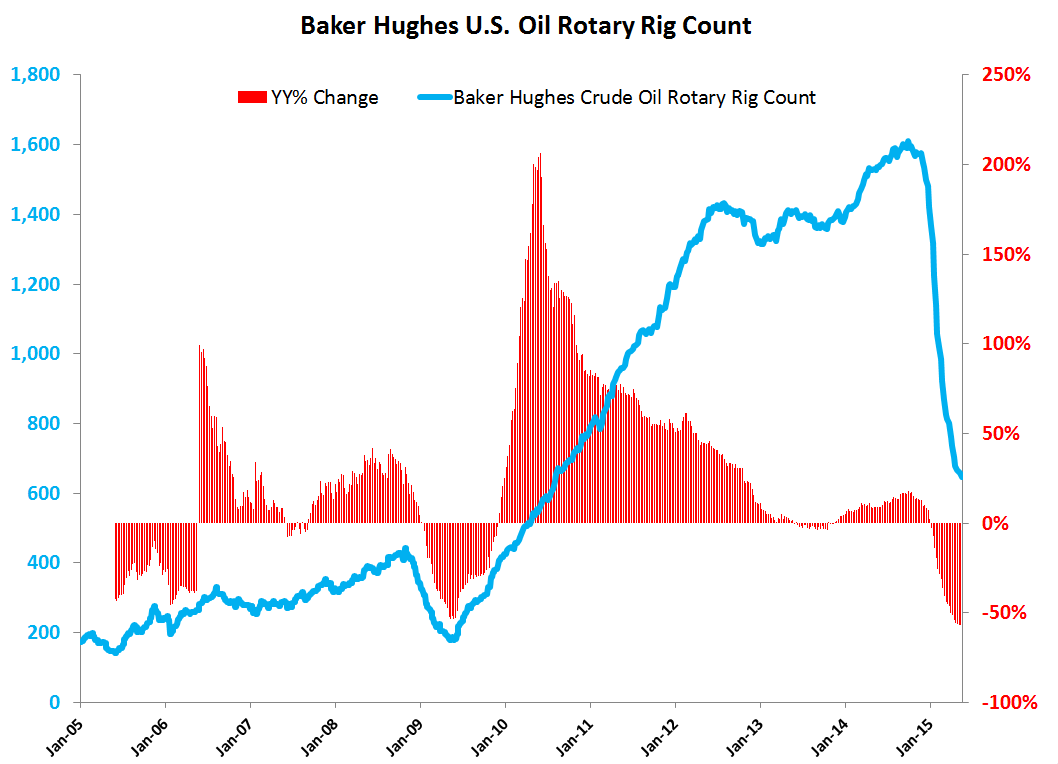

Rigs continue to come offline (although decelerating) while production per rig is still increasing sequentially --> How long can production per rig continue to increase? It could be petering out..

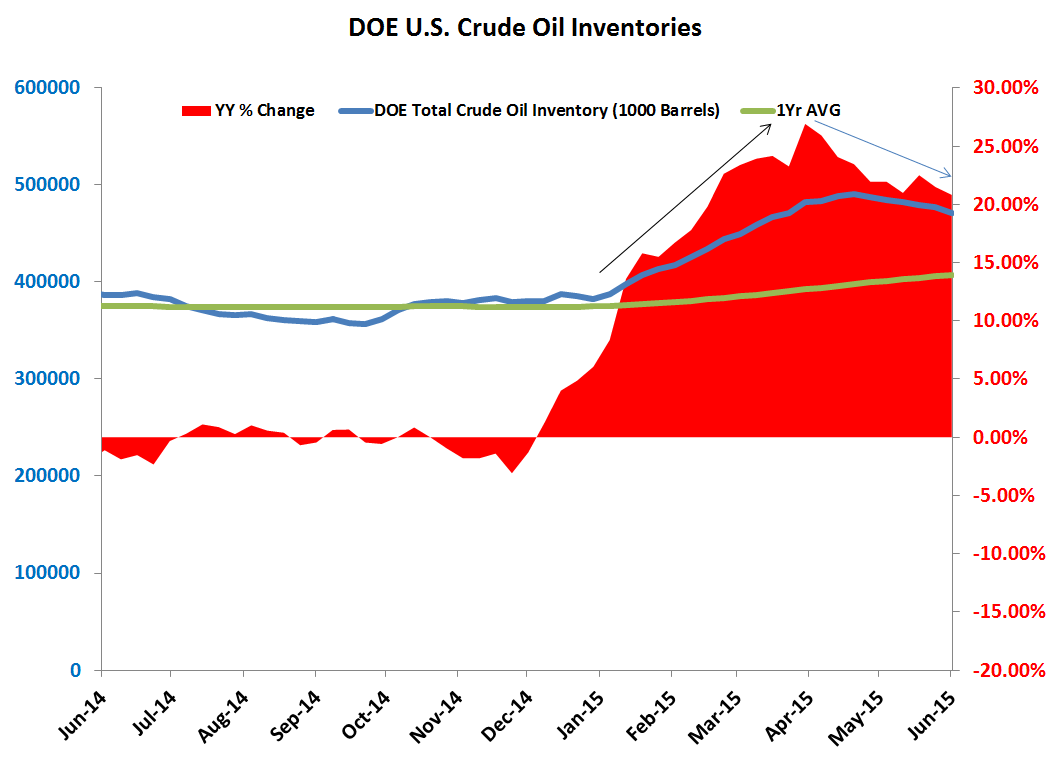

After increasing for 16 consecutive weeks and sparking fear that the U.S. may be running out of storage space, crude oil inventories at commercial refiners have declined for 6 consecutive weeks coming out of the seasonal refinery maintenance season

BEARISH VIEW

What we viewed as a big consensus short bias to crude (and all commodities for that matter), has been washed out.

Consensus Positioning usually chases price. We saw this at the lows in commodity prices in March (the market moved shorter of commodities the more they went down!)

As you can see in the chart below, the market is longest (most bullish expectations) when prices are highest.

While showing signs of deceleration, domestic crude oil production is still touching new highs not seen in 43 years. The EIA reported a 43-Year high of 9.6MM B/D of production in May (NOTE: The EIA has upwardly revised preliminary estimates for February, March, and April production numbers which originally showed a noticeable deceleration in production starting in March. The blue series in the chart below estimates their reported figures in March. They have since been upwardly revised.

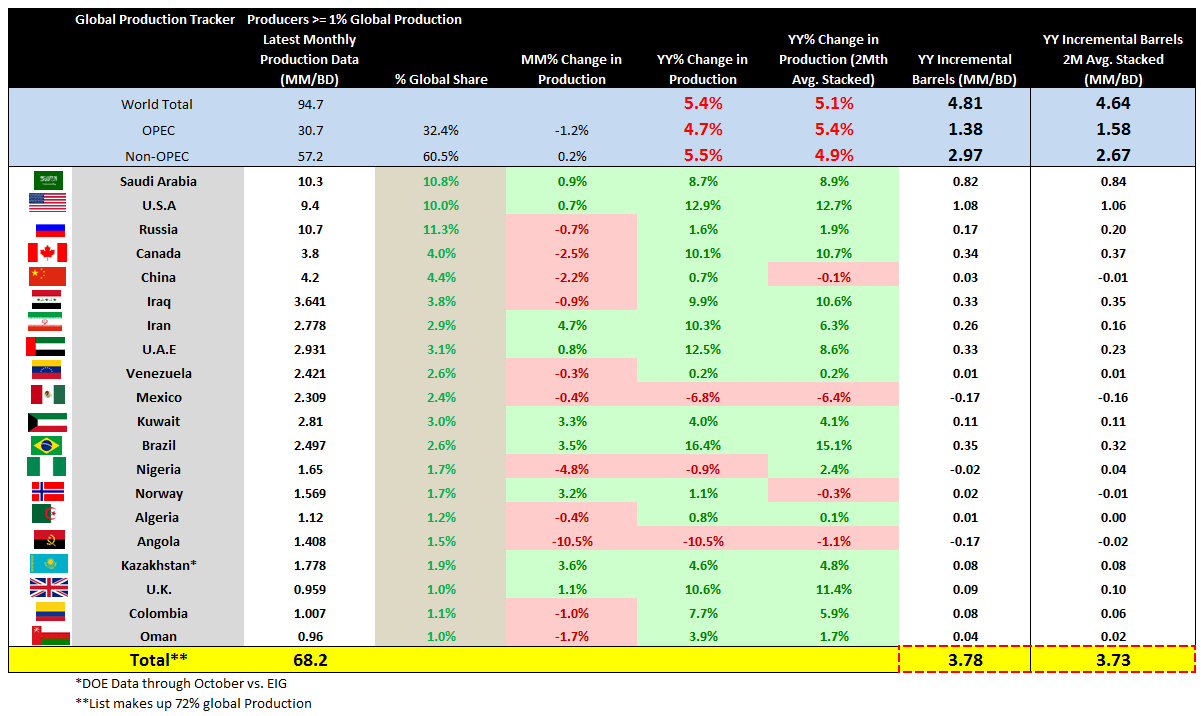

On a global scale, oil markets are as competitive as they’ve been in a long time. Global crude production in 3 of the top 4 producing countries is up double digits YY and positive in 17 of the top 20 producing countries, also on a YY basis.