Editor's Note: Below is an excerpt from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. Why settle for an excerpt? Click here to subscribe.

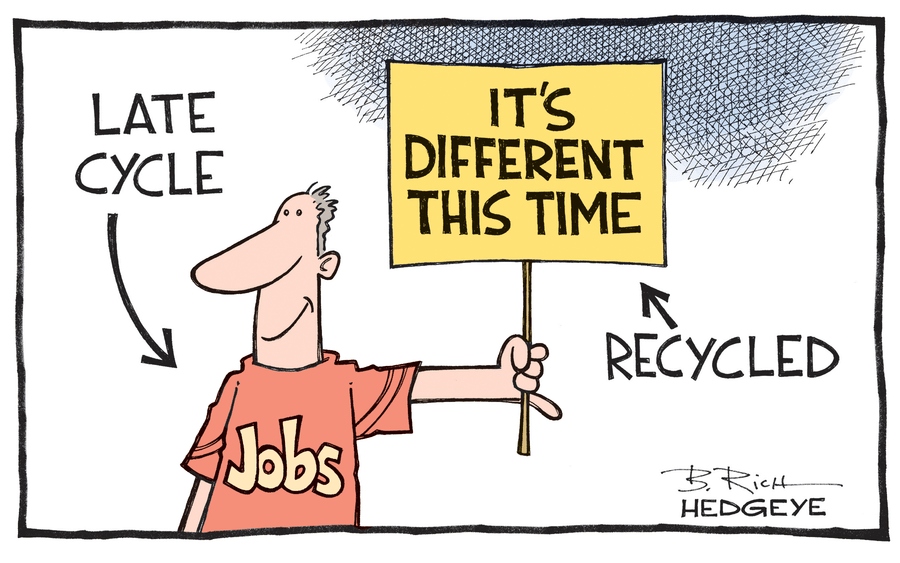

"...I’m not capitulating on the Slower-For-Longer (lower rates) cycle call this morning. If US growth was accelerating, I would. On jobs, #history students know that Non-Farm Payrolls rising is what happens AFTER the US economic cycle has already peaked.

...Yeah, I know – the Fed and its Old Wall research departments are all over it, reminding you about that this morning. But, unless it’s “different this time”, US non-farm payrolls are in the #process of peaking. And I’m not a big fan of capitulating at peaks..."