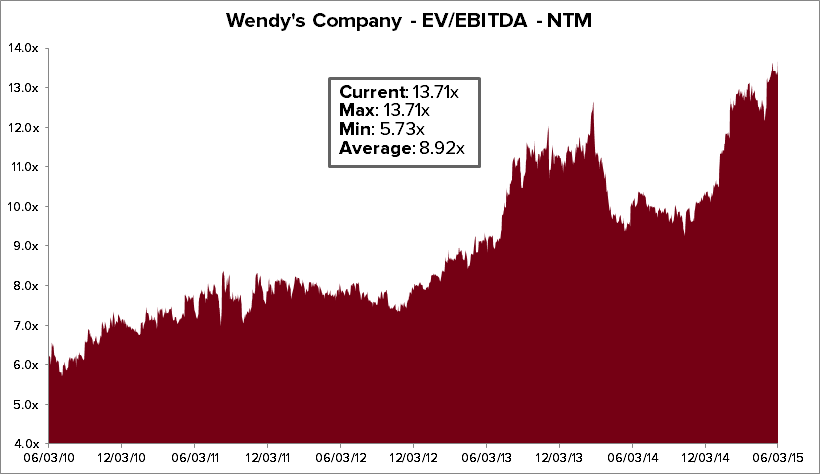

We are removing WEN from the Hedgeye Restaurants favorites list as a LONG and moving it down to the LONG Bench. WEN is up 30% year-to-date and 42% over the past 12-months. The WEN transformation is more than 50% complete and the stock reflects most of good news. To that point, over the past two years, the EV/NTM EBITDA multiple has expanded from 9.15x to 13.71x, with the stock now trading at the upper end of its peer group valuation.

Our bullish bias to WEN is based on the company’s willingness to transform the business model to a leaner, more efficient machine. The news today is a further affirmation that this process is nearly complete. As a whole, Wendy’s new operating model will deliver more predictable earnings growth, higher EBITDA margins, and higher earnings quality, while requiring less capital outlay. By 2017, WEN will have completed the system optimization initiative, where the company will be generating 80% of its earnings stream from predictable, sustainable, rental and royalty income.

All of this is now baked into the company’s valuation.

WHAT’S NEW TODAY

- The Board authorized a new share repurchase program for up to $1.4B of the company's common stock (30% of the company's market capitalization through the end of 2016)

- The company intends to repurchase shares with existing cash on its balance sheet, cash flow from operations, net proceeds of $925MM from its recently completed securitization refinancing, expected after tax proceeds of $350MM from the third phase of its system optimization program and the after-tax proceeds of $50MM from the sale of its bakery operations

- As part of the new authorization, the company will commence an $850MM share repurchase program today, including a modified "Dutch Auction" tender offer to repurchase up to $639MM of its common stock at a price range between $11.05 and $12.25 per share

- The tender offer is part of an $850MM stock buyback program, which also includes a separate purchase of up to $211MM of the company's common stock from the Trian Group

- The company expects to use the remaining $550MM of its $1.4B share repurchase authorization before the end of 2016, as funds become available from the company's system optimization initiative

2015 OUTLOOK

- The company reaffirmed that its business trends remain on track to achieve the 2015 outlook issued in its first-quarter earnings release on 6-May

- WEN now expects 2015 Adjusted EBITDA of $375MM to $385MM vs prior $390MM to $400MM and consensus of $400.69MM. In addition, 2015 Adjusted EPS is now $0.31 to $0.33 vs prior $0.33-$0.35 and consensus $0.34 (excluding $0.02 attributable to its bakery operations)

Same-Store Sales

- Same-restaurant sales growth of 2.5 to 3.0% at Company-operated restaurants and company-operated restaurant margin of 16.5 to 17.0%

THE LONG-TERM MODEL

The company's expected restaurant count for its long-term outlook includes sale of 100 Canadian restaurants and the sale of 540 additional domestic by the middle of 2016. The company's long-term outlook includes the expectation for average annual system-wide same-restaurant sales growth of 2.25 to 3.0% beginning in 2016

EPS TARGETS

- High single-digit Adjusted EPS growth in 2016

- High teens Adjusted EPS growth in 2017

- Accelerating to 20% beginning in 2018

EBITDA TARGETS

- Flattish Adjusted EBITDA in 2016

- Low-single digit Adjusted EBITDA growth in 2017

- High single-digit Adjusted EBITDA growth in 2018

The company also continues to expect to achieve the following system goals by the end of 2020:

- Average unit sales volumes of $2.0M

- Restaurant margins of 20%

- A sales-to-investment ratio of 1.3 times for new restaurants