The Hedgeye Financials team hosted a conference call with the CEO of the Accounting Observer, Jack Ciesielski who has done deep dive work on the current impact of the strongly trending U.S. dollar on the constituents of the S&P 500. The replay of our call is below:

Launch audio replay HERE

Materials for the presentation are HERE

The 3 most important takeaways from the call in our view were:

1.) The impact of the U.S. dollar continues to increase into 2015, with the +11.3% increase in the U.S. currency in 2014 accelerating into the first quarter of this year with another +7% rally. In totality, 296 companies out of a pool of 336 companies on a December fiscal reporting schedule reported declines in cash and cash equivalents from a stronger dollar.

2.) Exposure is not created equal with 24 companies experiencing a greater than 7% decline in their cash balances in the first quarter of 2015 alone. Losses in cash and in equity balances are a new phenomenon over the past 6 quarters, with very little impact being felt in 2013. Bellwethers including Philip Morris, McDonald's, and Kimberly Clark have lost -19.8%, -10.9%, and -7.1% of their cash resources respectively due to currency fluctuations net of hedges thus far year-to-date.

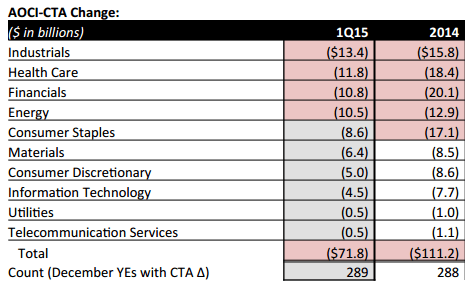

3.) Industrials, Healthcare, and Financials are shouldering most of the currency load with the Energy sector not too far behind. Although, most investors think that matching revenues and expenses in foreign operations as well as financial hedging is the most effective way to manage FX risk, the Account Observer outlined that only matching foreign subsidiary equity with the consolidated parent equity balance is a way to truly nullify FX exposure.

Macro Team