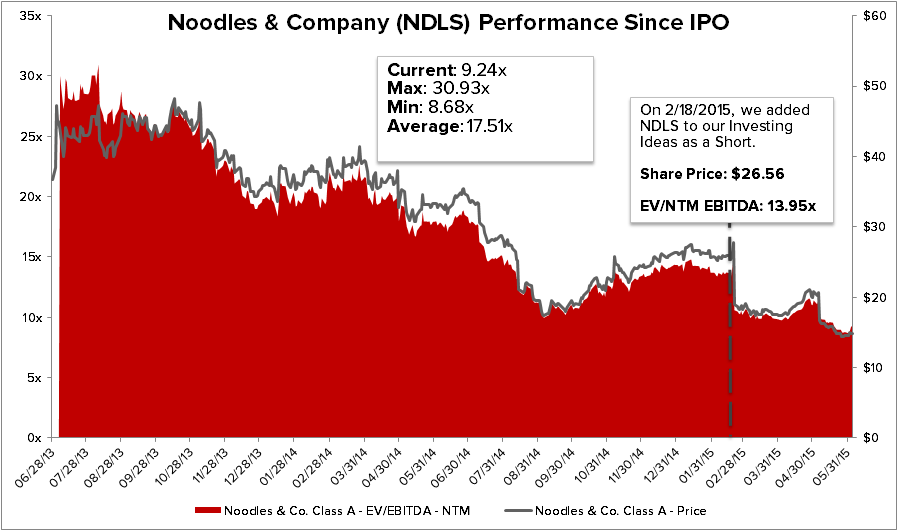

Today we are announcing the removal of NDLS from our SHORT LIST, at this point we believe the stock has been beat to the floor. We originally added it to our Investing Ideas list as a short on 2/18/15, and as you see in the chart below it was a great time to get in short. Since our call the stock price has traded down 44.2% falling from $26.56 to $14.81. The valuation of this company is very much in line with where we think it is worth and we do not believe there is much more room to go lower, EV/ NTM EBITDA is down 33.8% from our call to 9.24x.

Our original reasons for shorting the stock still hold true, but for the most part are now priced into the valuation:

- Cost of sales inflation: management is only estimating 2% food inflation, but durum wheat prices are under pressure and food cost estimates could head higher as we move into the back half of the year

- Geographic concentration: the company has a notable number of stores in the DC metro area, which is an extremely competitive market

- Rising labor costs: 52% of company operated restaurants are in markets that are facing minimum wage increases in 2015 or 2016 (or both), the majority of which are coming this year

- The Affordable Care Act: will add about 30-50 bps of pressure on margins in 2H15

Please note the changes made to our Restaurants Investing Ideas List below. In addition to our update on NDLS, MCD has been elevated to our LONG LIST (previously reported), WEN dropped to our LONG BENCH (previously reported) and BOJA added to our SHORT BENCH (new).