Takeaway: The current trend in commodity strength vs. a declining U.S. dollar has legs into the FED meeting next week, but we continue to believe that global deflation and FX devaluation from abroad will pressure commodity prices over the intermediate to longer-term. See the debate below.

------

In a recent note, Re-Visiting Conflicting Signals and Communicating the Internal Debate , we outlined some of the conflicting signals that typically encompass a TREND reversal in an asset class by taking a look at crude oil specifically. This debate is updated in two sections (BULLISH vs. BEARISH Signals) with a confluence of easily consumable charts and commentary, much of which can be applied to the broader commodities complex and all of its derivatives. Please reach out to us with any comments or questions.

To be clear, the Hedgeye macro view is that the USD will continue to strengthen over the longer term.

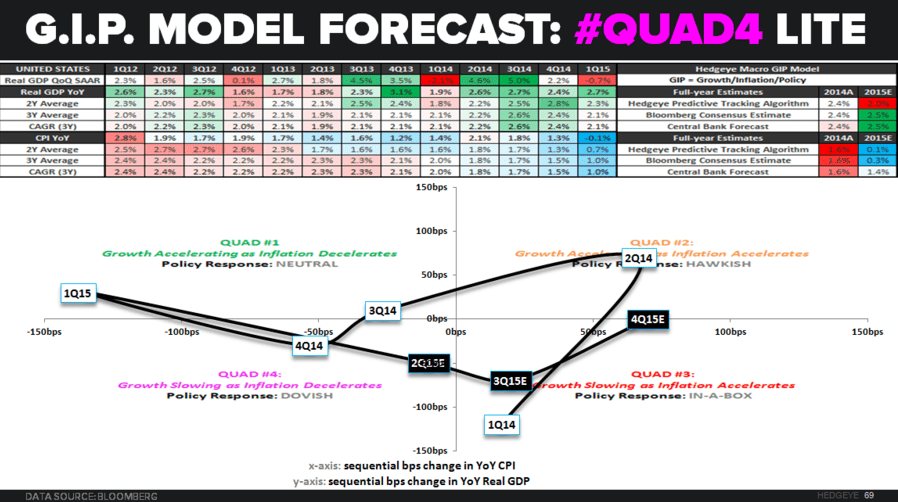

Net exposure to commodities in our asset allocation model has been mythodically increased to its current 12% level in reaction to what we expect to be yet another round of downward revisions to growth and inflation expectations. Full-year growth and inflation forecasts in our GIP model remain well below both consensus and central bank estimates and the trend in the macro data remains one of deterioration. (Counting Down to Recession?)

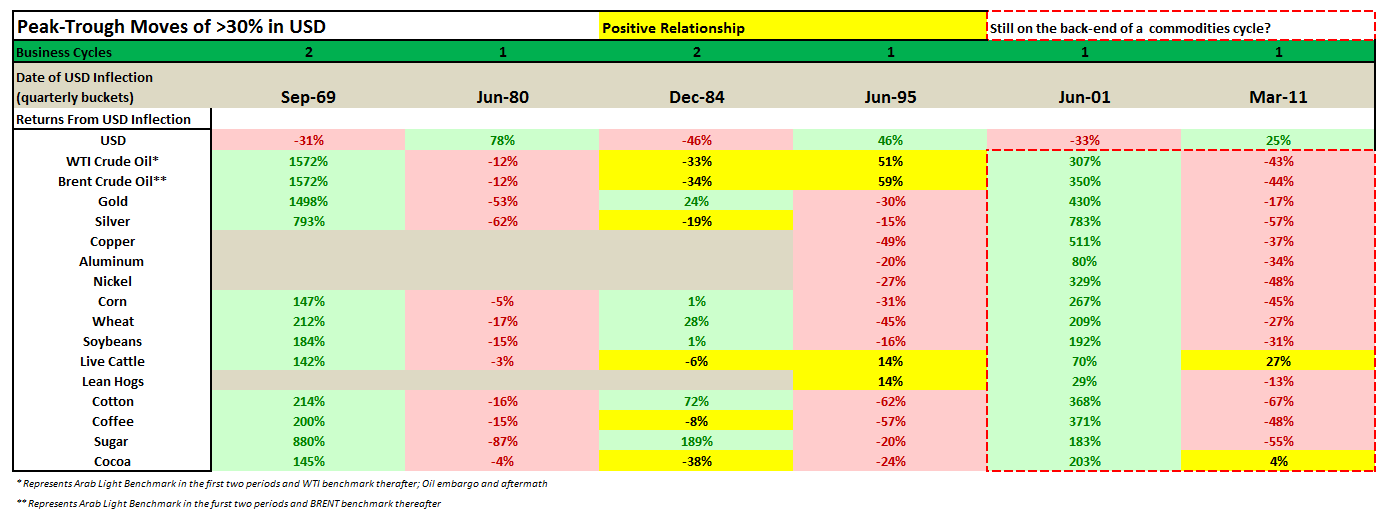

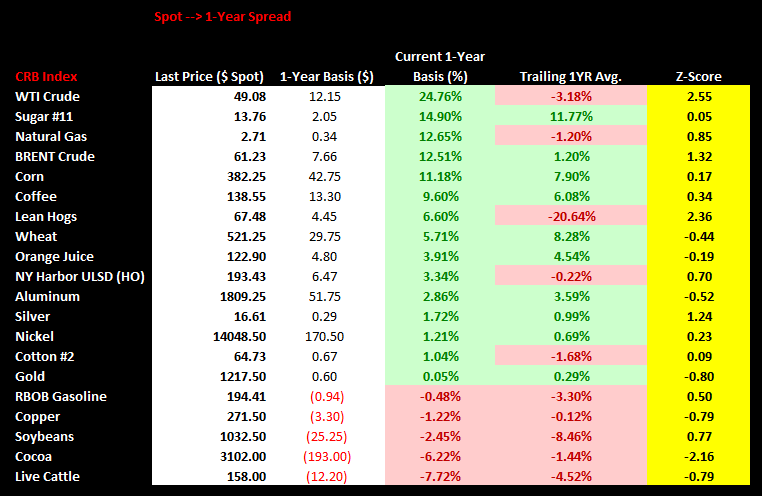

To regurgitate a few of the most relevant slides from our Q2 macro themes deck, our view on the currency shapes our biases toward managing this commodity exposure (fading the speculation-fueled, exhaustive price movements within intermediate and longer-term directional biases). Aside from the longer term cycle charts below which are self-explanatory, we would ask the following question with regards to the current state of physical oil markets: How much has actually changed since the $43-handle on WTI in March?

Given the current set-up of relative monetary policy accommodations around the world attempting to arrest the inevitable cycle, we like GOLD and CRUDE OIL LONG side at a time and price given the divergence between Hedgeye and consensus expectations.

GOLD (ETF: GLD) is currently a long position in real-time alerts. We have also been in and out of crude oil (via OIL) long side since both completed a BEARISH to BULLISH TREND reversal in the mid-May.

Below we outline the BULL/BEAR Debate...

------

BULLISH Indicators:

1. The FED’s addressing of the Q1 GDP bomb at next week’s FOMC meeting, along with the deteriorating trend in domestic economic data (ex. labor market) which we expect to be USD bearish near-term

2. TREND in U.S. data continues to drive bullish psychology in WTI

- GROWTH: The FED will be forced to address the big downward revision in Q/Q SAAR GDP for Q1 to -0.7% vs. the original print of +0.2%

- INFLATION: CPI for April fell to -0.2% YY from -0.1% in March and comps continue to become more difficult throughout the second half of the year

- The Hedgeye macro GIP model (GROWTH, INFLATION, POLICY) is still tracking well below both consensus and Central Bank forecasts for the full year 2015, and we expect a continued trend in downward revisions to growth and inflation to manifest once again

- Crude production growth is decelerating alongside a recent trend in declining inventories (changes on the margin from a bombed-out consensus stance can whip around prices)

------

BEARISH Indicators:

1. Consensus short bias has been washed out from the March lows in crude oil and is now chasing price higher

2. On a global scale, there is still a surplus in oil, and preliminary domestic production estimates from the EIA have been upwardly revised. In effect, net of the currency move which is our most important indicator, not much has changed fundamentally since March

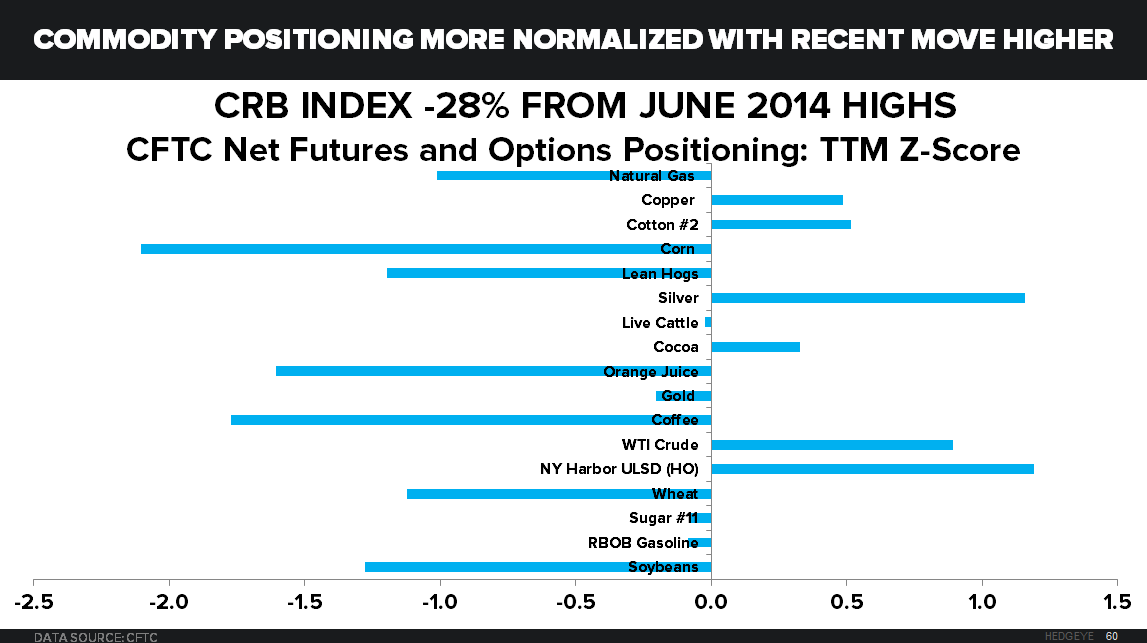

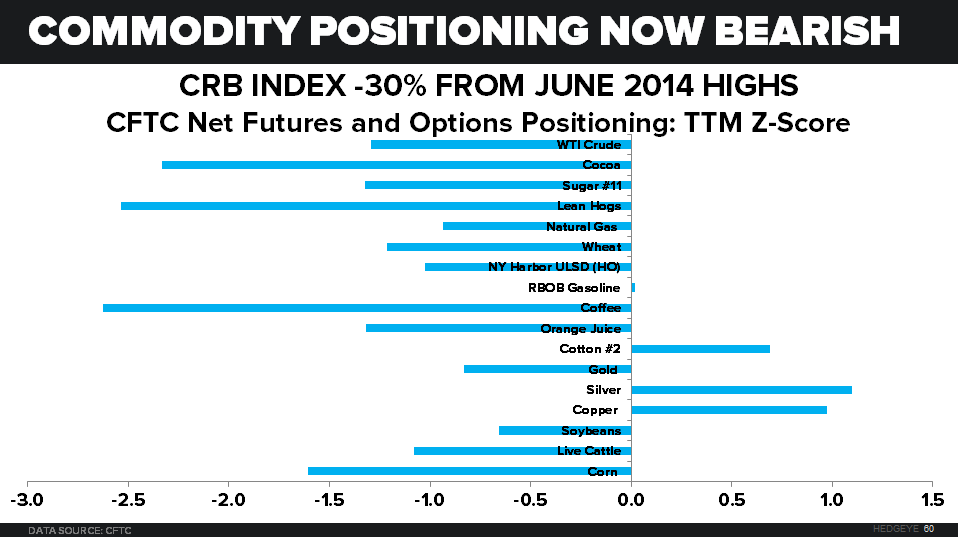

- Consensus short positioning in commodities, as evidenced by the CFTC Commitments of Traders Report, is much more normalized

- Overall expected volatility and the big divergence in downside protection has flattened out

- Drastic contango in commodity futures curves is also flattening out

- While showing signs of deceleration, domestic crude oil production is still touching new highs not seen in 43 years. The EIA reported a 43-Year high of 9.6MM B/D of production in May (NOTE: The EIA has upwardly revised preliminary estimates for February, March, and April production numbers which originally showed a noticeable deceleration in production starting in March (See table below)

- A survey of oil companies from a two-time Hedgeye Guest speaker, Leonardo Maugeri, suggests most cap-ex cuts haven’t hindered projects already underway:

“I ran a test on a sample (20) of large and medium-sized oil companies, asking each one about its expectations for the future. With two exceptions, all of them answered me that they believe firmly in a short-term rebound of crude oil prices, specifically because of the investment cuts announced by everyone. The next question was: You also announced massive cuts, but have you cut investments in oil development that is underway? The answer was a flat “no.” Naturally, the final question was: Then from whom do you expect the future production cuts?

After some perplexity, the general answer I received was "from others." I could only follow up with a supplemental question: But who are the others, in detail? No one could explain it.”

- The trend in commercial refinery inventory draws has been a psychological supporter of oil prices, but overall inventories are not far off of all-time highs (still +~20% YY)

- Global crude production in 3 of the top 4 producing countries is up double digits YY and delta positive in 17 of the top 20 producing countries, also on a YY basis

CFTC Positioning on the March Lows in Commodity Prices vs. Current (Biggest reversal in energy).

CURRENT Positioning:

MARCH Positioning:

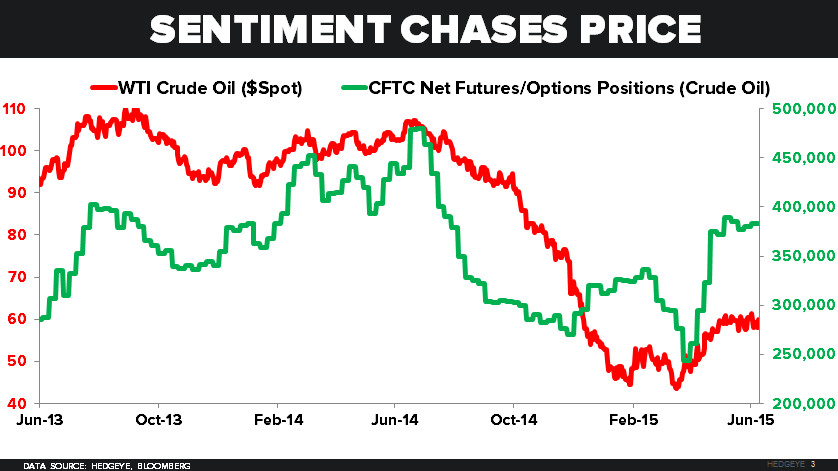

Crude Oil Positioning Chases Price:

The following table looks at volatility skew at different points in time on spot contracts since last summer. Both the trend in volatility and negative skew have normalized since crude moved off its 2015 lows.

The Contango in futures markets has become much less drastic since March:

CURRENT 1-Yr SWAP

MARCH 1-Year SWAP

PRELIMINARY EIA ESTIMATES (BLUE SERIES) vs. revised numbers

Aggregate commercial crude inventories not far off of all-time highs

GLOBAL PRODUCTION MONITOR

Ben Ryan

Analyst