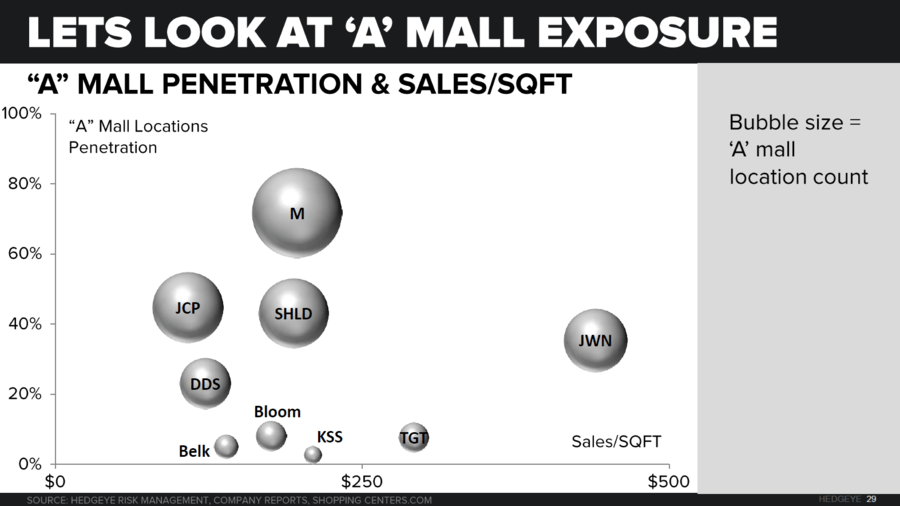

M, KSS - Macy's Real Estate at Play?

Takeaway: For starters, M's real estate portfolio is far better than every other mid-tier operator in this space with an existing presence in ~80% of the 'A' malls in the US. Add to that the High Street locations (Herarld's Square, etc.) and its clear that the company has a pretty attractive owned real estate portfolio. Will the company monetize that? Hoguet did nothing on the last call to dispel the possibility of a real estate play.

But, that seems like a near term solution being floated by investors who don't see a whole lot to get excited about in the base business. M paid ~$300mm in rent (1% of revenue) last year -- assuming that the company pays $3/sq. ft. for it's leased DC space that implies $5.50/ft. for its leased/ground leased properties that are not capitalized. Assuming an identical rate for the 90.5mm sq. ft. of owned real estate (which is probably too low given that lease terms will be marked to market for any sale leaseback transaction) we would see a minimum of 170 bps of added margin pressure from rent alone.

As for the crown jewel in the portfolio -- it is not the Saks 5th Avenue location which was valued at $3.7bil just a few months ago. Herald Square is about 3x the size of that building but its designation as a National Historic Landmark makes it far less attractive for anybody looking at a potential redevelopment. Just yesterday the 78k sq. ft. Old Navy door across the street which has a footing that could support a 300,000 sq. ft. mixed use property was acquired by Vornado for $355mm, a 41% premium to the price struck 12mnths ago. If we discount the transaction value for the Historic Landmark status we get to a valuation of about $1.3bil ($600/sq. ft. x 2.17mm sq. ft.). Add that to the existing 88mm of owned sq. ft. at near 'A' mall cap rates and rent/sq. ft. of around $7 and we get to an aggregate valuation in the $9.5-$12bil range.

Lastly, we think it's important to draw a distinction between M and KSS. Unlike M, KSS has limited mall exposure (virtually 0 'A' Mall exposure) and operates mostly in strip centers -- there are over 7,000 in this country. It's hard to argue an attractive valuation especially when you consider the holes being opened up by the consolidation of the office supply stores, Best Buy, etc. Where M has beach front property, especially in its 'A' mall locations, KSS would be the equivalent of a 2hr drive inland.

SIGMAs for Retailers Reporting in the Past 24 Hrs

ASNA, ANN - If you didn't know why ASNA is buying ANN, now you know. It's results were not good. But that won't matter now that it's crown jewel is Ann Taylor instead of Lane Bryant, Dress Barn, or Justice. Seriously...what is this company becoming?

GES - 1Q16

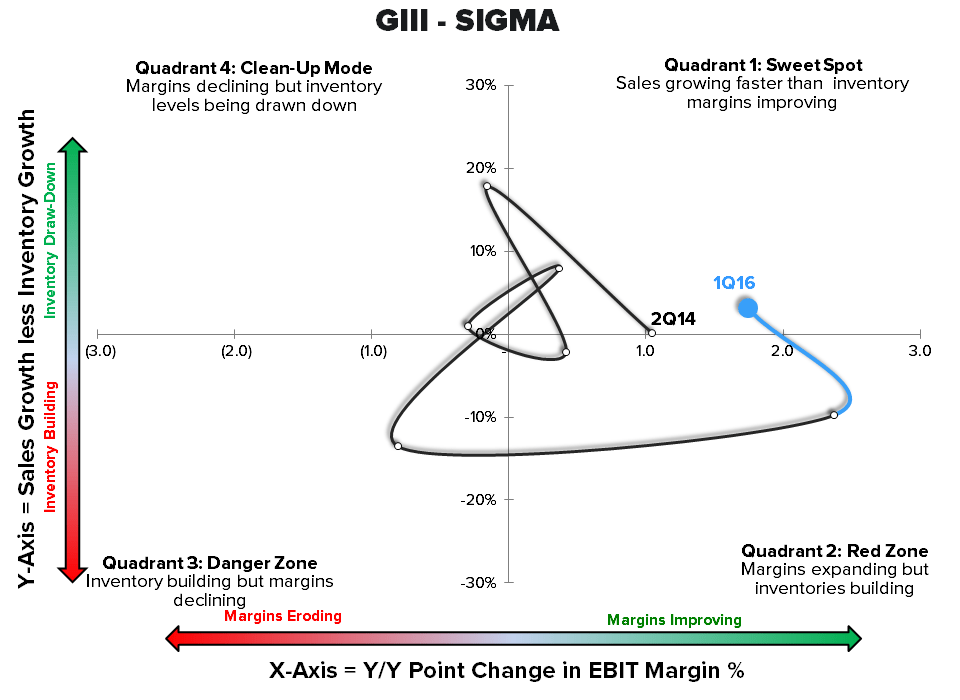

GIII - 1Q16

VRA - 1Q16

OTHER NEWS

Toys 'R' Us Hires New CEO With A Rich IPO Resume In David Brandon

VRA - Vera Bradley Names Theresa Palermo EVP, Chief Marketing Officer

(http://investors.verabradley.com/releasedetail.cfm?ReleaseID=916128)

True Religion promotes interim VP to CEO

(http://www.chainstoreage.com/article/true-religion-promotes-interim-vp-ceo)

Jo-Ann Fabric among first retailers to partner with Pinterest’s new Buyable Pins

USTR: TPP to Lower Tariffs on U.S. Exports

(http://wwd.com/business-news/government-trade/ustr-tpp-lower-tariffs-u-s-exports-10139029/)

TGT - Target Takes Tartan to the Limit

(http://wwd.com/retail-news/mass-off-price/target-tartan-plaid-merona-mossimo-10139352/)