ZOES in on the HEDGEYE Best Ideas list as a LONG

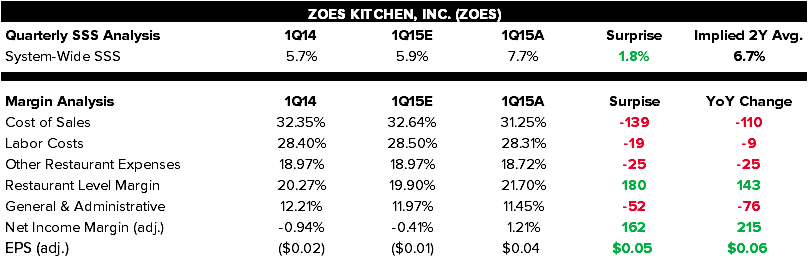

ZOES delivered a fantastic quarter, exceeding our already bullish expectations. The company beat on nearly every metric, driven by same-store sales, climbing to 7.7% beating consensus by 180 basis points (traffic was up 3.7%). Coupled by top ($63mm vs. consensus $61.4mm) and bottom line beats ($0.7mm vs. consensus -$0.1mm), there was nothing to complain about in this one.

Management increased its full-year 2015 guidance, including higher 2015 revenues of ($218mm to $223mm vs. prior $215mm to $220mm) and vs. consensus $219.9mm. The higher revenues growth is driven by high-quality 2015 comps of 4.0% to 6.0% vs. consensus +5.1%, but which now incorporates no new pricing in 2H15. Management also guided to higher restaurant contribution margins of 20.0% to 20.5% vs. 19.7% to 20.2% and new 2015 new store development of 31 to 33 vs 30 to 33.

As shown in the table below, they are effectively growing there business, while intelligently managing cost line items, to maintain a healthy company.

Same-Store Sales Composition

Same-store sales increased 7.7% during Q1 FY15, consisting of a 3.7% increase in traffic, a 2.8% increase in product mix and a 1.2% increase in price. Since the price increases were taken last year, that consideration will go away this July, leading to management aiming for 4-6% comp sales growth for FY15. The two biggest contributors to mix were catering and new flavors of hummus.

Controlling Costs

We came out of this earnings report being very positive about management doing all the little things right. They continue to prove that they are some of the best operators in the industry. Importantly, many small cap restaurant companies with an undisciplined unit growth strategy experience significant labor inefficiencies as they expand. ZOES is in a different class of companies. In a quarter where ZOES opened 12 new company-owned restaurants they managed to decrease both COGS and labor.

COGS were down 140 basis points, primarily driven by new annual pricing agreements for produce, feta cheese and olive oil. Although some of these Q1 savings will be partially offset by rising chicken prices (which have increased in Q2 by 15% sequentially since Q1). The company is projecting full year COGS to be slightly above 32% which would be flat relative to last year. This is virtually unrelated to avian flu, per or thought leader call, only 1% of chickens used for their meat have been infected. Additionally, eggs represent roughly 1% of COGS, making those price increases insignificant.

Labor costs are obviously a growing concern around the country but ZOES has been methodical about this cost line. They track labor on a daily basis, run labor matrices, and have become much more efficient at opening stores. They expect this number to increase slightly as they have added an additional manager at seven high volume locations, to build out the bench of managers to enable future growth. This extra cost now will pay off greatly in the future.

Outlook

ZOES was added to our Best Ideas list as a long on 4/02/15, admittedly since then the stock hasn’t moved up much, just about 3.8% but the underlying thesis is being confirmed.

LTM Stock Price Performance

We still like ZOES on the long side for many reasons, including its:

- Superior brand positioning

- Management philosophy and execution

- Unit opening geographic profile

- Early-stage average unit volumes and returns

We want to close this note with a quote from the CEO that describes the basis for our bullish stance. “Zoës is a differentiated concept offering wholesome, freshly prepared Mediterranean dishes with Southern hospitality, appealing to guests across the country and inspiring them to live Mediterranean. We continue to bring this Mediterranean lifestyle to more guests, opening 12 new restaurants in the first quarter, and we remain on track to open 31 to 33 new restaurants in 2015. We are confident that we can successfully operate over 1,600 units in the US long term.” This is the most differentiated offering in the quick service segment, and this team knows how to take advantage of that.