Editor's Note: The excerpt and chart below are from today's Morning Newsletter written by CEO Keith McCullough. If you're not a subscriber yet, you're missing out. Click here to learn more and subscribe.

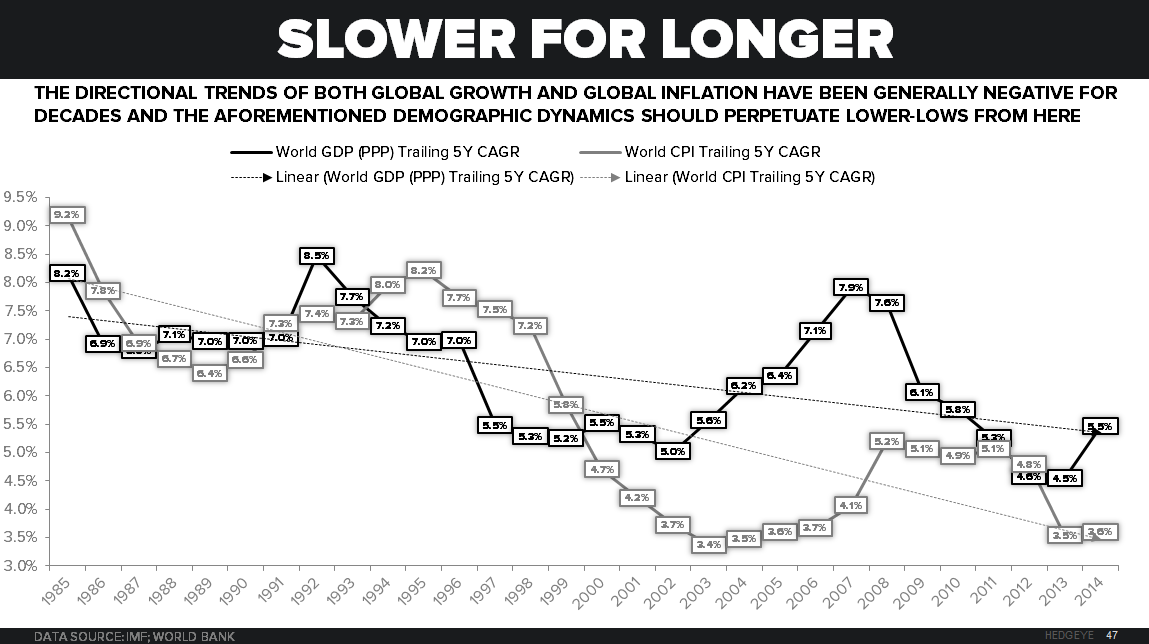

...The two core components of our Global Macro slide deck remain A) the cyclical call (USA in a #LateCycleslowdown) and B) the secular call (#Demographic slowing of core baby boomer consumption cohorts, in the US, Europe, Japan, and China).

Click to enlarge