Editor's Note: Below is a chart and brief excerpt from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. Click here to get ahead of the pack and start your market morning right.

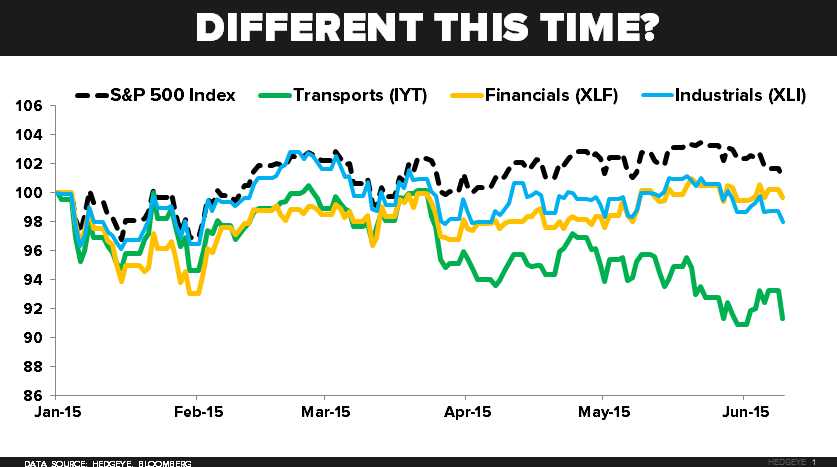

...In macro strategy there are some leading indicators that even the most creative storyteller can’t convince you that “it’s different this time.” When we went bullish on US #GrowthAccelerating in 2013, the Dow Transports (IYT) index was breaking out to the upside.

Now, after 73 months of a US economic expansion, it’s breaking down:

- Transports (IYT) led losers yesterday, down -2.1% vs. SPY -0.65%

- Transports (IYT) have been leading losers for the last month, -4.9%

- Transports (IYT) are now -8.7% for 2015 YTD

So what say you Mr. Global Growth Is Back man?